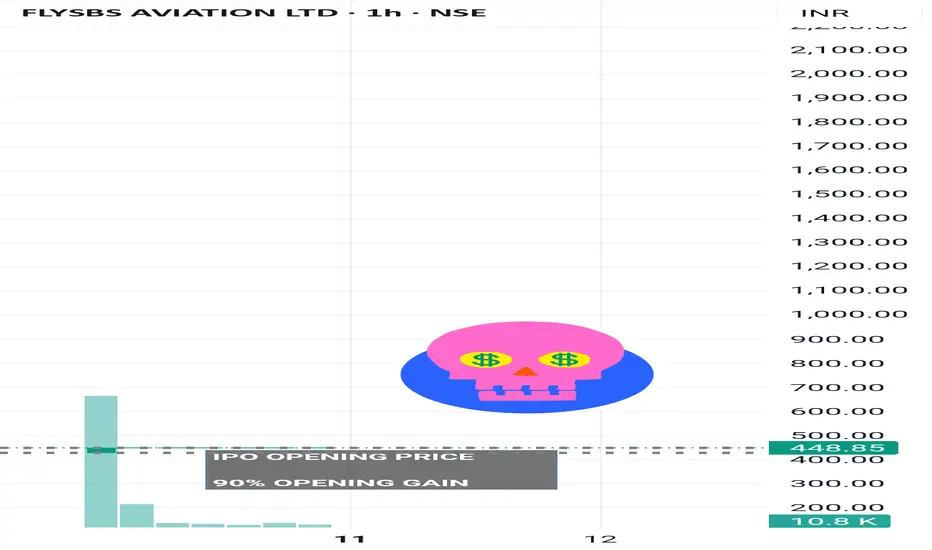

With strong sector tailwinds, rapid fleet expansion, and clear operational scale-up plans, FlySBS Aviation is well positioned to deliver sustainable positive cash flows and attractive long-term returns, offering meaningful upside for investors as industry demand accelerates

🌸 Company Overview & Industry 🌸

-FlySBS Aviation is a private non-scheduled air charter operator serving B2B & B2C clients including corporates, HNIs, celebrities, and diplomats.

-Operates a fleet of 3 owned private jets plus dry/wet lease options to meet demand surges.

-The Indian private aviation market is growing rapidly, with an expected CAGR of 8–15% over the next decade

🌸FY2025 Sales (Total Revenue: ₹193.9 Cr)🌸

Private Jet Charters: 94% (₹182 Cr)

International Missions: 77% (₹149 Cr)

Domestic Charters: 23% (₹44.7 Cr)

Medical/Security Operations: 4% (₹8 Cr)

Subscription/Leasing: 2% (₹3 Cr)

🌸Financial Highlights (FY21–25)🌸

Revenue CAGR: ~63%

Net Profit CAGR: ~70%

Operating Margin: 21%

Net Profit Margin: 14.7%

ROE: 18.9%

EPS (FY25): ₹25.47

🌸DCF Valuation Insight🌸🫰🏻

Intrinsic Value: ~₹220 per share

Justification:

The valuation captures the expected transition from a heavy investment phase with negative free cash flow toward stable and positive cash flow generation.

The reliability is moderate, contingent on effective execution of growth plans and capital management aligned with market trends

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.