Our opinion on the current state of LIFEHC(LHC)Life Healthcare (LHC) is the second-largest, JSE main-board listed, healthcare company with private hospitals, same-day clinics and surgeries and healthcare companies in South Africa, the UK (Alliance Medical), and Western Europe.

The out-going CEO, Shrey Viranna, says that the group is trying to diversify away from conventional hospitals more towards day-clinics and non-acute services. It is also trying to diversify away from medical aid schemes towards people who pay for their medical attention out of their own pockets. They have launched MyLife Clinic which offers a consultation and basic medication for R300.

In its results for the year to 30th September 2023 the company reported revenue up 10,3% and headline earnings per share (HEPS) down 16,9%. The company said, "The Group's SA operations experienced strong demand for their services in the current year driven by the Group being the preferred network provider for medical aids. This led to higher utilisation of the Group's hospitals and complementary services which delivered PPD growth of 9.5%."

In a trading statement for the six months to 31st March 2024 the company estimated that earnings per share would increase by more than 20% due to the disposal of Alliance Medical Group. This will not affect HEPS, however.

In its results for the year to 30th September 2024 the company reported revenue up 12,7% and headline earnings per share (HEPS) up 73,4%. The company said, "NEPS, which excludes non-trading related items, increased by 48.5% to 132.3 cents (2023: 89.1 cents). The LMI RM2 transaction contributed 30.1 cents net after tax."

In a trading statement for the six months to 31st March 2025 the company estimated that it would make a headline loss of between 150,9c and 158,7c compared with a profit of 65,2c in the previous period.

Technically, the share peaked at R47 in September 2014 and then entered a long downward trend. It is now trading for around 1380c and is on a P:E of 10,6. The multiple reflects the share's defensive nature and its overseas diversification – which gives it some rand-hedge characteristics. It has not yet broken up through its long-term downward trendline.

In our view, this share looks like reasonable value.

Our opinion on the current state of M&R-HLD(MUR)Murray and Roberts (MUR) is a large South African construction company which has suffered from the sub-prime crisis and then the slump in construction spending following the 2010 World Cup. This brought the share down from a massive double-top formation at around R100 per share to a low below R5 in May 2020.

The company has been consolidating and reducing costs. It has transformed itself into a "...multinational engineering and construction Group focused on the natural resources market sectors..." with three primary business platforms – underground mining, oil & gas, and power & water.

On 27th March 2023 the company announced that it had sold its Australian operations (65% of Insig Technologies) for A$1 and so disposing of A$7m in liabilities.

On 8th December 2023 the company reported that it would be able to reduce its debt from R2bn in April 2023 to R350m as a result of "Cementation Canada Inc's recently renewed banking facility agreement with a Canadian bank will provide for Cementation Canada to pay CAD40 million."

In its results for the six months to 31st December 2024 the company reported no revenue and a loss of 167c per share. MUR remains a relatively risky penny stock with high debt levels.

On 15th July 2024 the company announced that it had won a $200m multi-year contract in Latin America.

On 22nd November 2024 the company's board of directors said that the company met the Companies Act definition of being "financially distressed" and that the best way forward was to enter into business rescue. Accordingly, trading in the company's shares has been suspended on the JSE.

On 20th January 2025 the company reported that it had obtained an additional R250m in funding.

In an update on 3rd April 2025 the company reported, "The date set by the Business Rescue Practitioners ("BRPs") for creditors of MRL to vote on the Business Rescue Plan ("the Vote") is Tuesday, 08 April 2025."

Our opinion on the current state of PURPLE(PPE)Purple Group (PPE) is a trading platform and asset management company that is aimed mainly at the private investor and offers the cheapest costs of dealing in shares on the JSE.

The company has three divisions: (1) Easy Equities which enables investors to buy very small quantities of shares with very low dealing costs. For example, buying R100 worth of a share costs the investors just 64c. 95% of accounts opened are first-time investors and the company has 150 000 active investors. (2) Emperor Asset Management which manages funds on behalf of clients and (3) GT247, a derivatives trading platform.

On 18th May 2023 the company announced the finalisation of its rights issue to raise R105m and already had the support of more than 27% of its shareholders. Shareholders will be offered 10,20567 new shares for every 100 shares that they already hold at a price of 81c per share. The offer is at a 31,87% discount to the volume-weighted average price (VWAP) of the 7 days ending 16th May 2023.

In its results for the six months to 28th February 2025 the company reported revenue up 25,8% and headline earnings per share (HEPS) up 204,1%. The company's net asset value (NAV) increased by 9% to 45,35c per share. The company said, "Client deposits are rising, though not yet back at peak levels – signalling that further upside remains as clarity returns to global markets."

The share is well traded with an average with over R1m worth of shares changing hands daily on average. The share has made a "double top" formation at around 340c in the first half of 2022 and then fell until the beginning of March 2024. Since then it has been rallying.

We advised applying a 65-day exponentially smoothed moving average and waiting for an upward break – which occurred on 4th March 2024 at a price of 66c. It has since risen to 105c.

We believe it still has significant upside potential.

Our opinion on the current state of TREMATON(TMT)Trematon (TMT) is an investment holding company with subsidiaries, joint ventures and associate companies, mostly in the Western Cape. The company also invests in listed and unlisted shares.

Originally most investments were related to property, but its investments have moved outside that. The company owns Club Mykonos.

In a trading statement for the six months to 28th February 2025 the company estimated that HEPS would fall by between 17% and 25%. The company said, "INAV per share for the current period to be between 335 cents and 345 cents, which is between 18% and 15% lower than the previous interim period's 408 cents."

The share has only about R80 000 worth of shares changing hands each day – so it is marginal for private investors.

While this share is in a downward trend, we believe that it could become a worthwhile investment if it expands its growth in the education business and improves the volume traded, now that the pandemic is behind us.

Our opinion on the current state of PURPLE(PPE)Purple Group (PPE) is a trading platform and asset management company that is aimed mainly at the private investor and offers the cheapest costs of dealing in shares on the JSE.

The company has three divisions: (1) Easy Equities which enables investors to buy very small quantities of shares with very low dealing costs. For example, buying R100 worth of a share costs the investors just 64c. 95% of accounts opened are first-time investors and the company has 150 000 active investors. (2) Emperor Asset Management which manages funds on behalf of clients and (3) GT247, a derivatives trading platform.

On 18th May 2023 the company announced the finalisation of its rights issue to raise R105m and already had the support of more than 27% of its shareholders. Shareholders will be offered 10,20567 new shares for every 100 shares that they already hold at a price of 81c per share. The offer is at a 31,87% discount to the volume-weighted average price (VWAP) of the 7 days ending 16th May 2023.

In its results for the year to 31st August 2024 the company reported revenue up 45,1% and headline earnings per share (HEPS) of 1,77c compared with a loss of 2,05c in the previous year. The company said, "Year on year value added from August 2023 to August 2024: - Client assets increased by 24.8% to R58.2 billion (5 year CAGR: 45.4%) - Active retail clients increased by 10.4% to 991,320 (5 year CAGR: 66.4%) - Easy Group Revenue increased by 51.5% to 360.2 million (5 year CAGR: 54.6%)."

In a trading statement for the six months to 28th February 2025 the company estimated that HEPS will be between 2,29c and 2,44c compared with 0,78c in the previous period.

The share is well traded with an average with over R1m worth of shares changing hands daily on average. The share has made a "double top" formation at around 340c in the first half of 2022 and then fell until the beginning of March 2024. Since then it has been rallying.

We advised applying a 65-day exponentially smoothed moving average and waiting for an upward break – which occurred on 4th March 2024 at a price of 66c. It has since risen to 102c.

We believe it still has significant upside potential.

JSE Down From Supply ZoneHi there,

JSE looks bearish on the daily chart, with a potential drop that could reach 11,835 and further down to 10,742.

11,193 is also a support area that can be considered as a target.

Happy Trading,

K.

Not trading advice

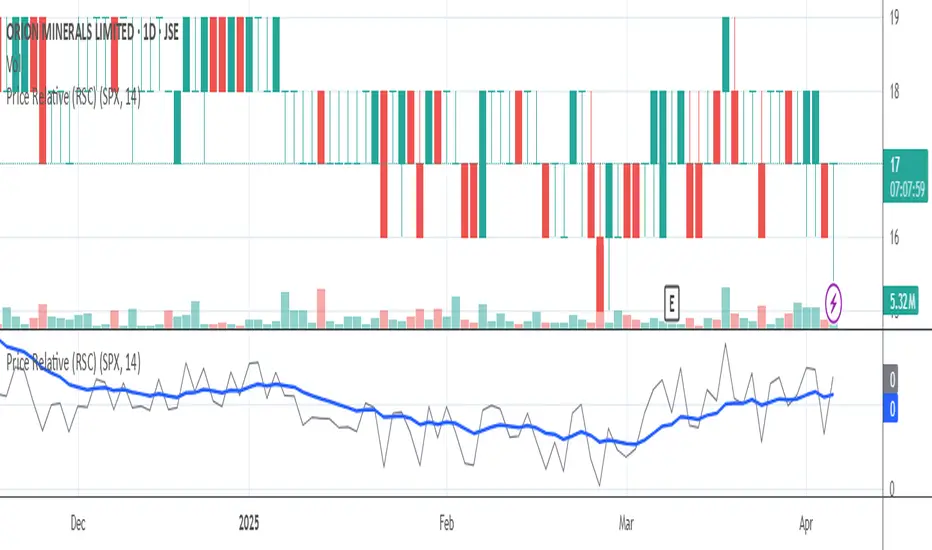

Our opinion on the current state of ORIONMIN(ORN)Orion Minerals (ORN) is an Australian exploration company which is listed on the JSE (September 2017) and on the Australian Stock Exchange in Sydney. It is trying to find funding for its copper and zinc mine in Prieska.

The Prieska mine was previously operated by Anglovaal, but stopped operating in 1990 after 20 years during which it extracted more than 1 million tons of zinc and 430 000 tons of copper concentrate. The main problem with the mine is flooding. Orion hopes to exploit this resource with a mechanised approach and minimum labour.

Vedanta Resources, which runs the Gamsberg mine next to Orion's resource, is looking at building a smelter that could service all the mines in the area and even resources from Namibia. Once construction begins on the Prieska mine, they will need to pump out nearly 9 million cubic meters of water from the existing structure. Production is expected to begin in 2024.

Mining exploration is probably one of the riskiest investments on the JSE. At 30th September 2023 the company had $15,74m in cash.

On 17th April 2024 the company asked for a halt on the trading in its shares because of a "...material announcement on exploration results at Okiep copper mine." On 22nd April 2024 the company announced a "Spectacular High-Grade Copper Intercept at Okiep Copper Project, Flat Mines Area 49m at 4.89% Cu including 10.23m at 12.47% Cu." This caused the share price to jump from 19c to 24c.

Investors should be very careful of this loss-making penny stock and maintain a strict stop-loss level.

On 25th June 2024 the company requested an immediate stop to trading in its shares pending an announcement.

On 28th August 2024 the company announced that it had been granted a key water use licence for the Okiep copper mine.

In its results for the six months to 31st December 2024 the company reported a headline loss per share of 0,01c compared with 0,07c in the previous period (AUD). The company said, "The operating loss for the previous corresponding period reflected an unrealised foreign exchange loss of AUD0.51 million and exploration expenditure of AUD6.73 million."

In our view, this is a volatile penny stock engaged in a particularly risky venture.

On 3rd April 2025 the company announced that Errol Smart would step down as CEO and be replaced by Anthony Lennox with immediate effect.

Our opinion on the current state of SAIL(SGP)Previously Chrometco. Chrometco (CMO) is a company involved in the exploration and mining of chrome. Chrometco is obviously dependent on the international price of chrome and has all the risks associated with a mining company and a commodity share.

In its results for the six months to 31st August 2021 the company reported revenue down 43,6% and a headline loss per share of 2,02c compared with a loss of 2,95c in the previous period. The company said, "...the Group has been under severe financial pressure due to the prevailing chrome market as well as the ongoing impact of Covid-19 on operations. This resulted in Sail Contracting being placed in provisional liquidation on 5 July 2021 and the flagship operation, Black Chrome Mine, being put into care and maintenance soon thereafter. As at 31 August 2021, the Group’s current liabilities exceed its current assets by R922.3 million (28 February 2021: R540.3 million). There is however still a material uncertainty if the Group will be able to meet its obligations."

In addition, this share has very thin volumes traded which makes it relatively risky for the private investor. Essentially, it is a penny stock in a risky commodity which could easily fall into bankruptcy if the chrome price falls.

On 14th June 2022 the company announced that it had placed its Black Chrome Mine in business rescue.

On 1st July 2022 the JSE warned that CMO had missed the deadline to publish its financials within 4 months of its financial period end.

On 18th July 2022 Business Day reported that the JSE had suspended Chrometco shares. The shares were still suspended on 28th March 2024 pending the publication of the financial results.

In a suspension report on 28th June 2024 the company said, "In respect of the late publication of the Company's Provisional Report, the Company has been struggling in its appointment of new auditors due to three subsidiaries within the group, Black Chrome Mine Proprietary Limited ("Black Chrome Mine"), Sail Resources Proprietary Limited and Sail Minerals Proprietary Limited, being in Business Rescue."

In an update on 30th September 2024 the company said, "Trading in the Company's shares remain suspended due to the late publication of the annual financial statements for the years ended 28 February 2022, 28 February 2023 and 29 February 2024 ("Annual Results") and the subsequent interim results for the six months ended 31 August 2022 and 31 August 2023 ("Interim Reports")."

In an update on 3rd April 2025 the company said, "The Business rescue plan for the Company's subsidiary, Black Chrome Mine (Pty) Ltd ("BCM"), was approved and the Business Rescue Practitioner ("BRP") decided to proceed with a Mine Restart and Trade Out Plan ("Plan")."

DRD Long TradeDRD Gold has finally broken out from the Cup and handle pattern

those like me sold at 2,800 High and the systematically bought

back physical silver Krugerrands with the profits. well done.

its time to buy gold again

Standard Bank outperforming the market and showing strong upsideHere is the update with Standard Bank.

The price broke up and out of the Brim level of the Cup and Handle.

The price is also above the 20 and 200 MA - Bullish by nature.

It then rocketed up which I said, the target was on the way to R251.68.

It's an unusual situation as the general JSE has been coming down as of late, and yet banks signal a bit of a foretelling notion that the index is soon set to fly.

Is that the case or will there be a fakeout of note.

We will have to see.

Anheuser Busch InBev preparing for MAJOR upside!Inv Head and Shoulders formed on Anheuser Busch Inbev and now we are waiting for a SOLID break to the upside above the Neckline.

We also see bullish signs with the Moving Averages.

Price> 20 and 200

So we can expect the first target at R1,384.54

But remember, Neckline needs to break first.

POSSIBILITY OF AN UPSIDE PROJECTION (CONTINUATION)FSR is very much bullish but we had sideways movement (accumulation of orders) from March 2022 to July 2024 finally we took liquidity and we had an impulse movement to the upside (Elephant stepped in the pool). The market after breaking the structure it maintained above external high showing intention of a bullish bias, Ey I would be unreasonable to think the market will just push up without a retracement making the price efficient before the bull run..... The back bone of the setup is momentum the correction down to my point of interest is something I could wish for -this is textbook- the concept "sprint & recovery" fits this to perfection. My stops will be around R56.50 stop loss represents where your setup is no longer valid

ABG...... I AM STILL MAINTAINING MY LONGSI was studying the momentum to the upside I am pretty much convinced that the elephant stepped in the pool(liquidity) and the corrective move to the downside it solidifies my long position and I have my heat wave entry instrument I would be looking to take more positions

Our opinion on the current state of ARCINVEST(AIL)African Rainbow Capital (AIL) is a BEE investment company that was formed in 2015 and listed on the JSE in September 2017. Since its formation, AIL has invested in more than forty listed and unlisted investments across a wide range of industries, including telecommunications, mining, construction, energy, property, agriculture, insurance, asset management, and banking.

ARC Investments is 44.4% effectively owned by African Rainbow Capital Proprietary Limited (ARC), which in turn is 100% owned by Ubuntu-Botha Investments Proprietary Limited (UBI). UBI effectively owns 51.2% of ARC Investments. AIL is thus owned through Ubuntu-Botha Investments by the Motsepe family through their trusts.

In the South African context, AIL has a significant advantage in finding suitable companies in which to invest because it can offer them a solid, reliable BEE shareholder. AIL has benefited from an investment by Sanlam and owns a stake in the Sanlam subsidiary, Santam. The company acquired 100% of TymeDigital, which has launched a digital bank in partnership with Pick 'n Pay. It offers digital banking, especially for those who cannot afford normal banking, via their phones, and had the distinction of being the only bank in South Africa not to charge transaction fees. It competes with other new banks in South Africa like Discovery Bank and Bank Zero.

AIL has taken a hit on its investment in EOH (which may now be improving) but has done well in most other areas. Roughly half of the AIL portfolio is in what it describes as "early lifestyle stage businesses" such as Tymebank, Rain, and Kropz. These investments are seen as disruptive in their sectors but will take time to mature. It also owns 7% of Afrimat, having reduced its stake from 18.4%.

If there is a criticism of this investment holding company, it must be its lack of focus. It appears to be invested in a very diverse range of industries without significant synergies or economies of scale. The need for most South African companies to have a stable BEE partner gives it an edge in finding and negotiating good deals, but its lack of focus may eventually become a problem.

The share trades at a fraction of its intrinsic NAV. It was 59% of its NAV after falling about 25% in the last six months to 2023. The discount makes it good value and may result in "unbundling" some of that value into the hands of shareholders in due course. The directors have said that they will consider delisting from the JSE if the discount persists because the listing cannot be used to raise further capital at current share prices.

On 21st November 2023, the company announced a rights issue to raise R742.35m. Shareholders will get 11.06579 new shares for every 100 shares they hold at a 7.32% discount to the volume-weighted average price on 10th November 2023.

In its results for the six months to 31st December 2024, the company reported net asset value (NAV) up 3.2% to 1278c per share. The company said, "Rain - strong performance of rainOne and Rain mobile offerings. TymeBank – 10.7 million customers and increased activity per customer. Tyme Global – GOtyme customer base has more than doubled to 5 million. Alexforbes – strong share price performance on the back of solid results and a positive outlook."

The company announced that it will be delisting from the JSE, and shareholders are offered 975c per share, which is a 22.8% discount to the NAV.

Technically, the share was falling since March 2023. We recommended applying a 200-day moving average and waiting for a clear upside break before investigating further. That break came on 26th April 2024 at 544c per share. The delisting offer means that anyone who acted on that suggestion made a capital gain of 79% in just under one year.

Our opinion on the current state of MASTDRILL(MDI)Master Drilling (MDI) is a South African company that specialises in drilling exploration and other holes for the mining industry. It has diversified into drilling for hydro-electrical projects and construction. The company has moved away from the South African mining industry and now provides services in North and South America, Europe, and elsewhere.

Master Drilling has developed a new horizontal drilling technology, or tunnel boring machine, which could revolutionise the mining industry worldwide. This technology enables the drilling of horizontal tunnels or tunnels inclined up or down by 12 degrees. It is much quicker and cheaper than the traditional blast-and-clear methods currently in use. At the moment, it requires three operators, but the company is working on a completely automated, remote-controlled version.

In its results for the six months to 30th June 2024, the company reported revenue up 17.3% and headline earnings per share (HEPS) down 3.2% (in US dollars). The company's net asset value (NAV) increased 8% to 135c per share. The company said, "...operating profit decreased by 67.6% to USD6.9 million due to impairment losses recognised on reverse circulation and mobile tunnel-boring equipment."

In a trading statement for the year to 31st December 2024, the company estimated that HEPS would increase by between 16.4% and 26.4%. It is now trading at about 62% of its net asset value (NAV) and on a price:earnings (P:E) multiple of 5.25 - which looks like good value.

We regard the company's horizontal drilling technology as a potentially disruptive technology in the mining industry. It extends the life of some mines and makes others viable again. While this is a risky share due to its link to the commodities markets, it has the potential to offer strong growth because of its new technologies. These innovations could revolutionise the mining industry.

In our view, this is an interesting company with the potential to perform well as its new horizontal boring machine gains traction.

Our opinion on the current state of REMGRO(REM)Johann Rupert's Remgro (REM) is an investment holding company that owns 28.2% of Rand Merchant Bank Holdings (RMH) and 3.9% of FirstRand. However, Remgro's investments extend beyond banking. It also owns Mediclinic, an international healthcare company with operations in Switzerland, Southern Africa, and the United Arab Emirates, which has now been delisted from the JSE.

Remgro recently sold its 25.8% stake in the London-listed Unilever Group for R4.9bn in cash, along with the Unilever spreads business in Southern Africa. This acquisition gave it ownership of brands like Flora and Rama. In its food division, Remgro owns 31.8% of Distell and 77.2% of RCL Foods, where the Unilever spreads division may be housed in a new subsidiary called "Silver 2017."

Under insurance, Remgro holds 29.9% of RMI. Additionally, it owns a number of other investments, including a 23.1% stake in Grindrod and a 30% stake in Seacom. The Competition Tribunal has approved the acquisition by Community Investment Ventures Holdings (CIVH), a Remgro subsidiary, of Vumatel, a "last mile" fibre infrastructure company. As part of the approval, Vumatel must supply free uncapped fibre services to schools near its networks for the next 10 years.

On 2nd December 2020, Remgro announced plans to increase its stake in RCL Foods at a cost of R805m. The company also intends to enter the electricity generation business to supply its own businesses, citing concerns over Eskom's reliability.

In its results for the year to 30th June 2024, Remgro reported revenue of R50.4bn, up from R48.1bn, while headline earnings per share (HEPS) declined by 18.8%. The company stated, "A significant driver of the decline in headline earnings relates to the effect of the corporate actions implemented in the recent past, the majority of which are non-recurring items. Remgro's intrinsic net asset value per share increased by 1.0% from R248.47 at 30 June 2023 to R251.01 at 30 June 2024."

In a trading statement for the six months to 31st December 2024, Remgro estimated that HEPS would rise by between 33% and 43%. The company explained, "The increase in headline earnings is driven by improved operational performances from the majority of Remgro's investee companies, lower finance costs, as well as the negative impact of significant corporate actions in the comparative period."

Technically, the share made a low at 8388c on 7th September 2020 and has been in a rising trend. It is currently trading at 15048c on a P:E of 14.78. We recommended applying a 65-day exponential moving average and waiting for a clear upside break before investigating further. That break came on 12th June 2024 at 13000c. We see further upside potential in the share.

Our opinion on the current state of SUPRGRP(SPG)Super Group (SPG) is a large international logistics group offering transportation to the industrial sector. The company has a policy of not paying dividends, preferring to undertake share buy-backs and investing in organic and acquisitive growth. Its policy of diversifying outside South Africa has paid off with as much as 51% of operating profit now coming from non-South African sources. This reduces the company's exposure to the strength of the rand and to the relatively depressed economic conditions which exist in SA at the moment.

The company may have lost as much as R100m during the civil unrest. This is usually a profitable company which generates strong free cash flows. On 19th July 2023, the company announced that it had acquired 78,82% of CBW Group in the UK for GBP30,3m (R700m).

In its results for the six months to 31st December 2024, the company reported revenue down 7,6% and headline earnings per share (HEPS) down 24,2%. The company said the fall was, "...primarily due to weaker performance in the UK Dealerships and Supply Chain Africa Commodity businesses. Operating profit fell by 13.0% to R959.8 million, with the overall operating margin decreasing slightly to 4.1% from 4.3%. This was largely attributed to margin pressure in the Supply Chain Africa Commodity businesses and UK Dealerships. Fleet Africa, however, saw an improvement in operating profit margins."

At the current price of 2760c and on a P:E of 7,8, it looks reasonably valued. It has strong support at around 2500c per share and may bounce off this lower level. On 25th November 2025, the company published a cautionary announcement which caused the share price to jump. An Australian company offered A$3.50 per share for all the shares of Supergroup Fleet. This caused the share price to jump.

Our opinion on the current state of MTN-GROUP(MTN)MTN is a leading emerging market mobile operator, serving 290 million people (including 29 million in South Africa) in 19 countries across Africa and the Middle East. MTN's three largest subscriber bases are in Iran, Nigeria, and South Africa. Generally, companies supplying a mobile service have faced very stiff competition and declining voice revenue. The sharp increase in data usage has, to some extent, mitigated this change, but these companies remain quite risky. MTN is especially risky because of the political risk in Iran and Nigeria.

MTN is working with Sanlam to offer insurance products to its clients in the hopes that "fintech" will become a major part of its business. The goal is to turn MTN into a "...digital operator with a major focus on the fintech, digital, enterprise, and wholesale business areas." MTN has rolled out its mobile money services in both Nigeria and South Africa. It is currently offering these services in 14 out of the 21 countries where it operates, and it has 41.8 million mobile money customers. It is trying to increase that number to 60 million. MTN has now listed on the Nigerian stock exchange.

On 13th January 2023, MTN received an assessment from the Ghanaian tax authorities that it owed $773 million (about R13.3 billion). This is seen as a "shakedown" of a wealthy international company by a cash-strapped national government—similar to what happened in Nigeria. The company announced that Mastercard would take a R100 billion stake in its fintech business and partner with it to expand that business.

In its results for the six months to 31st December 2024, the company reported data revenue up 21.9% and fintech revenue up by 28.5% in constant currencies. Headline earnings per share (HEPS) fell by 68.9% and total subscribers increased by 2.2% to 290.9 million. The company said, "Active data subscribers increased by 7.7% to 157.8 million - Mobile Money (MoMo) monthly active users (MAU) increased by 0.9% to 63.1 million - Data traffic increased by 32.6% to 19 459 Petabytes (PB) - Fintech transaction volumes increased by 15.3% to 20.3 billion."

Clearly, the company is being impacted by the volatility in the Nigerian economy, which has been a large part of its business. The share was falling from its cycle high in March 2022. We recommend applying a downward trendline from that peak and waiting for a clear upside break before investigating further. That break came on 7th December 2024 at a price of 9289c, and the share has since moved up to 11519c. It was added to the Winning Shares List (WSL) on 14-1-25 at 9729c.

Our opinion on the current state of RHODES(RFG)Rhodes (RFG) is a Western Cape manufacturer of convenience foods—started by Cecil John Rhodes in 1896. It has several well-known South African brands like Bisto, Bull Brand, and Hinds. The company operates 15 manufacturing plants in South Africa and a fruit processing plant in Swaziland.

In its results for the year to 29th September 2024, the company reported revenue up 1,5% and headline earnings per share (HEPS) up 18,6%. The company's debt-to-equity ratio improved from 21,3% to 11,9%. The company said, "The regional segment delivered resilient revenue growth in an environment of sustained pressure on consumer spending. However, the rate of volume decline and price inflation have slowed considerably relative to the prior year as consumer confidence started to show signs of improvement."

In a trading update for the 5 months to 28th February 2025, the company reported revenue up 2,1%. The company said, "Regional revenue increased by 5.6%, driven by volume growth of 8.7% (prior comparative period: volume decline of 5.7%) and price deflation of 0.6% (prior comparative period: price inflation of 10.8%)."

Technically, the share fell from a high of 2900c in October 2016 in a bear trend. We suggested waiting for it to break up through its long-term downward trendline—which happened on 13th November 2023 at a share price of 1220c. It has since moved up to 1895c and is on a P:E of 8,53— which looks reasonably priced, even cheap. We believe that the share will continue to recover over time as the economy and rand improve.