The West Takes Aim at Russian Oil MarketsAs tensions continue to escalate between the West and Russia, a new development has emerged in the ongoing struggle over oil shipments. The West has been using shipping insurance as a tool to put pressure on Russia, but this strategy has had limited success so far. Insurance is only available for shipments valued at less than $60 a barrel, and as it happens, Russian oil already trades just below this cap. As a result, it's not yet clear how much of an impact this will have on oil prices.

But this raises an interesting question: why would the West set the cap at this level? The answer, it seems, is that they've calculated it in such a way that it provides just enough incentive for Putin to keep pumping oil. This is because the West is understandably concerned that Putin might choose to remove Russian oil from the international market, causing prices to rise significantly. And if global oil prices do rise much above where they currently are, the situation could become much more heated.

This is just one example of the complex dance that goes on between petronations and the West. On the one hand, the West has the ability to put pressure on petronations by limiting their access to the global market. But on the other hand, petronations have the power to put significant pressure on the West via energy prices. So it's a delicate balancing act, and it's not always clear who has the upper hand.

But what does this mean for the future? Well, it's difficult to say for certain, but it's clear that the West is trying to find a way to put pressure on Russia without causing a major disruption in the global oil market. And if they're successful, it could have significant implications for the ongoing struggle between the West and Russia.

Of course, there are many other factors at play here, and it's impossible to predict exactly how things will unfold. But one thing is clear: the discussion around this issue is only going to become more heated as global oil prices continue to fluctuate. So it's definitely a topic worth keeping an eye on in the coming months and years.

Russia

CL back to $90 a barrel?Following price cap on Russian oil, Opec+ is likely to cut oil supply for the second time.

Technically, CL has broken above the downtrend resistance and now in a correction wave.

Getting filled at $77 will give us the ideal RRR in this trade.

Brent Crude OIL (01.12.2022) InterdayCan see some higher highs on the daily we need to close above 90.5. Possible rejection of of that level and continuation to the downside.

CEIX Consol Rally to $60 for Local Coal Cycle Toptry and be patient with this one. Geopolitical headlines will move it fast in this thin volume topping structure.

await a run up near 60 and then play for downside

strong fundamentals:

finviz.com

Greenlight Capital also discussed CONSOL Energy Inc. (NYSE:CEIX) in its Q2 2021 investor letter. The fund said:

“Thermal Coal and Natural Gas

ESG investing is inflationary, as green energy is simply more expensive than hydrocarbons. Hydrocarbon energy companies are starved for capital and are being told to change their ways. The result is less exploration and drilling. Even with benchmark oil prices surging over the last year, companies are loath to drill more. Normally, the cure for high prices is high prices. With ESG in the proverbial driver’s seat, we might need much higher prices still in order to increase investment to meet demand.

There is almost nothing less popular than thermal coal. From 2011 to 2020, U.S. coal production declined by 51%. U.S. demand has fallen as we’ve shifted to alternative sources of electricity. As unpopular as coal is though, it still makes up about 20% of U.S. electricity generation. Globally, coal demand is growing modestly as China and India add power generation capacity faster than the West is reducing it. Even so, reduced oil and gas drilling has caused natural gas prices to advance and coal prices are following. Seaborne thermal coal prices are up 140% year-over-year and at the highest levels since 2011, and Northern Appalachia thermal coal prices are catching up, rising 23% in the last month alone.

We own CONSOL Energy (CEIX), the lowest cost, most efficient miner in Appalachia, which is poised to benefit from rising coal prices. It trades at 12x consensus earnings estimates that look stale to us, as they do not reflect recent coal price gains.”

Supply risks point to higher oil pricesOil prices were whipsawed this week with swings of more than 6%1 after a report from the Wall Street Journal suggested that Organisation of the Petroleum Exporting Countries (OPEC+) is looking to possibly increase output by 500,000 barrels per day (bpd). The rumour could have easily been justified by President Biden’s decision to offer sovereign immunity to the Saudi Crown Price Mohammed bin Salman in a civil lawsuit, as geopolitics could influence decisions. However, the Saudi’s shortly denied the report that OPEC+ was not considering an output increase, helping oil prices claw back losses on the day. This makes logical sense, given that OPEC+ reduced its oil production noticeably since the beginning of November, in accordance with its early October decision. The price action on 22nd November goes to show that it takes only a small amount of movement in trades to cause a large price effect in oil. The oil market remains susceptible to further volatility amidst a backdrop of low liquidity into year end.

Looking ahead, the oil market remains vulnerable to a number of key events starting with the OPEC+ meeting on Dec 4 followed by the European Union (EU) embargo on Russian oil alongside G-7 plans to launch a price cap on Russian crude sales on Dec 5.

Price cap on Russian oil is hardly bearish

Expectations are that the G-7 will soon announce the level at which they intend to set the price cap on Russian oil. The latest reports suggest a cap of US Dollar 65-70 per barrel, which would be well above Russia’s cost of production. Russia is already selling its crude at a significant discount, so a cap at these levels would likely have minimal impact on trading and inflict minimal harm to Russia. Russia’s Deputy Prime Minister Alexander Novak has once again made it clear that Russia will not supply crude oil or refined products to countries which follow the G-7 price cap. In fact, oil will either be redirected to those nations who choose to ignore the price cap or Russian output will be reduced. This appears to be more supportive for higher prices. So far, EU diplomats are locked in negotiations over how strict the Russian mechanism should be, after Poland and Greece rejected the proposal. They would prefer to see a cap closer to the cost of production at US$30. EU leaders are now expected to seek a deal at a 15-16 December summit, in follow up to the energy minister meeting this week on 24 November.

EU embargo on the import of Russian oil is approaching fast. This comes into effect on 5 December for crude oil and 5 February 2023 for oil products. In the last three months, Russia has remained the largest external supplier of diesel to the EU, delivering 540kbd2. According to IEA estimates, the EU was still importing 1.5mbd of Russian crude oil in October, which corresponded to just under 15% of total EU crude oil imports. In the coming months, the EU will need to find alternative suppliers. Replacing these supplies is not going to be easy. Russia will need to find other buyers leading to further uncertainty on the oil markets. India, Turkey and China have increased their purchases of Russian oil, thereby enabling Russia to continue exporting large quantities of oil.

Weak demand dominating sentiment on the oil market

Oil prices are down nearly 35% from its peak as sentiment remains dominated by concerns over weaking demand as the global economy enters a recession alongside an unprecedented release from the US Strategic Petroleum Reserve (SPR). Net speculative positioning in WTI crude oil futures is more than 1-standard deviation below the 5-year average underscoring extreme bearishness on the oil market3. Its worth noting that speculative positioning in oil was on a downtrend prior to the peak in oil prices. That indicates for one investors were probably taking profits on earlier holdings and higher volatility in oil market kept buyers at bay.

Although in a severe recession, oil demand can decline sharply, we are anticipating a much shallower recession for both the US and Eurozone economy. In the middle of the year, China’s oil demand was hit severely by lockdown restrictions, with demand falling below April 2020 and 2021 levels by 1-2mbd4. Although their remains uncertainty about China re-opening, we expect oil demand to recover from Q2 2023 onwards and accelerate towards year end. This should help oil demand from China grow in contrast to the prior two years.

Conclusion: The oil market still seems structurally undersupplied over the next few years. The International Energy Agency (IEA) assumes by the end of Q1 2023 oil production will be 2mbd lower than prior to the invasion of Ukraine. We expect the Chinese re-opening, Russian supply risk, the end of SPR releases and lower levels of investment in the energy sector to contribute to a tighter oil market in 2023.

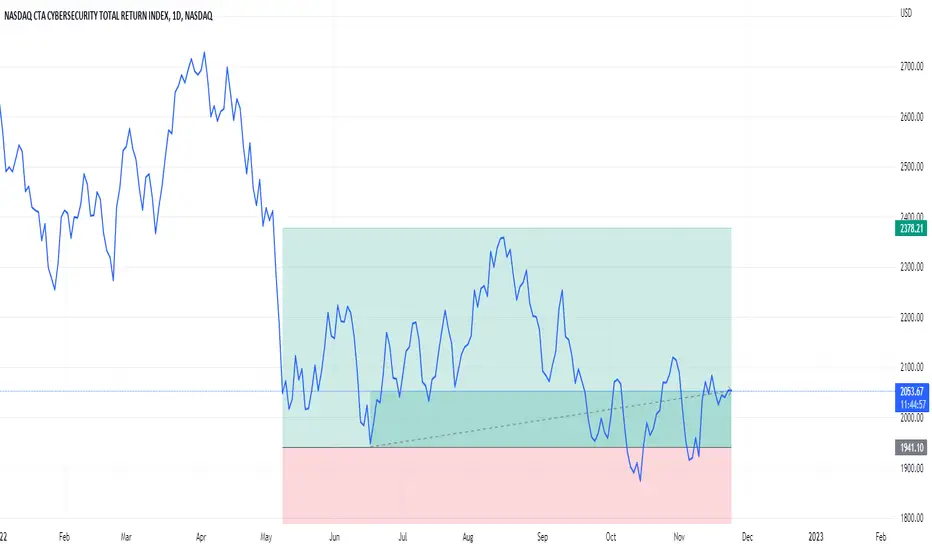

Have you experienced ‘Tool Sprawl’ in Cybersecurity?We recognise we have a diverse array of readers, probably some individual business owners, some employees of large companies, some employees of smaller companies and possibly even some people who are retired or between jobs.

Whatever your situation—how many different cybersecurity tools are you aware of that you interact with? A password manager? A single-sign-on interface? A specialist tool focused on email? Another specialist tool focused on accessing a cloud computing infrastructure?

The fact of the matter is that the more you learn about cybersecurity, the more you are awakened to a large number of providers that each specialise in different types of protection. We saw the term ‘tool sprawl’ used to describe the 2022 cybersecurity landscape—we thought it painted an informative picture1.

How many tools are customers using?

Enterprise customers may be managing portfolios of 60-80 tools, with those on the extreme higher end of the spectrum possibly managing up to 1402. Imagine managing all of these tools over the course of a normal business operation.

One reason why the current environment is characterised by so many tools could relate to the progression of the Chief Information Security Office (CISO) role. 10 years ago, the way a ‘good CISO’ was defined largely had to do with buying and deploying tools. The CISO in 2022 is now much more a top priority for a company’s board and C-suite, and now a ‘good CISO’ is evaluated based on outcomes rather than deploying tools3.

A survey conducted by Gartner found that 88% of Boards of Directors view cybersecurity as a ‘business risk’ rather than a ‘technology risk4.’

Of course, the attack surface in 2022 has also massively expanded, and frequently companies may be launched around new types of artificial intelligence and machine learning techniques, to use one example that could also lead to the proliferation of companies.

Dealmaking is already taking off in 2022

Through 18 August 2022, private equity sponsors and their portfolio companies have backed 162 cybersecurity deals worldwide, valued at $34.9 billion. If this pace continues, it could surpass 2021’s tally of $36.4 billion across 308 transactions5.

One driver—valuations. 2020 and much of 2021 saw the most newly public cybersecurity companies, many of which were focused on the cloud, experience massive multiple expansion and therefore premium valuations. The growth was strong, but the prices were not inexpensive in an environment where the cost of capital had been very low for a very long time.

With the rise of inflation and then the shift in policy of many central banks going from expansionary support of growth, many of these companies experienced dramatic multiple compression. This allows private equity players focused on building consolidated product offerings to pick up interesting companies at much lower prices.

Thoma Bravo is one such player that has been quite active. Just in the identity space, Thoma has done deals to acquire Ping Identity for $2.8 billion and SailPoint for $6.9 billion6.

Consolidation is a big desire from customers—possibly a response to the ‘tool sprawl’ that we mentioned earlier. There is a feeling in the market that there might already be too many companies, so it’s not just about more innovation but also building integrated platforms so customers can go to one place and get more services.

Option3 is an example of a firm that has shifted from funding new firms to acquiring late-stage middle-market companies for buy-and-build strategies. They are planning to raise a $250 million buyout fund dedicated to a platform acquisition strategy7.

Private equity firms are attracted to cybersecurity companies for many reasons, but it is noted that they have exhibited lower churn rates than other Software-as-a-Service (SaaS) businesses. They also have tended to generate high margins.

What about the slowing economic environment?

As is the case with many things, historical comparisons can only take us so far. If we think about the state of cybersecurity in 2007-2009, encompassing the ‘Great Recession’, it was totally different. Cybersecurity budgets are much different in 2022 than they were in 2007 heading into that significant slowdown8.

One doesn’t need to look too far to see quotes from experts indicating that even if cybersecurity spending could be impacted by a slower economic environment, it most likely wouldn’t be as impacted as other areas. There are many things that are regulatory requirements or viewed as ‘table stakes’ to the ongoing operation of companies, which make them that much more difficult to cut.

Regulators are also upping the ante. The Securities and Exchange Commission in the US has explored a rule that would require disclosure of a ‘material cybersecurity incident’ in a public filing. Disclosure would also have to be quite quick after the event—possibly a response to certain types of attacks and breaches like SolarWinds, where months after the fact the scope of potential damage was growing and growing9.

Even if regulators do not mandate spending more on cybersecurity, their pursuit of certain types of rules would be likely to have that impact.

Conclusion: a megatrend for all seasons?

Norges Bank Investment Management, the world’s largest sovereign wealth fund at $1.2 trillion, recently indicated that cybersecurity is their biggest current concern, citing that it faces an average of three serious attacks each day. The fund sees roughly 100,000 attacks per year, and they classify about 1,000 of them as serious10.

Firms operating in the financial industry have been increasingly targeted, and firms operating in the Nordic region feel the proximity to Russia during the Ukraine conflict quite tangibly.

While many investment themes might be a bit discretionary or susceptible to delays in a slowing economic environment, cybersecurity is not one of them. We may not know the exact companies or services that will grow the fastest but backing away from focusing on security is not an option.

Sources

1 Source: Alspach, Kyle. “Thanks to the economy, cybersecurity consolidation is coming. CISOs are more than ready.” Protocol. 17 June 2022

2 Source: Alspach, 17 June 2022.

3 Source: Alspach, 17 June 2022.

4 Source: “Gartner Survey Finds 88% of Boards of Directors View Cybersecurity as a Business Risk.” Gartner. Press Release. 18 November 2021.

5 Source: Shi, Madeline. “PE dealmaking thrives in cybersecurity sector.” Pitchbook. 23 August 2022.

6 Source: Shi, 23 August 2022.

7 Source: Shi, 23 August 2022.

8 Source: Alspach, Kyle. “Cybersecurity spending isn’t recession-proof. But it’s pretty close.” Protocol. 6 June 2022.

9 Source: Alspach, Kyle. “’Game-changer’: SEC rules on cyber disclosure would boost security planning, spending.” VentureBeat. 10 March 2022.

10 Source: Klasa, Adrienne & Robin Wigglesworth.” Financial Times. 22 August 2022.

USOIL Long term forecast Don't forget From December, the EU and G7 also want to cap the price countries pay for Russian oil. They are telling importers of Russian crude oil that western insurers will not cover oil shipments if they pay more than the cap. and also we have OPEC meeting in the beginning of December

NGAS BULLISH TREND REVERSALNGAS - As observed in previous heating seasons across EU, US, and Central Asia, there is a strong possibility of raising the demand for Natural Gas, instabilities in delivering, producing, and trading the blue fuel may soon lead to a not-so-cheerful holiday season in the EU and the UK. Panic is raising and if Russia decides to continue cashing on that fear, we might see new highs concurred on the spot market.

Risk Disclosure: Trading Foreign Exchange (Forex) and Contracts of Difference (CFD's) carries a high level of risk. By registering and signing up, any client affirms their understanding of their own personal accountability for all transactions performed within their account and recognizes the risks associated with trading on such markets and on such sites. Furthermore, one understands that the company carries zero influence over transactions, markets, and trading signals, therefore, cannot be held liable nor guarantee any profits or losses.

US PPI data and wayward projectiles affecting EUR/USDThe Euro has lost some ground against the US dollar after reports that Russian missiles had struck inside the Polish border killing two polish citizens.

The reason for the drop in the Euro is because Poland is a NATO member and the potential results of this, yet unverified report, is a retaliation from Polish and/ or NATO forces. Poland has previously noted that they are ready to defend their sovereignty in the face of accidental or purposeful attacks within its borders which could induce NATO forces to join in on the conflict too. NATO and US authorities are currently investigating the report before commenting publicly. It could be that markets wait for confirmation from these two authorities before considering their risk appetite for the Euro the rest of this week.

The Euro is still up against the greenback but was registering greater gains before the missile report hit the news flow. The reason for the strength in the Euro is due to the US Producer Price Index (PPI), a measure of wholesale inflation, coming in softer-than-expected. October’s PPI rose +0.2% month-over-month in October of 2022, below market forecasts of +0.4% adding fuel to the theory that inflation in the US has peaked and is now slowing. The EUR/USD was heading toward 1.0500 before investors were spooked by the missile report, sending it as low as 1.0280. It has since recovered to close to the 61.8% Fib level between this recent high and low

Previously, the EUR/USD rallied after the release of the US consumer inflation data (on November 11th) which was the first indicator that US inflation has reached its peak. The EUR/USD is still up 2.7% over the week.

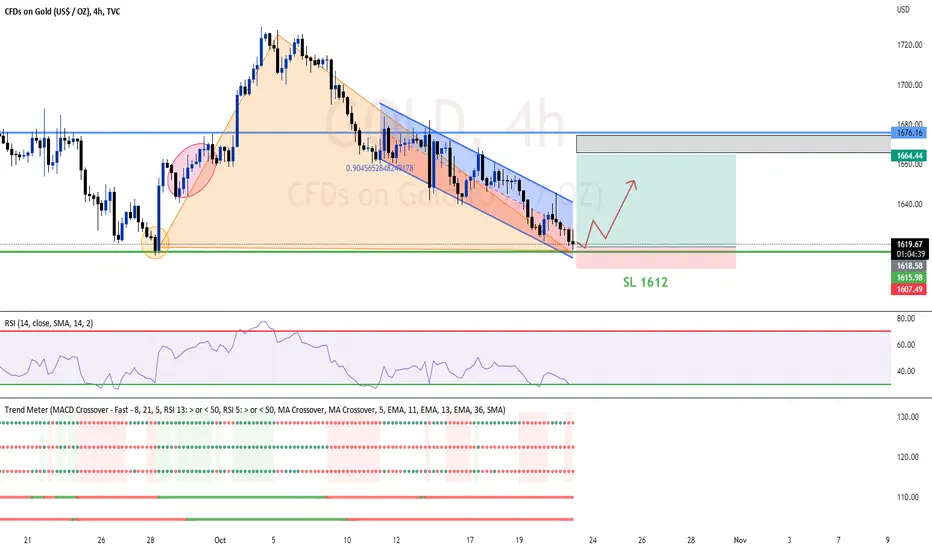

XAUUSDHello traders.

Gold is continuing to create Higher Highs and preseserves Higher Lows.

If you look on the left of past chart depiction, the area of 178x has been considered a former resistance like the 179x.

Finally, the price last August touched 1803 level and fell vigorously.

So, every possible entry at these levels could be profitable. But, the safest place to place the SL I strongly believe is above 1803 area.

We all know what gold can do with spikes. Regarding of spikes, the price action is indicating the weakness to go higher for short - term.

Traders Dynamic index has created a divergence with Price movement, but this doesn't mean that it will sell immidiately.

It can go further for some time, this is the reason I consider both 179x and 180x nice areas for sell - close to the Daily supply zone, where many pending orders will be open. A break above 1812 I think it may push price higher to 1840 - 1860 levels.

1750 area can be considered a safe zone for first TP and maybe a good entry for buys but the main key area is 1730, for strong buy.

Breaking news some moments ago informed humanity about a missile attack to some village of Poland. If this was not an accident and it was made by design, prepare to see gold rocketing above ATH!!!

Good luck!

Oil Technical analysisKey support level has been held, next stop 108/107.

Last local resistance must be. broken next week and held above.

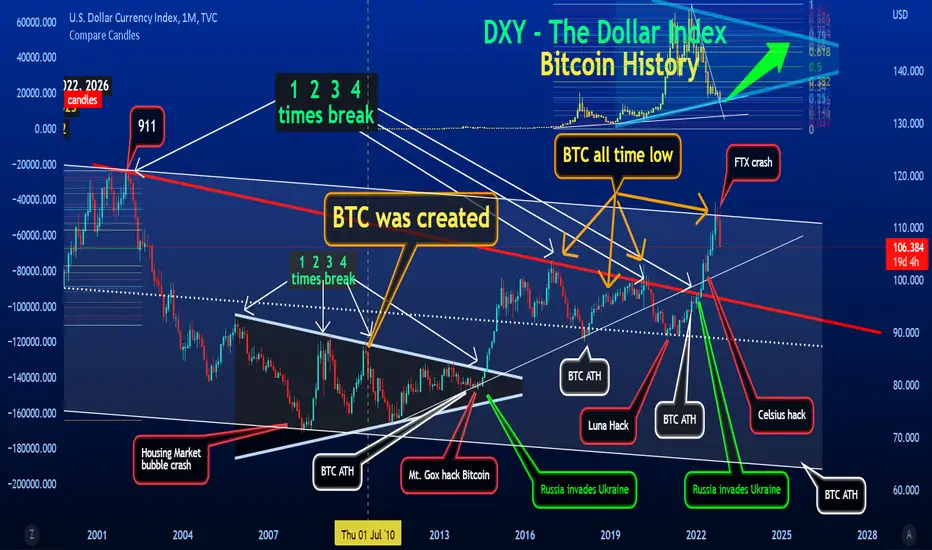

DXY with BTC historyHere you can see that the 4 year BTC cycle lines up well against the oposite corelation against DXY. So much history in 20 years with some important major events to gander at.

Why does the DXY drop when FTX files bankruptcy? So many questions about why the DXY moves the way it does.

Is this the Bitcoin bottom? Not according to the 4 year cycle. We could be headed into a bull trap in the next 4 months.

How far will it go?

50k is possible if you take a symmetrical triangle.

38k is highly likely if you are using the Fibs,

30k is an absolute if you take into count the BTC LONGS have to have to exit their liquidity.

The break even point for the millions of long positions put in is around 30k to break even.

When LUNA was hacked that is when a massive amount of longs went in. When Celsius got hacked another set of missive longs were added.

Whats the next all time lows?

10k, there is 1 open CME gap on the daily that hasn't been filled yet

7.5k, This is the last lowest trend line as well as the .886 fib which would conclude our "90% drop from all time highs"

Whats the next all time high?

hard to tell. I'm guessing 124k from that 7.5k, then a drop 50% back down to 70k, then up to 224k.

Check this chart in Dec of 2024 to see if 124K is then next BTC top

EURUSD 4H trend analysis. '''''''This is NOT a financial advice""""""

In this pair, the price can still touch 0.98 area before continue its journey on formed channel since early september. Meanwhile European countries are preparing themself for coming winter and of course Russia will use this opportunity to put some pressure on EU to get off of some sanctions. that means Euro zone is now fighting with a energy crises and i don't see this pair move above 1.0 anytime soon.

BCO Technical Analysis (Day trade)Overall bullish trend although we might have one more pullback to 97.2.

Big size entry tight stop loss

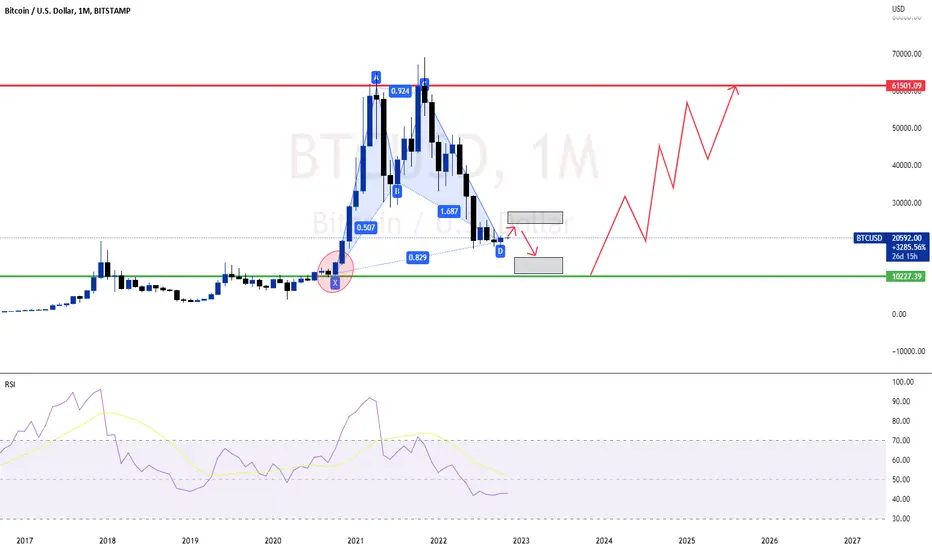

bitcoin to 12k in 2023 soonBelieve it or not, Bitcoin on the monthly frame says that we are at the end of Bitcoin's decline, and we will go down to the bottom and then head to higher levels!

Buy gold to 1699Pay attention to the market and news before trading please The situation is very embarrassing

Strong Reversal SPY/SPX IHFundamentals: Slowing growth from Google and Microsoft continued our confirmation of a slowing macro environment. Microsoft reporting slowing growth in cloud revenue. Google even said their strongest ad flow of "search" saw a decline in revenue. Ad spend being the canary in the coal mine indicates the market is ready to continue it's collapse. META continues to blow through cash to build the metaverse.

-3 month/10 year yields inverted

-Yields/Dollar continue their climb - taking a break the last couple of days.

-BOJ intervention

-Canadian central bank increasing just .5

-Chinese Xi reigns again and this time with complete dominance - Speaks of a great challenge ahead - Taiwan in the crosshairs

-Russians talking nuclear attacks

Technical Analysis: The low from Sept 6th, the downward sloping trendline from August 26th, the 50 day MA, combined with the upward trend line from the recent lows created a strong resistance after a 3.5 day run up. ES1! futures stopping a few ticks below 3900. 3 day pumps are the norm.

-Gap at 408.6, 200 MA and downward trend line from the ATH creating the next target to the upside.

Outlook: I definitely believe there is more downside ahead for the markets into 2023. Although today's price action and macro indicators are pointing down that does not guarantee we have seen the end of this rally. Upside gap to 408.6 is being eyed by the bulls. Perhaps by no coincidence the 200 MA is closing in on that price. Those combined with the downward trend line point to a mid November rally adjourning. Bulls looking to load back up around 375 SPY. Breaking through 375 shows the bears have gained control and we have entered into a longer correction formation or new wave down.

Buy Gold TodayHello, we will see a rise in gold soon. I hope everyone suggests caution when trading. Good luck

buy bitThere is a rise or correction in Bitcoin Please be careful when you trade and the news is very important also I wish you a good day and SL : 19121.5

LMT Lockheed Martin Options Ahead Of EarningsLooking at the LMT Lockheed Martin options chain, i would buy the $405 strike price Calls with

2022-11-18 expiration date for about

$9.50 premium.

Looking forward to read your opinion about it.

sell goldSelling gold, there is a slight correction, and then it returns to its position. I wish you a nice day

ETHUSD SELL TODAYEthereum analysis today is a simple but effective analysis. I wish you a happy trading day and a happy holiday