THE united state interest rate stands at 4.25%-4.5%

the US10Y open the day at 4.293% and closes 4.26% a significant drop from may high of 4.62%

the dollar index is heading to 96$ after open 97.611$ to close 97.313$.

Final GDP q/q

Actual: -0.5%

Forecast: -0.2%

Previous: -0.2%

The US economy contracted by 0.5% in the first quarter, worse than the expected 0.2% decline, indicating a sharper slowdown than anticipated.

2. Unemployment Claims

Initial Claims: 236,000

Forecast: 244,000

Previous: 245,000

Initial jobless claims fell by 10,000 to 236,000, lower than forecast and near historically low levels, suggesting that layoffs remain relatively subdued despite economic challenges.

3. Core Durable Goods Orders m/m

Actual: +0.5%

Forecast: +0.1%

Previous: +0.2%

Core durable goods orders, which exclude transportation, rose 0.5% month-over-month, beating expectations and signaling some resilience in business investment.

4. Durable Goods Orders m/m

Actual: +16.4%

Forecast: +8.6%

Previous: -6.3%

Total durable goods orders surged 16.4%, a strong rebound following a prior decline, indicating a pickup in demand for long-lasting manufactured goods.

5. Final GDP Price Index q/q

Actual: 3.7%

This measure of inflation in the GDP deflator remains elevated, reflecting persistent price pressures in the economy.

Summary of Market Implications:

The larger-than-expected GDP contraction signals economic weakness, which could increase expectations for accommodative Fed policy.

The drop in initial jobless claims supports the view that layoffs are limited, but rising continuing claims suggest some labor market softness ahead.

Strong durable goods orders point to underlying business investment strength, providing a mixed but cautiously optimistic outlook.

Elevated inflation as shown by the GDP price index keeps inflation concerns alive.

Overall, the data presents a complex picture of a slowing economy with pockets of resilience and ongoing inflationary pressures

the interest rate remains 4.24%-4.5% ,the bond market remain weak on fiscal policy challenges and pending rate outlook.

the 10 year bond yield is trading around 4.291% -4.26% and edge lower from fundamental outlook.

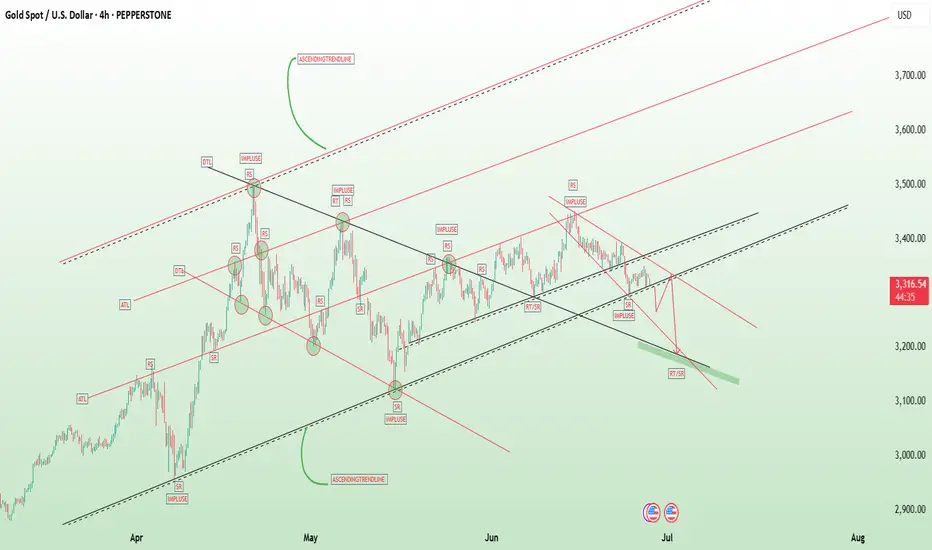

gold on ascending trendline connecting April till June and found support at 3312-3314.

buyers during newyork session will build momentum on technical to bridge 3350 supply .

break below 3311-3314 will heading to my demand floor .

the US10Y open the day at 4.293% and closes 4.26% a significant drop from may high of 4.62%

the dollar index is heading to 96$ after open 97.611$ to close 97.313$.

Final GDP q/q

Actual: -0.5%

Forecast: -0.2%

Previous: -0.2%

The US economy contracted by 0.5% in the first quarter, worse than the expected 0.2% decline, indicating a sharper slowdown than anticipated.

2. Unemployment Claims

Initial Claims: 236,000

Forecast: 244,000

Previous: 245,000

Initial jobless claims fell by 10,000 to 236,000, lower than forecast and near historically low levels, suggesting that layoffs remain relatively subdued despite economic challenges.

3. Core Durable Goods Orders m/m

Actual: +0.5%

Forecast: +0.1%

Previous: +0.2%

Core durable goods orders, which exclude transportation, rose 0.5% month-over-month, beating expectations and signaling some resilience in business investment.

4. Durable Goods Orders m/m

Actual: +16.4%

Forecast: +8.6%

Previous: -6.3%

Total durable goods orders surged 16.4%, a strong rebound following a prior decline, indicating a pickup in demand for long-lasting manufactured goods.

5. Final GDP Price Index q/q

Actual: 3.7%

This measure of inflation in the GDP deflator remains elevated, reflecting persistent price pressures in the economy.

Summary of Market Implications:

The larger-than-expected GDP contraction signals economic weakness, which could increase expectations for accommodative Fed policy.

The drop in initial jobless claims supports the view that layoffs are limited, but rising continuing claims suggest some labor market softness ahead.

Strong durable goods orders point to underlying business investment strength, providing a mixed but cautiously optimistic outlook.

Elevated inflation as shown by the GDP price index keeps inflation concerns alive.

Overall, the data presents a complex picture of a slowing economy with pockets of resilience and ongoing inflationary pressures

the interest rate remains 4.24%-4.5% ,the bond market remain weak on fiscal policy challenges and pending rate outlook.

the 10 year bond yield is trading around 4.291% -4.26% and edge lower from fundamental outlook.

gold on ascending trendline connecting April till June and found support at 3312-3314.

buyers during newyork session will build momentum on technical to bridge 3350 supply .

break below 3311-3314 will heading to my demand floor .

Join My telegram Channel

t.me/+O0YhUHNCodM5Yjhk

Free Forex Signals

t.me/+O0YhUHNCodM5Yjhk

t.me/+O0YhUHNCodM5Yjhk

Free Forex Signals

t.me/+O0YhUHNCodM5Yjhk

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.

Join My telegram Channel

t.me/+O0YhUHNCodM5Yjhk

Free Forex Signals

t.me/+O0YhUHNCodM5Yjhk

t.me/+O0YhUHNCodM5Yjhk

Free Forex Signals

t.me/+O0YhUHNCodM5Yjhk

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.