BitMine Immersion Technologies (BMNR) AnalysisCompany Overview:

BitMine Immersion Technologies AMEX:BMNR is a crypto mining innovator leveraging immersion cooling to maximize mining efficiency and lower operational costs. Recently, the firm has pivoted from Bitcoin mining to Ethereum accumulation, positioning itself as a long-term Ethereum value play.

Strategic Drivers:

Ethereum Focus: Building exposure to the fast-growing DeFi, smart contract, and developer ecosystem.

Treasury Growth: Ethereum holdings have surged in value with ETH rising above $4,000 and peaking at $5,200 in 2025, creating significant unrealized gains.

Investor Confidence: Backed by high-profile investors, expanding revenues, and improving liquidity.

Capital Strategy: Launch of a $1B share repurchase program highlights management’s conviction and shareholder-first approach.

Investment Outlook:

Bullish above: $41–$42.

Upside target: $130–$135, supported by Ethereum accumulation, buybacks, and capital efficiency.

📢 BMNR—A high-beta Ethereum proxy with structural tailwinds from DeFi expansion and shareholder-focused capital allocation.

#BMNR #Ethereum #CryptoMining #DeFi #Blockchain #GrowthStocks #Buybacks

Growthstocks

Opera Limited | OPRA | Long at $16.68Opera Limited NASDAQ:OPRA is best known for its web browsers (Opera, Opera GX, and Opera One - which integrates advanced AI features and enhanced tab management). The company has expanded its portfolio to include mobile browsers, advertising technology, and other internet consumer products, positioning itself as a leader in delivering personalized and secure browsing experiences. With a focus on AI-driven tool and a growing user base, Opera serves millions of users worldwide, particularly in emerging markets.

The growth projections for NASDAQ:OPRA look great due to its expansion of AI-driven features, growth in advertising revenue, and penetration in emerging markets. Revenue is excepted to rise 15-25% year-over-year into 2026 and 10-20% year-over-year in 2027. NASDAQ:OPRA is extremely healthy, with a debt-to-equity of 0.01x, Quick Ratio of 2.43x, and extremely low bankruptcy risk. Also, there is a nice 4.7% dividend with share ownership. Low float: 83 million.

From a technical analysis perspective, the stock is (currently) bouncing off my historical simple moving average channel and has very strong upward momentum. While the price could enter my historical simple moving average channel in the near-term ($13-$15), I think the momentum is there to take it higher to fill the major gap on the daily chart between $26.25 - $26.98. It will likely take some time, but lower interest rates and new AI tools/news may fuel a positive rally long-term.

Unless, the market flips...

Thus, at $16.68, NASDAQ:OPRA is in a personal buy zone with short-term risk for a drop near $13.

Targets into 2028:

$22.00 (+31.9%)

$26.75 (+60.4%)

Qualcomm Inc | QCOM | Long at $156.60Qualcomm NASDAQ:QCOM is a global leader in wireless technology, focusing on 5G chipsets, AI-capable Snapdragon processors, and connectivity solutions for smartphones, IoT, and automotive. Revenue through 3 quarters of 2025 is ~$40B. Revenue growth is anticipated to be 10-12%, year over year (2026: ~$45B; 2027: ~$50B; 2028: ~$56B). 5G adoption, AI chip demand, and automotive needs should continue to drive the stock price. Earnings per share are projected to grow 12-14%, year over year (2026: ~$11.20; 2027: ~$12.80; 2028: ~$14.70). Thus, the future looks quite bright for NASDAQ:QCOM .

Regarding price, it is currently trading at a PE of 15x and has a 2.25% dividend. The price is resting just above my historical simple moving average channel. I do anticipate it to drop into the channel (down in the high $130's-$140's) in the near-term due to typical September selloffs. However, I plan on adding more in the zone. A major bear case would be a major drop into the $90's to fill the price gaps on the daily chart before moving higher. I do not think this will happen unless a major catalyst in the market emerges - but always be prepared. Regardless, it is a strong company providing products and services that are in high demand. Currently fairly valued, I believe it become undervalued as the demand for 5G and new phone chips with AI capabilities emerges.

Thus, at $156.60, NASDAQ:QCOM is in a personal buy zone with a likely near-term drop into the $130's and $140's.

Targets into 2028:

$191.00 (+22.0%)

$225.00 (+43.7%)

Protagonist Therapeutics (PTGX) AnalysisCompany Overview:

Protagonist Therapeutics NASDAQ:PTGX is a clinical-stage biotech developing peptide-based drugs in hematology, inflammatory, and metabolic diseases. Its pipeline spans polycythemia vera, psoriasis, and obesity — addressing multi-billion-dollar markets.

Pipeline & Catalysts:

Rusfertide (Polycythemia Vera) 🩸

Phase 3 VERIFY trial met all primary and secondary endpoints.

Showed reduced phlebotomy needs and improved hematocrit control.

Positions rusfertide as a first-in-class treatment and regulatory catalyst.

Icotrokinra (Psoriasis) 🌐

NDA filed for IL-23 receptor antagonist.

Approval could unlock a major dermatology revenue stream.

PN-477 (Obesity) ⚡

Expands PTGX’s reach into the fast-growing obesity market.

Strategic Advantage:

Global Takeda partnership enhances execution power.

Recent $25M milestone payment post-Phase 3 validates science & provides financial support.

Investment Outlook:

Bullish Case: Above $46–$48, driven by strong clinical data & regulatory progress.

Upside Potential: Target $78–$80, supported by trial success, NDA filings, and Takeda backing.

📢 PTGX—A high-upside biotech story with catalysts across hematology, dermatology, and obesity.

#PTGX #Biotech #ClinicalTrials #Obesity #Psoriasis #Takeda #GrowthStocks

Wix | WIX | Long at $124.35NASDAQ:WIX is a company with steady growth projections driven by AI adoption, market expansion, user acquisition, and a focus on profitability. For example, earnings are forecast to grow 28.24% per year. Analysts project NASDAQ:WIX to achieve approximately $1 billion in free cash flow by 2028. While the current P/E is around 47x, its Forward P/E ratio is approximately 18x (potentially undervalued). I truly believe the changing economy will shift individuals into more entrepreneurship (what else can they do?) and that will be the driving force behind user growth.

From a technical analysis view, the price recently bounced off from my historical simple moving average band (often an area for share accumulation / consolidation). While it may trickle down to close the price gap on the daily chart near $110 in the near-term, I think the outlook needs to be long-term here given the projections. The only issue I see is the current high debt for NASDAQ:WIX , but interest rates are absolutely coming down soon which will help ease the strain.

Thus, at $124.35, NASDAQ:WIX is in a personal buy zone.

Targets into 2028:

$175.00 (+40.7%)

$250.00 (+101.1%)

DPRO falling wedge breakoutDPRO has broken out of a falling wedge on the weekly. Ticker will respond well to Trump's "Big Beautiful Bill" which includes over $30 billion for defense/military spending. The drone company is already making progress with US military projects and is setting up for a strong rally.

TOM LEE leading the charge in this new BULL MarketThank you for providing excellent analysis,

being on the right side of the trade

and helping retail with your public speaking on your own channel, podcasts, and of course CNBC.

I wish you continued success in you Granny shots ETF which is already over $1.5 Billion in AUM!

ABCL — Bullish Breakout with Upside PotentialAbCellera Biologics Inc. (ABCL) has recently confirmed a breakout above a long-term descending trendline, followed by a successful retest of both the trendline and previous local highs. This technical development increases the probability of a sustained upward move.

The first target stands around $5.70, with a potential medium-term extension toward $13.20, offering attractive risk-to-reward parameters.

The company operates in the biotechnology and healthcare innovation sector — one of the most promising and rapidly advancing industries. While such stocks often face increased volatility due to news-driven events, the potential for high returns makes them compelling for both swing traders and long-term investors.

Lemonade, Inc. (LMND) – AI-Driven Disruption in InsuranceCompany Snapshot:

Lemonade NYSE:LMND is a tech-forward insurer reinventing traditional insurance through AI, data science, and a mobile-first experience across renters, homeowners, auto, pet, and life products.

Key Catalysts:

AI + OpenAI Integration 🚀

Collaborations with OpenAI are powering Lemonade’s RealTime API and AI voice agents, improving claims automation and customer support.

Enhances scalability and reduces overhead, key to long-term margin expansion.

Operational Resilience 🔥

Despite a $22M wildfire loss in California, Lemonade met Q1 guidance—thanks to robust reinsurance and effective risk management, underscoring operational maturity.

Auto Insurance Momentum 🚗

Car insurance was the top growth driver in Q1 2025, tapping into a multi-billion-dollar market where Lemonade still holds early-stage penetration.

AI-powered underwriting gives it an edge over legacy incumbents.

Investment Outlook:

Bullish Entry Zone: Above $38.00–$39.00

Upside Target: $65.00–$70.00, supported by AI innovation, product diversification, and scalable infrastructure.

🧠 Lemonade is not just selling insurance—it’s rewriting the rulebook on how it’s delivered, priced, and experienced.

#Lemonade #LMND #Insurtech #AIInsurance #OpenAI #DigitalTransformation #AutoInsurance #TechStocks #GrowthStocks #ClaimsAutomation #Reinsurance #Fintech #CustomerExperience

GRAB — Breakout Confirmation and Strong Upside PotentialGrab Holdings (GRAB) is currently forming a promising technical setup supported by a breakout from long-term consolidation. After printing a strong low and breaking out of a multi-year range, the price action confirms a bullish reversal with clear structure.

Technical Analysis

– Trendline breakout and bullish market structure shift

– Price is consolidating above the breakout level, forming a continuation zone

– Valid entries: market execution above $4.50 or limit orders near $4.00 support

– First profit target: $6.60 (around 40% growth)

– Second target: $10.15 (over 100% from entry)

The setup suggests increasing bullish momentum. A clean consolidation above previous resistance strengthens the case for a breakout continuation toward $6.60 and potentially $10.15.

Fundamental Backdrop

Grab is a Southeast Asian tech leader operating across ride-hailing, food delivery, and digital payments. The company continues to reduce losses, improve margins, and expand its fintech arm. With rising digital adoption in the region and a shift toward profitability, GRAB is gaining investor attention. Its most recent earnings report showed improving revenue trends and narrowing net losses — a strong signal of long-term sustainability.

Conclusion

Grab Holdings presents a well-aligned opportunity from both a technical and fundamental perspective. With a clear structure, breakout confirmation, and fundamental turnaround, this setup fits both swing and midterm investment strategies. Risk management is still key — stops should be placed below consolidation lows or key structure levels.

GH (Guardant Health) — Breakout Setup with Strong Upside PotentiGuardant Health (GH) is showing signs of completing a long-term accumulation phase and transitioning into a bullish trend. After breaking out of a major descending trendline and holding above key resistance at $38.30, the stock entered a tight consolidation range — a classic base formation before a potential breakout.

Technical Highlights:

– Confirmed trendline breakout

– Price is consolidating above previous highs

– Entry zone around $50–$51

– First target: $70 (+40%)

– Second target: $103 (+100% from current levels)

Fundamental Support:

Guardant Health is a leading precision oncology company specializing in liquid biopsy technologies for cancer screening and monitoring. The company continues to expand its product offerings, especially in early cancer detection — a market with huge long-term growth potential. Recent news includes positive developments in clinical trials and expanded partnerships, which could significantly boost revenue.

Institutional interest in GH has also been rising, with increased buying activity visible in the most recent 13F filings. The overall market sentiment toward biotech stocks with strong data pipelines is improving, which further supports the bullish outlook.

Conclusion:

GH is a strong candidate for medium- to long-term growth. The technical setup aligns with a fundamental narrative of innovation and market expansion. Partial profit-taking could be considered at $70 and $103. Due to the volatility of biotech stocks, proper risk management and position sizing are essential.

Rivian Kicking Off Potential UptrendHey, all. I'll get down to it. Obviously NASDAQ:RIVN has been an incredibly tough stock to own. Fake out after fake out. It has been brutal - unless you have been nimble enough to buy the dips and sell the rips.

I would like to posit, however, that NASDAQ:RIVN is going to start marching back higher here over time. In the signal system I have been taught via the T@M strategy, Rivian is putting in a range expansion to the upside on the weekly time frame. If you take the range of the past monthly consolidation period, attach it to the "mode" (or central zone of the consolidation range), it gives you a target of $25 over the next few months. Now, whether this is another fake out just to reverse on us... again... remains to be seen of course. It is early in the idea. But potentially offers a decent risk/reward position here.

I just do not see Rivian really going away at all and, if they can keep refining their business, they could see some success going forward. Anyway, hope you enjoy this idea! As always, position carefully as the market is risky business.

Including the Daily Chart below for your reference as well.

Uptrend Stock / Swing and Run Trend / SE (NYSE)Uptrend Stock / Swing and Run Trend

SE (NYSE)

Fundamental

Sea Limited operates in three highly attractive business segments:

Sea Money – The company’s digital financial services arm offers consumer and SME lending, mobile wallets, and payment processing services.

Shopee – The largest e-commerce platform in Southeast Asia and Taiwan, with strong market presence and growth.

Garena – The company’s digital entertainment division, providing access to popular mobile and PC games. It also promotes eSports. Garena has developed its own successful game titles such as Free Fire, a globally popular battle royale game.

Sea Limited's key strength lies in its integrated platform that combines e-commerce, digital finance, and digital entertainment under one umbrella. This synergy allows the company to cross-leverage its customer base—for example, using Shopee users to promote Sea Money's financial services.

Technical

The price has been forming accumulation patterns at the bottom and gradually rallying upwards.

It’s showing a sideways-up structure, where the price bases sideways and then continues to rally upward in steps.

This setup allows for buy-the-dip opportunities using an indicator called Regression Trend to identify the trading channel.

For swing trading, one could buy on dips near the lower support band and sell at resistance on the upper band.

As shown in the chart (with circles marked), I’ve been buying on dips along the way.

In the most recent phase, you can consider buying around $139. If the price breaks out, the next support levels to watch would be around $143 and $147.

Target prices:

First target: $150

Next targets: $160 and $170

Stop Loss:

If the price drops below $120 and breaks the price structure, that would be the stop level.

As the quarterly earnings announcement approaches, the price is rallying in anticipation, and it's showing strong momentum within an uptrend—very positive sign.

KRYSTAL Integrated Services LtdTechnical View: KRYSTAL is consolidating between ₹520–₹550 after a rally from March lows. A breakout above ₹560 could target ₹600+, while a dip below ₹500 may weaken momentum. RSI shows moderate bullishness.

Fundamental View: FY24 revenue grew ~44% YoY to ₹981 Cr; net profit rose ~26% to ₹48 Cr. ROE ~18%, ROCE ~20%. Recently secured a ₹349 Cr 3-year contract from Tamil Nadu Medical Services.

Action Plan:

Short-term: Buy above ₹560, target ₹600.

Long-term: Attractive valuation; accumulate on dips ₹450–₹500 zone.

Zai Lab (ZLAB) – Biotech Growth & Profitability PathCompany Overview:

Zai Lab NASDAQ:ZLAB , a leading Chinese biotech firm, is on track for non-GAAP profitability by Q4 2025, driven by strong revenue growth & cost management.

Key Catalysts:

Financial Discipline & Expansion 💰

Operating losses fell 45% in Q4 2024, highlighting cost efficiency while scaling operations.

Analysts project $2 billion in annual revenue by 2028, reinforcing long-term value creation.

Blockbuster Drug Pipeline 💊

VYVGART generated $93.6M in its first full launch year, demonstrating strong adoption.

KarXT & bemarituzumab are key upcoming growth drivers, expanding ZLAB’s market footprint.

Investment Outlook:

Bullish Case: We are bullish on ZLAB above $34.00-$35.00, supported by financial execution & product expansion.

Upside Potential: Our price target is $54.00-$55.00, driven by strong product adoption & long-term growth trajectory.

🔥 Zai Lab – Unlocking the Future of Biotech Innovation. #ZLAB #Biotech #GrowthStocks

Defensive Sector with Growth PotentialSupporting Arguments

Current Market Uncertainty Sustains Demand for the Defensive Sector. NEE represents the defensive utility sector. Given the current political and economic uncertainty in the market, there could be an additional catalyst for the company's stock price growth.

Demand for Green Energy from the IT Sector. More than 80% of the company's portfolio consists of renewable energy sources (RES). Demand from data centers in the IT sector may allow the company to outperform competitors.

Attractive Valuation Levels and Technical Outlook

Investment Thesis

NextEra Energy (NEE) has strong long-term growth prospects due to the increasing demand for RES and the electrification of various sectors. Their integrated business model, combining the regulated utility business FPL and the competitive renewable energy business NEER, ensures both stability and growth opportunities. NEE's leadership in RES production, along with investments in battery energy storage and gas infrastructure, allows the company to benefit from the growing demand for clean energy solutions.

Current Market Uncertainty Could Drive Stock Price Growth. Tariffs imposed by the administration on imports and their potential impact on the U.S. economy remain in investors' focus. The market has responded to high uncertainty with a significant correction in overheated sectors, and pressure may persist for some time. As a representative of the utility sector, NEE benefits from uncertainty and may continue its growth.

Demand for Green Energy from the IT Sector. The largest public companies continue to increase capital expenditures on AI infrastructure to stay competitive. A key component of such infrastructure is data centers, which consume large amounts of energy and contribute to increased environmental pollution. As a result, data center owners create strong demand for companies that provide access to RES. More than 80% of the company’s portfolio consists of renewable energy sources. Already, the company’s annual profit growth rate is twice as high as that of its competitors.

Attractive Valuation Levels and Technical Outlook. The company's stock is trading at the 200-day moving average and recently rebounded from the resistance line at the 50-day moving average, which could serve as a strong catalyst for movement toward the previous peak of $84.8. Based on the forward PEG ratio, the company is trading at about the same level as companies engaged in traditional energy sources for household supply, while maintaining profitability 5-15% higher than competitors. Based on the forward P/E ratio, the company appears cheaper than its closest direct competitors (18x vs. 20.5x).

Our target price is $82, with a "Buy" recommendation. We recommend setting a stop-loss at $64

TG Therapeutics (TGTX) – Biotech Innovation & Global ExpansionCompany Overview:

TG Therapeutics NASDAQ:TGTX is a biotech leader focused on novel cancer and autoimmune treatments, gaining momentum as an IBD Leaderboard and IBD 50 Top 10 Growth Stock.

Key Catalysts:

Regulatory Approvals & Expansion 🌍

BRIUMVI secured approvals in Europe & the UK, unlocking new revenue streams in key markets.

Strong Profitability & Growth 💰

88.3% gross margin ensures sustainable reinvestment into R&D and future pipeline advancements.

High-Growth Stock Recognition 📊

Technical strength is validated by its inclusion in top-performing stock lists, signaling strong investor confidence.

Investment Outlook:

Bullish Case: We are bullish on TGTX above $34.00-$35.00, driven by global expansion, financial strength, and biotech leadership.

Upside Potential: Our price target is $55.00-$56.00, supported by continued innovation and market penetration.

🔥 TG Therapeutics – Pioneering the Future of Cancer Treatment. #TGTX #Biotech #GrowthStocks

$CDRE: Cadre Holdings – Riding the Safety Wave?(1/9)

Good afternoon, everyone! 😊

NYSE:CDRE : Cadre Holdings – Riding the Safety Wave?

With CDRE at $30.20, is this stock a safe bet or a risky ride? Let's dive into the world of safety gear and see if Cadre's holdings hold up! 😎

(2/9) – PRICE PERFORMANCE

• Current Price: $30.20 as of March 12, 2025 😏

• Recent Moves: Down 11% from $34.02 a week ago 😬

• Sector Vibe: Safety equipment sector is growing, driven by stricter regulations and demand for safer workplaces. 📈

Short commentary: The stock's taken a hit, but the sector's looking good. Maybe it's just a temporary dip? 🤔

(3/9) – MARKET POSITION

• Market Cap: Approximately $1.23 billion 💰

• Operations: Manufacturing and distributing safety and survivability products for law enforcement, first responders, military, and now, the nuclear market. 🛡️

• Trend: Expanding into new markets with the acquisition of nuclear safety brands. 🚀

Short commentary: They're diversifying, which is usually a good sign. More markets mean more opportunities. 😉

(4/9) – KEY DEVELOPMENTS

• Acquisition of Carr's Engineering Limited's Engineering Division for nuclear safety solutions, announced on January 16, 2025. 📈

• Expected to close in the first half of 2025. ⌛

• Market Reaction: The stock has seen a recent dip, possibly reflecting integration concerns or broader market volatility. 😐

Short commentary: This should bring in new revenue streams and expand their international presence. Let's see how it plays out. 🌍

(5/9) – RISKS IN FOCUS

• Integration risks from the acquisition. ⚙️

• Supply chain disruptions. 🚚

• Regulatory changes in the nuclear sector. 📜

Short commentary: These are all things to keep an eye on, but every company has some risks. Stay vigilant! 🕵️

(6/9) – SWOT: STRENGTHS

• Strong reputation in safety equipment. 🏆

• Diverse product portfolio. 🌈

• Recent acquisition expanding into the nuclear market. 🌟

Short commentary: They're well-known and have a broad range of products, which is great. Keep up the good work! 👍

(7/9) – SWOT: WEAKNESSES & OPPORTUNITIES

• Weaknesses: Potential over-reliance on government contracts, integration challenges. ⚠️

• Opportunities: Growth in nuclear safety market, increasing global demand for safety products. 🌐

Short commentary: They need to manage their dependencies and make sure the acquisition goes smoothly, but there's a lot of potential for growth. Let's hope they nail it! 📈

(8/9) – CDRE at $30.20 – what's your call? 🗳️

• Bullish: Price could rise to $35+ soon, due to successful acquisition and sector growth. 🚀

• Neutral: Price remains steady, as the market digests the acquisition news. 😐

• Bearish: Price could drop to $25, due to integration risks and market volatility. 📉

Drop your pick below! 💬

(9/9) – FINAL TAKEAWAY

Cadre Holdings' $30.20 stance shows a robust portfolio and strategic expansion, but recent price dips and integration risks are concerns. Volatility’s our ally—dips are DCA treasure. Snag low, soar high!

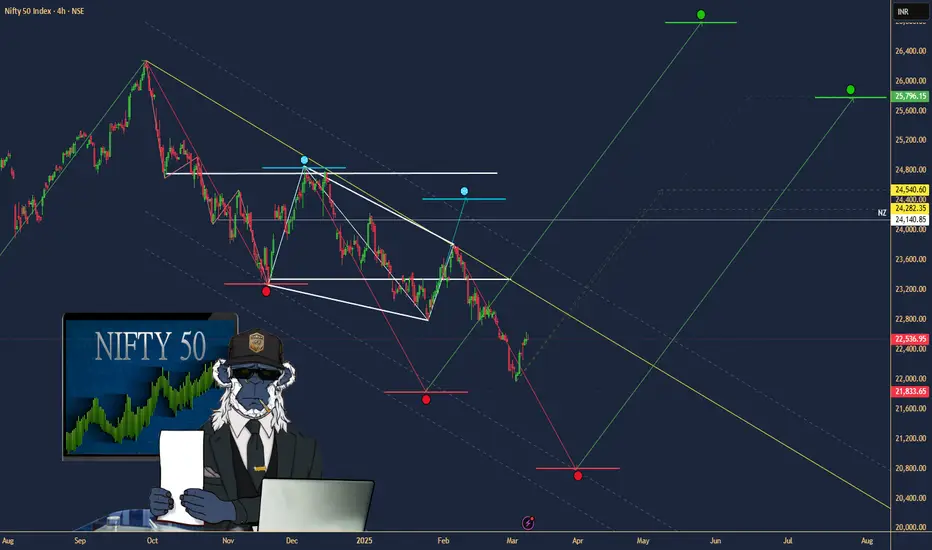

$NIFTY: Nifty 50 – India’s Market Meltdown or Hidden Gem?(1/9)

Good Morning, folks! ☀️ NSE:NIFTY : Nifty 50 – India’s Market Meltdown or Hidden Gem?

Gift Nifty’s at 22,555, down 65 points, and the index is off 13% since October 2024! Is this a crash landing or a golden ticket in disguise? Let’s unpack the chaos! 🔍

(2/9) – PRICE PERFORMANCE 📊

• Gift Nifty: 22,555, down 65 points (Mar 6, 2025) 💰

• Recent Trend: 13% drop from Oct 2024 highs 📏

• Sector Mood: Autos, real estate dragging, per web reports 🌩️

It’s a bumpy ride, but bargains might be brewing! 🔧

(3/9) – MARKET POSITION 📈

• Index Weight: 50 top Indian firms, 65% of NSE market cap 🏅

• Scope: Spans 13 sectors, from banks to tech ⏳

• Trend: Bearish streak persists, down 13% since Oct 🎯

Still a heavyweight, but feeling the squeeze! 🌐

(4/9) – KEY DEVELOPMENTS 🔑

• Earnings Slowdown: Growth at 5%, down from 20%+ 🔄

• Macro Woes: U.S. tariffs, trade tensions spook investors 🌍

• Market Vibe: Gift Nifty signals a sour start 📋

Tough times, but sectors might shine through! 💡

(5/9) – RISKS IN FOCUS ⚡

• Geopolitics: U.S. tariff threats hit exports 🔍

• Sector Slump: Autos, real estate under pressure 📉

• Volatility: Bearish trend grips tight 🌪️

Rough waters ahead, but storms pass! 🛡️

(6/9) – SWOT: STRENGTHS 💪

• Diversity: 13 sectors, broad economic play 🏆

• Scale: Tracks India’s biggest players 📈

• Value: Potentially undervalued, per web buzz 🔩

A battered champ with fight left! 💼

(7/9) – SWOT: WEAKNESSES & OPPORTUNITIES ⚖️

• Weaknesses: 5% earnings growth, macro drag 📉

• Opportunities: Sector plays in banks, tech shine 📈

Can it dodge the punches and rally? 🤔

(8/9) – 📢Nifty at 22,555 (Gift), down 13%—your call? 🗳️

• Bullish: $24K soon, undervalued steal 🦬

• Neutral: Flatline, risks offset ⚖️

• Bearish: $20K next, bears rule 🐻

Vote below! 👇

(9/9) – FINAL TAKEAWAY 🎯

Nifty’s 13% slide and $116 Gift price signal trouble 📉, but undervalued sectors tease upside 🌱. Volatility’s our mate—dips are DCA fuel 🔥. Buy low, aim high! Hit or miss?

BYD - What next post-earnings and the BoC's stimulus?HKEX:1211 has had a strong year in growth prospects, reporting solid earnings growth thanks to its robust EV sales and expanding footprint in international markets. The recent earnings beat highlighted an impressive increase in revenue, driven by the demand for both their electric and hybrid vehicles. But what we can notice is that the stock has only reflected this as a c.16% rise in price YTD. However, the question now is: where does BYD go from here?

- More recently, the BoC's latest stimulus measures, including rate cuts and support for the real estate sector, could indirectly benefit BYD. With increased liquidity and consumer confidence, domestic demand for EV's could rise, especially if coupled with additional green energy incentives.

- As for the earnings release, the markets reacted well, and with this new-found optimism in the markets, with both the SEE Composite Index SSE:000001 and the Hang Seng Index TVC:HSI up 5.78% and 9.28% in the past 5 days, is this the turn-around for China as a whole?

$COFORGE: Coforge Ltd. – AI Travel Tech Titan or Overhyped?(1/9)

Good afternoon, everyone! 🌞 NSE:COFORGE : Coforge Ltd. – AI Travel Tech Titan or Overhyped Split?

Coforge snags a $1.56B Sabre deal and a 1:5 stock split—shares spike 10%! Is this IT gem ready to soar or just riding AI hype? Let’s unpack the buzz! 🔍

(2/9) – PRICE PERFORMANCE 📊

• Recent Surge: Shares up 10% post-Sabre deal news 💰

• Stock Split: 1:5 split announced, boosting accessibility 📏

• Sector Trend: IT outsourcing on fire, per X posts 🌟

It’s a hot streak, fueled by big moves! ⚡

(3/9) – MARKET POSITION 📈

• Market Cap: Not specified, but shares soaring 🏆

• Operations: Global IT player, travel tech focus ⏰

• Trend: $1.56B deal lifts travel sector outlook 🎯

Firm, staking its claim in AI-driven IT! 🌐

(4/9) – KEY DEVELOPMENTS 🔑

• Sabre Deal: $1.56B, 13-year AI partnership 🔄

• Revenue Boost: Travel sector growth projected, per analysts 🌍

• Market Reaction: 10% jump, analyst upgrades flying 📋

Scaling up, with AI as the jet fuel! 💡

(5/9) – RISKS IN FOCUS ⚡

• Execution Risk: Big deal, big delivery pressure 🔍

• Hype Factor: AI buzz could overinflate expectations 📉

• Competition: IT giants crowding the space ❄️

High stakes, but risks are real! ⚠️

(6/9) – SWOT: STRENGTHS 💪

• Mega Deal: $1.56B Sabre contract, 13 years locked 🥇

• Travel Tech: Niche expertise shining 📊

• Split Appeal: 1:5 makes it investor-friendly 🔧

Loaded with ammo for growth! 💼

(7/9) – SWOT: WEAKNESSES & OPPORTUNITIES ⚖️

• Weaknesses: Execution hiccups could trip it up 📉

• Opportunities: AI adoption, travel sector boom 📈

Can it deliver or just dazzle? 🤔

(8/9) – 📢Coforge shares up 10%, $1.56B deal in pocket—your take? 🗳️

• Bullish: Skyrocketing on AI wings 🐂

• Neutral: Solid, but watch execution ⚖️

• Bearish: Hype outpaces reality 🐻

Drop your vote below! 👇

(9/9) – FINAL TAKEAWAY 🎯

Coforge’s $1.56B Sabre deal sparks a 10% surge 📈, with a 1:5 split sweetening the pot 🌱. Volatility’s our playground—dips are DCA gems 💰. Snag ‘em cheap, ride the wave! Goldmine or glitter?

Celsius Stock is a fast grower at a good priceCELH is a high growth stock that has finally found a fair price.

It has a popular brand and is now available everywhere, including costco.

Pepsi is partnering with them.

Now that its down 75%, it on my radar as a fairly price high growth stock.

so what, what can I expect.

What Im hoping when I get a grower, is 20-40% per year.

I covered Palantir when it was under 10, and now its over 100 only 2 years later, a 10x.

Could that happen here, I have no idea.

All we can do is look for good value and reduce our risk by finding quality.

Cheers.

UPSTART ($UPST): AI-DRIVEN LENDING ON THE RISEUPSTART ( NASDAQ:UPST ): AI-DRIVEN LENDING ON THE RISE

1/8 – REVENUE & EARNINGS BLAST

• Q4 2024 revenue: $219M (+56% YoY) 🔥

• Powered by a 68% jump in loan originations 💸

• EPS: $0.26, beating estimates by $0.30 (analysts expected -$0.04) 🚀

• Positive Adj. EBITDA—Upstart’s inching closer to sustained profitability 🏆

2/8 – BIG FINANCIAL EVENTS

• Strong focus on AI model innovation + expanding funding supply 🤖

• Management bullish on earnings call—AI improvements = growth catalyst 🚀

• Renowned for bridging lenders & borrowers via advanced, automated credit assessments 🌐

3/8 – SECTOR COMPARISON

• Some valuation measures say overvalued (e.g., GF Value ~$28 vs. market ~$65) 🧐

• Outpacing fintech peers like SoFi, PayPal, Ally in revenue growth 📈

• Profitability & multiples (P/E, P/S) lag behind due to recent net losses 😬

• Unique AI-lending angle may justify a premium—if it pays off 💡

4/8 – RISK ASSESSMENT

• Partner Dependence: A few big lenders = high exposure ⚠️

• Economic Sensitivity: Loan defaults rise if consumer conditions worsen 🌪️

• Regulatory Hurdles: Shifting financial rules could dent operations 🏛️

• Credit Risk: Holding loans on the balance sheet—watch out in downturns 💥

5/8 – SWOT HIGHLIGHTS

Strengths:

• Advanced AI for credit analysis 🤖

• High automation in approvals ⚡️

• Scalable via partner expansions 🌍

Weaknesses:

• Limited operating history ⏳

• Recent financial losses 📉

• Reliance on key partners 🤝

Opportunities:

• New loan products (auto, HELOC, etc.) 🚗🏠

• Expanding digital lending market 🌐

• Gaining market share as AI evolves 🔬

Threats:

• Fierce fintech competition 🏁

• Possible regulatory changes ⚖️

• Macro headwinds affecting credit demand 🌩️

6/8 – UN/UNDERVALUATION DEBATE

• Some see big future potential → undervalued by growth prospects 💹

• Others worry about multiples & an over-reliance on economic upswings 😬

• Recovery depends on broader economic rebound & strong risk management 🏦

7/8 Is Upstart a gem or a risk?

1️⃣ Bullish—AI lending will transform fintech 🏅

2️⃣ Cautiously Optimistic—Need more stability 🤔

3️⃣ Bearish—Valuation & macro risks are too high 🚫

Vote below! 🗳️👇

8/8 – STRATEGY WATCH

• Keep tabs on new loan products & partnerships 🛠️

• Monitor economic indicators (defaults, credit demand) impacting revenue 💼

• Regulatory shifts can either boost or bury AI-lending advantage ⚠️