AMAZON:FULL FUNDAMENTAL ANALYSIS|SHORT SETUP SCENARIO 🔔Amazon's stock price fell almost 8% on July 30 after the company released its second-quarter earnings report. The company's revenue growth did not meet analysts' expectations, and the company reported a lower-than-expected earnings outlook for the third quarter.

Amazon's fall weighed on other e-commerce and cloud stocks, as the company is considered an indicator of both markets. Many Wall Street analysts have also quickly decreased their price targets on the company's stock, citing difficult upcoming market comparisons in the wake of the pandemic. Let's take a look at the major conversations surrounding Amazon, find out who has the upper hand, the bulls or the bears, and whether the company is still a worthy investment.

Amazon's revenues increased 27% year over year in the quarter to $113.1 billion, but they fell short of Wall Street's average forecast by nearly $2 billion. The company anticipates its revenue to rise only 10%-16% year over year in the next quarter, while analysts were expecting 24% growth.

Amazon attributes the slowdown to difficult comparisons with the pace of online shopping growth caused by the pandemic a year ago. During a conference call, Amazon Chief Financial Officer Brian Olsavsky said that since last May, revenue growth "jumped to 35% to 45% and stayed at that level until the first quarter of this year, when growth was 41%." But starting in the second quarter, Amazon "began to slow down during a period of strong sales last year, and the rate of revenue growth for the year has declined."

Olsavsky foresees the slowdown to continue as "vaccines are becoming more available in many countries and people are getting out of their homes." He also noted that Amazon's average spending per Prime member "is down from the spending seen during the peak of the pandemic."

Amazon's accelerated growth during the pandemic and its subsequent slowdown make it difficult to estimate the company's near-term growth. So instead of focusing on hard year-over-year comparisons over the next few quarters, Olsavsky advised investors to look at the two-year annualized growth rate.

Olsavsky noted that before the pandemic, Amazon's earnings were up 21% for two years. But after smoothing out the volatility associated with the pandemic, Olsavsky still expects Amazon's two-year annual growth rate to be 25%-30%, indicating that its core businesses are still strong.

Amazon's long-term growth seems stable, but the main drivers of growth are changing. In the e-commerce segment, third-party sellers accounted for 56% of total paid units in the second quarter -- up from 53% a year ago -- and they continue to bring significantly higher sales growth than primary sellers.

This change is troubling because Amazon has already faced quality control problems in its third-party marketplace and persistent complaints about counterfeit products from overseas sellers.

Amazon's second-quarter revenue growth would have been even slower without the help of Amazon Web Services (AWS), the world's largest cloud infrastructure platform, and its advertising business.

AWS revenues rose 37% year over year to $14.8 billion, which is 13% of Amazon's total revenues, and its operating income rose 25% to $4.2 billion, which is 54% of Amazon's total operating income. Revenue from the "other" segment - which mostly consists of advertising revenue - rose 87% year over year to $7.9 billion, or 7% of Amazon's total revenue.

If you exclude AWS and the "other" segment from both periods, Amazon's second-quarter revenue would have grown only 22% year over year. Going even further and excluding all third-party vendor services, the company's revenue would have grown only 17% year over year.

Andy Jassy became new CEO in early July, but he has yet to provide a clear plan for the company's growth. Jassy previously led AWS, so Amazon's main profit driver - which subsidizes the growth of its low-margin retail business - is clearly in good hands.

Amazon's retail business, however, still faces serious challenges. Supermarkets like Walmart and Target have gotten better at matching Amazon's pricing and delivery capabilities, reliance on third-party sellers remains a double-edged sword, and the company is under pressure to raise wages and improve warehouse conditions. Shopify remains a major threat as it effects independent sellers to set up their online stores, and niche marketplaces like Etsy are pulling away shoppers who want more unique gifts.

Amazon also needs to expand aggressively overseas to drive new growth and reduce its reliance on an oversaturated U.S. market - but it is struggling to draw customers away from entrenched regional leaders such as MercadoLibre in Latin America and Sea Limited's Shopee in Southeast Asia.

Jassy may have to address these problems over the next few quarters to assure investors that Amazon is not losing its edge in the burgeoning e-commerce market.

Amznshort

Amazon- PLS DON'T BURN YOUR MONEY!!!Pls look at this chart and see for yourself the monthly candle we are about to produce.

This month will be hard. Hard for everyone who is investing right now.

After new all thime high

to new all time high

AMZN Amazon stock, Nice BUY setupAs you can see in the chart, the stock is trading in an uptrend, now it is making a correction, but it will go high again soon.

You can buy in the yellow area, your SL is 1 day closed candle under the trend

GOOD LUCK.

AMAZON today we have the trend up , the market is saturated with buying , big probability to broke the support

we will see a trend down sell the market

will the amazin AMAZON return to the highest value ?we make a pullback on a support , big probablity to market return

AMZN $AMZN AMAZON Possible down channelPossibly reached the top a channel, correlated with an upward channel @ $GOOG

AMZN couldn't breakoutAmzn is not looking good here , same with Q's altogether -- if 303 on QQQ breaks sell all tech positions until stabilized.

AMZN ShortReally rejected well on the 3350 today.

We should be pulling down tomorrow if we don't see strength pre-market and market is weak.

First tgt: 3250

Second tgt: 3210

AMZN Amazon Bearish Signals on Bullish Fundamentals In the Q4 institutional buys were 124B compared with 7.69Bil sells.

On 10/30/2020 JPMorgan Chase & Co. Boosted Price the Target price from $4,050.00 to $4,100.00

The Pharmacy business will be a long term growth catalyst for Amazon.

Their cloud service is growing too.

The Holyday sales will most likely surpass the last year`s.

The indicators are still bearish, i won`t buy yet, but wait for a breakout.

If you are interested to test some amazing BUY and SELL INDICATORS, which give the signal at the beginning of the candle, not at the end of it, just leave me a message.

AMZNAMZN/USD Broke out down Trend INC but might not last long due to the Support right under the Close for Friday.

Possible Head & Shoulders Pattern forming on FB and Amazon.Possible head and shoulders pattern on FB & Amazon - its not confirmed on both.

The ideal setup is that both decrease in value below the "neckline" marked in blue/red in each respective chart.

Although not guaranteed the price can then increase in value, coming back up to the neckline, where we see a rejection and continuation of the downwards breakout this is the confirmation area of the pattern, in extremely volatile markets we may not see a confirmation on the larger timeframes.

AMZN Inverted H&S Pattern formingAmazon (AMZN) appears to have a bearish inverted head and shoulders pattern forming. Final downside target of 2215 if it continues to play out.

Thoughts?

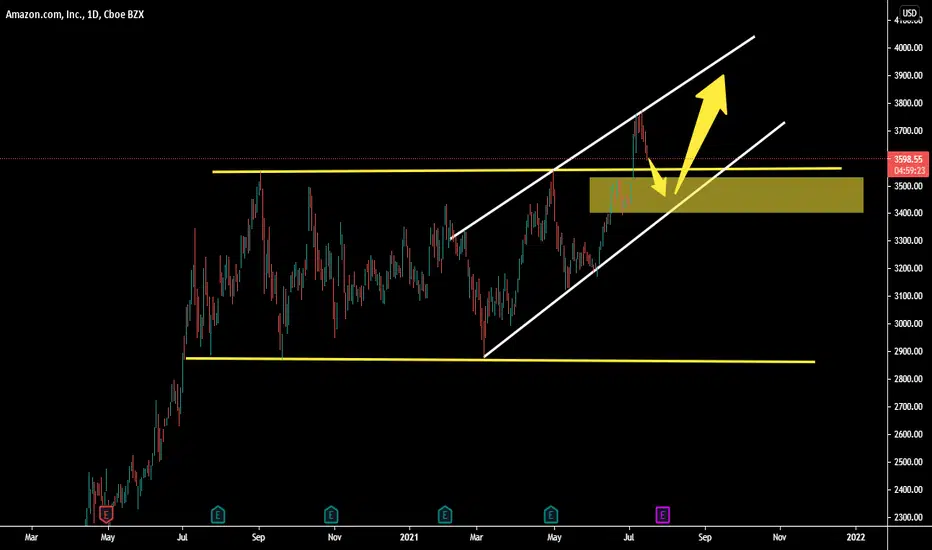

Amazon Rising WedgeSeems to be a large rising wedge which would make sense given the rate of increases.

AMZN Big Short coming out! First $3,270? Down to $2700...Amazon has seen some good upside recently, and that doesn't mean that cannot continue for the longer term. However, for the short term, we could see the stall of the most recent pop from 2,900 and the 100-day moving average and a retrace back down under that level along with the rest of the equity market into this Presidential election.

Amazon does have long term potential and medium-term potential from the potential closures due to COVID-19 again and also the holiday season coming up. People's number one option is jumping on Amazon and buying whatever they need. Not to mention the potential for a stock split on Amazon which could drive more money into the stock medium term.

However, with the current economic condition, we can see some volatility and a head and shoulders pattern form to completion when Amazon fails under the 3220 area and pushes through the support zone at 2900 which is the neckline. That would bring AMZN down to the 2670 area.

This idea is for educational purposes only and should not be taken as trading or investment advice.

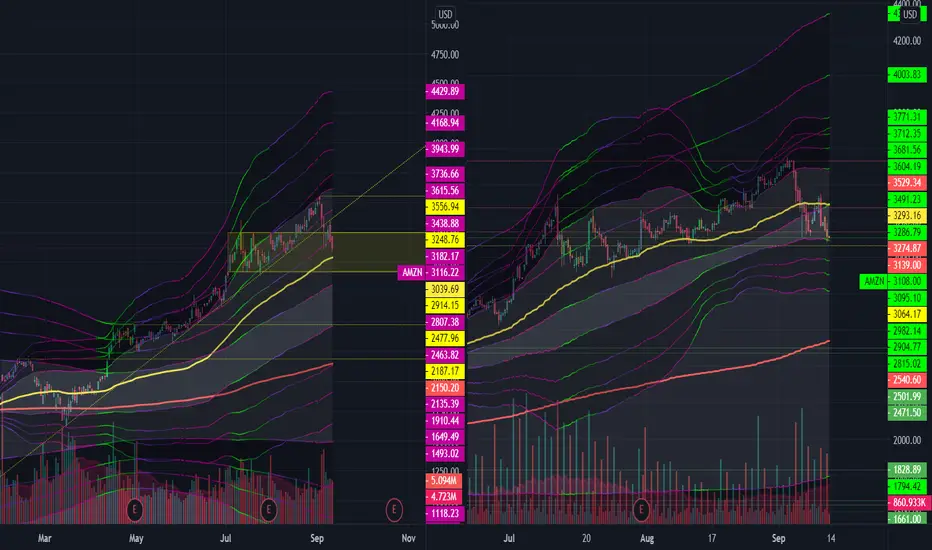

📫 AMZN 9/14-9/18 Trade Plan 🎁AMZN had a nice run pushing new ATH to @3552.25 and pulling back breaking the support trend line that has been holding since March.

LONG

Holding Above 3050

Target 3078, 3126, 3165, 3228 (Resistances)

SHORT

Holding Under 3042

Target 3018, 2994, 2947, 2912 (Supports)

AMZN looking for a new high, but swing traders be careful...The stock AMZN is consolidating in an ascending triangle , it is most probable that the market will look for 4038.05 (1.618 Fib level).

You need to wait for the confirmation of what I said by the breaking of the triangle from above.

Be aware of the negative divergence of RSI, another reason to wait for the confirmation of the increasing movement.

Finally, and most importantly, keep an eye on volumes they are what makes the market move, not prices.

AMZN ANALYSIS & FORECAST FOR THE NEXT DAYS Dear all,

Amazon may drop down to touch the black trend line below and then we will have a strong rebound to a very strong bullish trend,

Kind regards,

Amazon 3day Doji Movement. 2873 current range supports as we develop a doji candle. Want to look to see if this is Distribution

Look to play the breakout and confirm with the drop from overbought rsi and the ema dots to shoot red.

Neutral.

ANALYZE: AMZNafter all i notice on the chart my probability the trend going down to test the support line