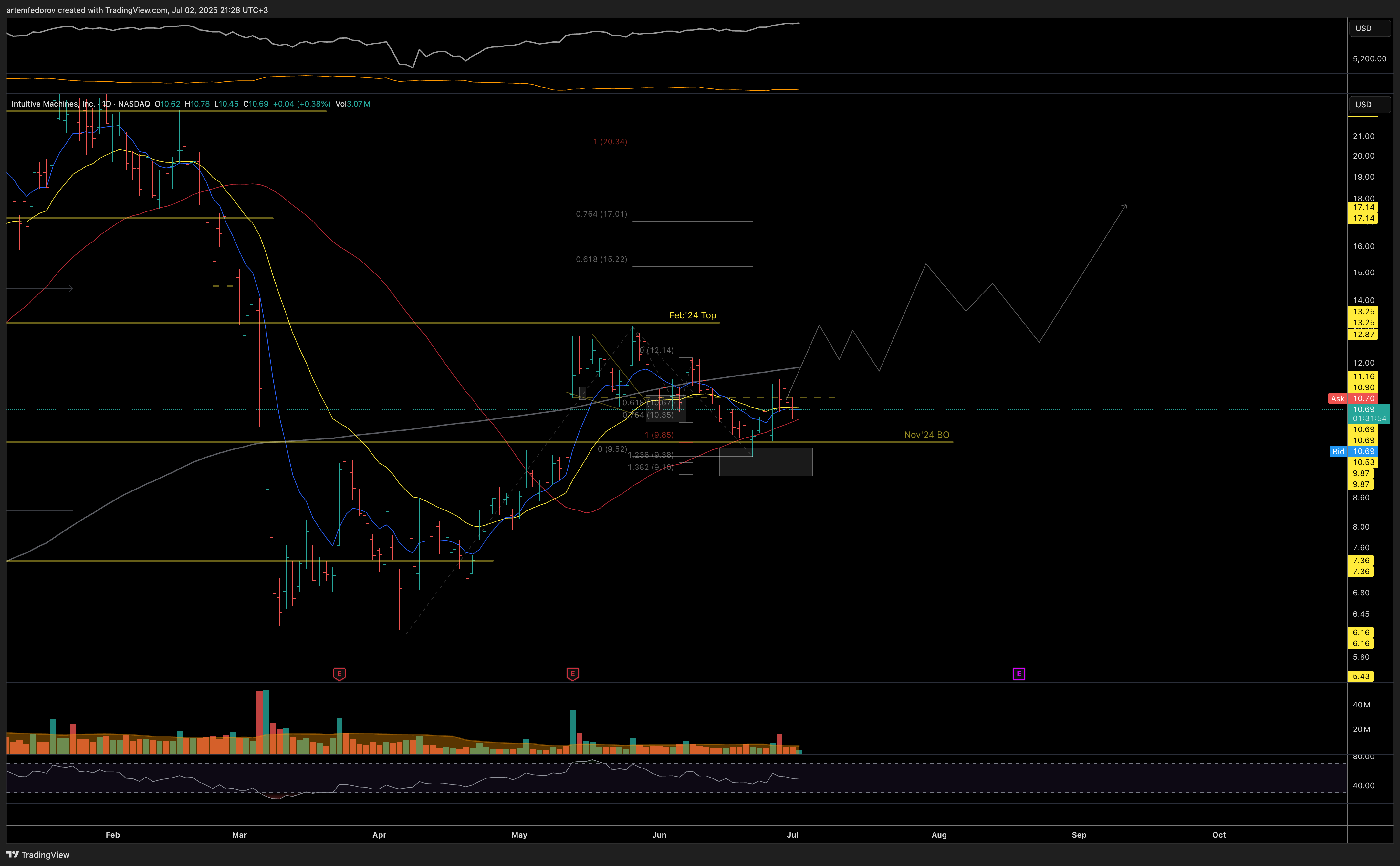

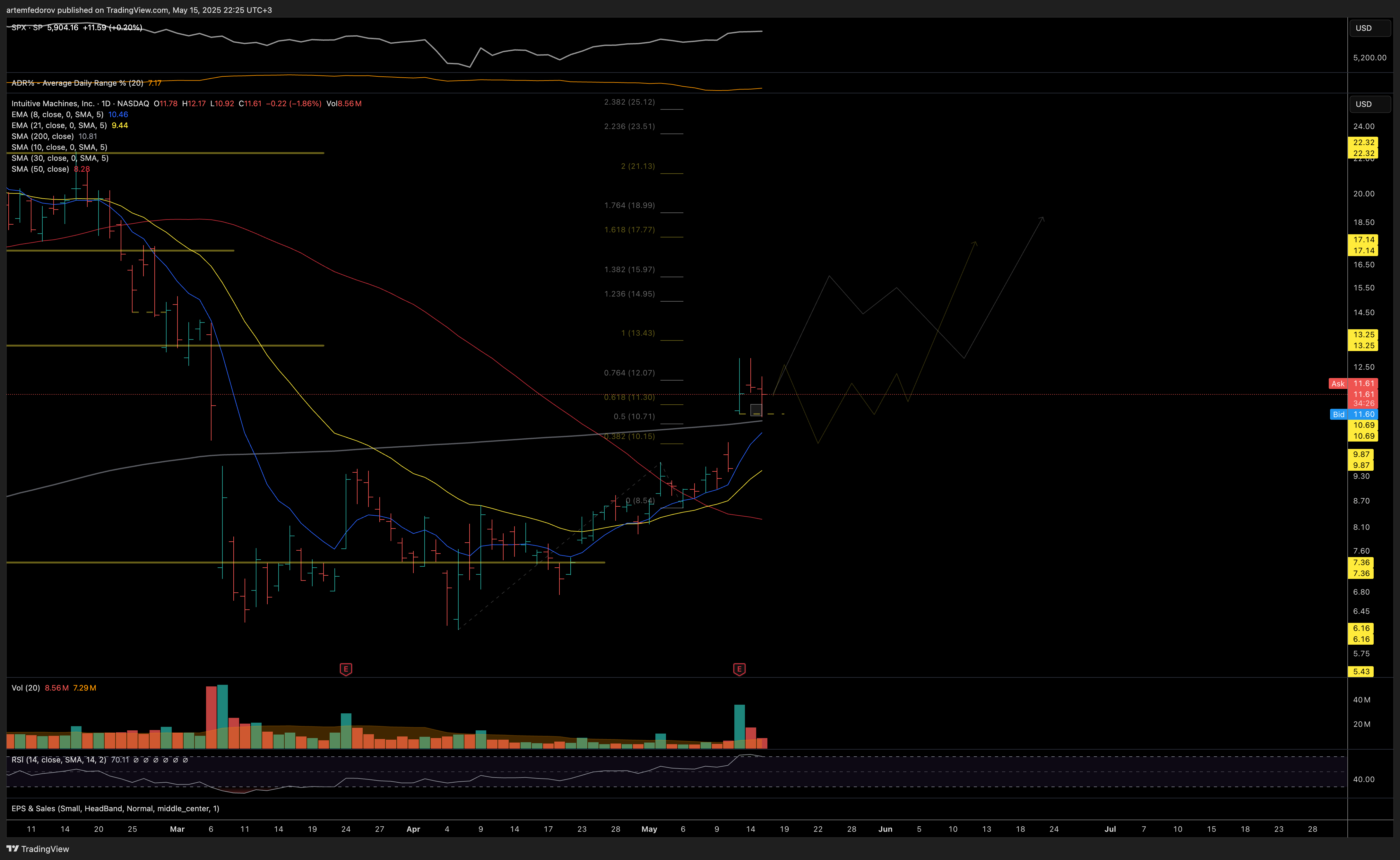

LUNR Like the action here with today’s volume breakout attempt. - Stocks was trading at just 5x projected sales and below industry-average forward P/E - Revenue expected to grow ~30% annually through 2026, driven by expanding government contracts in space and lunar markets (leading sector per IBD) - Increasing institutional interest - Strong EPS estimates for 2025 and 2026

Still overhead supply from the sharp Jan’25 selloff, but with tight risk, the reward looks compelling.

Consensus: Buy/Moderate Buy – Most analysts rate LUNR as a buy; only one “sell” and one “hold” among seven or eight

Average 12‑month price targets range from $15.2 to $16.5, suggesting upside of approximately 40–50% from current ~$10.94

Top analyst picks:

Canaccord Genuity: “Strong Buy” with a target between $21–22

Cantor Fitzgerald: “Buy/Overweight” with a range of $13→$16

Barclays, Benchmark, and others generally between $13–18, mostly positive .

🚀 Catalysts & Strengths

NASA contract wins: Leading a $4.82B Near Space Network deal, plus ongoing CLPS and Lunar Terrain Vehicle projects

Rapid revenue growth: Q4 saw revenues surge ~80% to $54.7M; backlog hit a record $328M

Debt‑free & improving cash: Operational costs remain high, but debt paid down and adjusted EBITDA expected to reach breakeven by end‑2025/2026 .

⚠️ Risks

High mission execution risk: Recent missions tipped over on the moon, impacting investor confidence

Burn rate concerns: Reddit data highlights a negative operating margin (~–86%), negative cash flow, and reliance on contract awards

Valuation premium: Price‑to‑sales ratio stands at ~5.9× against a fair estimate of ~1.2×

📊 Key Investment Takeaways

Upside Potential With targets at $15–16 (avg) and outliers up to $22, there’s ~40–100% upside potential.

Valuation Expensive by sales multiples; premium pricing factors in future mission/data upside.

Volatility Expect sharp swings tied to mission outcomes or contract updates. Strategy Fit Suited for investors bullish on the commercial lunar economy, NASA-backed growth, and tolerance for high-risk profiles.

✅ Summary Outlook

LUNR is a high-growth, mission-driven stock in the commercial space race. Backed by substantial NASA contracts, growing revenues, and improving financials, analysts generally see 40–50% upside over the next 12 months. However, the company remains unprofitable, with mission-execution and valuation concerns introducing notable risk.

LUNR in the next Monday 3/24 will be have a gap down to $6.xx that maybe a new low. After that will back to rising over Friday high, then touch the $9.00 in Tuesday 3/25. Thank me later on!