Our opinion on the current state of ANGGOLD(ANG)AngloGold Ashanti (ANG) is an international gold producer that used to have operations in South Africa (the last of which, Mponeng, has now been sold) and still has assets in the DRC, Tanzania, Ghana, Mali, and the US. It had some significant problems in bringing the Obuasi mine into production and with the Tanzanian government over royalties. The company has 14 operational mines.

AngloGold has retained its listing on the JSE despite having no South African assets. On 14th July 2021, the company announced that it had acquired Corvus Gold for R5,4bn in cash to extend its exploration in Nevada, USA. This is a relatively marginal, short-life (11 years) gold mine with rising costs, falling grades, and a volatile gold price.

In its results for the year to 31st December 2024, the company reported a, "...nine-fold increase in 2024 free cash flow to $942m versus prior year; Adjusted EBITDA* +93% year-on-year and H2 dividend growth of 263% to 69 US cents per share; total cash costs* +4% for FY 2024, below group inflation." Headline earnings per share (HEPS) was 221c (US) compared with a loss of 11c in the previous period.

Technically, the share has been rising since March 2024 in what looks like a volatile upward trend. On 10th September 2024, the company announced that it had made an offer for 83,6% of Centamin in Egypt for 0.06983 AngloGold shares and $0,125 in cash. The announcement caused ANG's share price to fall.

This share remains a speculation on the gold price.

Our opinion on the current state of DISCOVERY(DSY)Discovery (DSY), developed and built by Adrian Gore over the past 25 years, offers the A/B income group of people a matrix of financial services that are inter-linked and cross-selling. Thus, a customer can begin with his/her medical aid and then add to that a variety of insurance products and now, most recently, personal banking products.

Discovery's "Vitality" concept, which rewards clients for looking after their health in various ways, is extended to their driving record and a rewards system that ensures that there are attractive benefits for taking the full range of Discovery debit-order products. The Vitality platform tracks over 1000 customer activities and 50 biometrics a minute by using the Apple Watch in South Africa, the UK, China, Europe, and the US to ensure a process of healthy aging and retirement planning.

Discovery's Chinese company, Ping An Health, in which Discovery has a 25% stake, saw membership grow by 60% over the year, and written premiums increased by 87% to $753m. Ping An is rapidly developing into Discovery's "Tencent."

Discovery's move into banking offers existing clients a range of banking and credit card facilities. The banking license was approved in November 2017 and should significantly increase the profits being generated by the group in time. This is a disruptive development that will seriously shift the banking of A/B income group consumers away from existing banks. Discovery Bank's aim was to bring in 1000 new accounts per day from the end of August 2019.

The company has seen a drop in car accident claims and medical insurance claims since the lockdown. This is a highly rated share despite the decline in its share price over the past two years. Discovery Bank has now reached 700 000 active clients and those clients are mostly of very high quality—but the progress has been relatively slow, partly because of the pandemic.

Discovery shares remain expensive, but we regard this as one of the best shares for a private investor to hold for long-term growth. CEO, Adrian Gore, says, "I am a great believer that opportunities are not in good times,"—indicating his belief that growth comes from investing during difficult times such as South Africa is currently experiencing. Gore has also stated that the NHI, as it is proposed, is unaffordable for South Africa and that there are insufficient medical resources to implement it.

Discovery became the first large, listed company to require all its staff to be vaccinated. On 20th June 2022, the bank reported that it had more than 1 million accounts and was taking on about 750 new accounts per day.

In its results for the year to 30th June 2024, the company reported headline earnings per share (HEPS) up 14% and net asset value (NAV) up 16%. The company said, "Discovery Group achieved strong growth in the year ended 30 June 2024, with normalised operating profit up 17% to R11 604 million, headline earnings up 7% to R7 202 million, normalised headline earnings up 15% to R7 329 million, and core new business annualised premium income (API) up 18% to R26 667 million."

In a trading statement for the six months to 31st December 2024, the company estimated that HEPS would increase by between 30% and 35%.

Technically, the share has been in an upward trend since June 2024. We added it to the Winning Shares List (WSL) on 1st August 2024 at 14280c. It has subsequently moved up to 20936c. Due to the quality of its management and business model, we see this as a "must-have" share for any private investor's portfolio.

Our opinion on the current state of GLENCORE(GLN)Glencore (GLN) describes itself as, "...one of the world’s largest global diversified natural resource companies and a major producer and marketer of more than 90 commodities." The group's operations comprise around 150 mining and metallurgical sites, oil production assets, and agricultural facilities. With a strong footprint in both established and emerging regions for natural resources, Glencore's industrial and marketing activities are supported by a global network of more than 90 offices located in over 50 countries.

This is a massive, diversified mining house that markets its products worldwide and is involved in almost every mineable commodity that exists. This means that it is far less volatile and risky than other less diverse mining houses. Since the commodity cycle turned at the start of 2016, one of the greatest beneficiaries has been Glencore, particularly because it owned the world's richest source of cobalt in the Democratic Republic of Congo (DRC). Cobalt is the metal used in the batteries required for the world's shift to electric motor vehicles.

The problem is that the government in the DRC is in the process of declaring cobalt a "strategic mineral," which means much higher tax. The company is in the process of aggressively buying back GETTEX:2BN worth of its own shares. Glencore announced on 28th June 2021 that it had bought Anglo's 33% stake in Correjon Colliery in Columbia for $294m. Glencore clearly benefited from the war in Ukraine and the increase in coal prices, particularly.

In a production update on the year to 31st December 2024, the company reported copper production down 6%, cobalt down 8%, zinc down 1%, nickel down 16%, and energy coal down 6%, while lead was up 2% and steel-making coal was up 165%. The company said, "2024 production volumes were delivered within our guidance ranges (unchanged from the beginning of the year), reflecting stronger second half (H2) performances across our key commodities. Copper production was 26kt higher in H2 (+6% vs H1), supported by Antapaccay's recovery from H1 geotechnical issues."

Business Day (20-2-25) reported that Glencore had made a R30bn loss in the year to 31st December 2024, mainly because of lower prices for thermal coal. The price of nickel was down 22%, and cobalt fell 27%. The company has impaired its zinc and copper operations by almost R1,5bn. Earnings per share (EPS) fell to a loss of 13c (US) from a profit of 34c.

The share made a convincing "descending double top," with the second top being slightly lower than the first in April 2024. Technically, this is a bad sign. The fact that the share could not rise above its January 2023 top at R120 was a major disappointment to the bulls. Commodities are in a downward trend, which has a direct impact on Glencore.

Our opinion on the current state of METROFILE(MFL)Metrofile (MFL) is a company that specializes in records storage and management, image processing, and backup. The company has been listed since 1995 and has a 57.4% Black ownership. The Mineworkers Investment Company owns 38.64% of the business, and Sanlam owns 5%.

The company's record management division has 52 facilities at 27 locations with over 100,000 square meters of offices and warehousing. Housatonic Partners, a US company, made an offer to buy 100% of Metrofile for 330c per share but delayed the deal because of COVID-19. They stated that they would want to see the end-June 2020 results and "three months of normal trade" before reconsidering. Despite this, they have assured the company of their wish to continue with the possible acquisition of Metrofile.

In its results for the year to 30th June 2024, the company reported revenue up 1% and headline earnings per share (HEPS) down 49%. The company said, "General market conditions were weak. Demand for cloud services remained strong and now contributes 32% (2023: 26%) of our digital services revenue."

In a trading statement for the six months to 31st December 2024, the company estimated that HEPS would fall by between 23% and 46%. We see this as a good-quality small business that seems to be battling in a very tough economic climate.

Technically, the share now looks to be in a new downward trend. On 5th September 2024, the company announced that its CEO, Pfungwa Serima, would resign with effect from 30th September 2024. He will be replaced by Thabo Seopa.

Our opinion on the current state of MPACT(MPT)Mpact (MPT) is a large producer of paper and plastics packaging in Southern Africa. It recycles paper and cardboard and makes corrugated cardboard containers for a variety of industries, as well as polystyrene trays for the food industry. It has 20 manufacturing operations, with South African sales accounting for 86% of its business. It employs over 5,000 people.

The business is impacted by the general level of consumer spending (which has been depressed because of COVID-19 and was improving at least until the advent of the Ukraine crisis) as well as weather considerations, which affect the demand for corrugated containers for fruit and other agricultural products, especially in the Cape. Like many businesses in the current environment, Mpact has been working to preserve cash, but it has benefited from a switch to local suppliers during the pandemic.

In its results for the six months to 30th June 2024, the company reported revenue slightly down at R6,17bn and headline earnings per share (HEPS) of 144,6c compared with 211,6c in the previous period. The company's net asset value (NAV) increased 9% to 3411c per share. The company said, "The uncertain socio-political environment leading up to the national elections, high levels of loadshedding that continued until the end of March, high inflation and interest rates all contributed to weak consumer and business sentiment."

In a trading statement for the year to 31st December 2024, the company estimated that HEPS for continuing operations would be between 23,3% and 30% lower than in the previous period. The company said, "The Group experienced a challenging trading environment for most of the 2024 financial year, despite positive sentiment emerging from the May 2024 election outcome and reduced loadshedding since April 2024."

The share fell from a high of R51 in April 2016 to levels around R8 in March 2020 but has since recovered to 2812c. At the current level, it is on an earnings multiple of 6,31 - which looks cheap.

Technically, the share looks like it may be entering a new upward trend, but it has been moving sideways since August 2022. On 1st August 2024, the company announced that it had sold its Versapak business for R267,7m. On 3rd February 2024, the company announced that its shares would be traded on the A2X with effect from 11th February 2024.

Our opinion on the current state of SIBANYE-S(SSW)Sibanye (SSW) is a mining house that has been on a rapid acquisition trail, accumulating platinum and gold mines in South Africa and America and now broadening its scope to include base metals and minerals, especially so-called "green" metals.

The company is run by Neal Froneman, who is well-known in the mining industry for his toughness, expertise, and experience. Froneman has said that he intends to retire in about 2024/5 but plans to double the size of the company before he does. Sibanye is also considering moving into the base minerals used in motor vehicle batteries, like vanadium, copper, nickel, and lithium.

On 1st June 2021, the company announced a share buy-back program to repurchase up to 5% of its issued shares. On 3rd July 2024, Business Day reported that Sibanye had retrenched 11,000 workers over 18 months.

In its results for the six months to 30th June 2024, the company reported headline earnings of R137m compared with R5,891m in the previous period. Lower commodity prices caused revenue to decline by 9%. The company said, "The Group maintained a sound financial position with undemanding balance sheet leverage of 1.43x net debt: adjusted EBITDA at 30 June 2024, well below our covenant levels."

In an update for the 3 months to 30th September 2024, the company reported EBITDA up 9% and EBITDA from South African gold operations up 292%. The gold price in rands was up 24%.

In a trading statement for the year to 31st December 2024, the company estimated that HEPS would be between 63c and 67c compared with 63c in the previous year. The company took an R8,8bn impairment loss on its PGM operations in the US, which is not reflected in HEPS.

Technically, the share has been in a downward trend since March 2022, mainly because of falling commodity prices. On 13th February 2024, the company announced that CEO Neal Froneman would be retiring on 30th September 2025 and will be replaced by Richard Stewart.

Our opinion on the current state of VODACOM(VOD)Vodacom (VOD) is South Africa's largest airtime and data provider for cell phones. It is a subsidiary of the international company Vodaphone. Its competitors are MTN, Cell-C, and Telkom.

The cell phone industry has been hammered by a steady decline in voice revenue, which has to some extent been compensated by a sharp rise in data usage. The disadvantage which Vodacom has as an investment is that a foreign parent owns it. This was graphically demonstrated when its share price fell 7% in two days because it was feared that its parent company would be pressured to sell off its non-European subsidiaries.

Vodacom has businesses in Mozambique, Tanzania, the DRC, and Lesotho. Now the group is looking to develop a business in Africa's fastest-growing economy, Ethiopia, with a population of 105m. On 2nd December 2019, the Competition Commission ruled that Vodacom and MTN had to cut their interconnect fees by between 30% and 50%. Much of Vodacom's revenue comes from interconnect fees, and it saw its share price drop by 5%.

The company is launching a "super-app" in conjunction with Jack Ma's Alipay to boost its non-voice revenue. It has also spent R4bn to mitigate the impact of loadshedding. We believe that this share will perform well, but may take some time to reach former heights.

In its results for the six months to 30th September 2024, the company reported revenue up 1% and headline earnings per share (HEPS) down 19,4%. Financial services revenue increased by 7,8% and contributed 11,4% to group service revenue. The company had 206m customers and rendered financial services to 83m. The company said, "While our bottom line was impacted by various one-offs, I am confident that we are poised for a stronger second-half performance."

In a trading update for the 3 months to 31st December 2024, the company reported revenue up only 1,6% due to the stronger rand, with service revenue up 11,6%. The company said, "...the quarter was positively impacted by accelerated growth in South Africa's prepaid market in addition to another stellar performance in Egypt and Tanzania, while network operators in Mozambique, including Vodacom, have been hampered by post-election tensions since October 2024."

In a presentation to investors on 19th February 2024, the company said that it expected to grow earnings by 10% per annum in the years between 2025 and 2030. The expectation is that its Egyptian subsidiary will grow profits by at least 20% per annum.

Technically, the share fell from its high of 16214c on 1st April 2022, and we suggested waiting for a clear break up through its downward trendline, which happened on 25th July 2024 at 9836c. Since then, it has risen to 11900c. It still looks relatively cheap at current levels, with a dividend yield (DY) of around 3,83%—but it is in an environment where technology and regulation shift continuously, making it risky.

Our opinion on the current state of TRENCOR(TRE)Trencor's (TRE) primary asset is 47,78% of Textainer, a US-listed renter of shipping containers (Twenty-foot units or TEUs).

It should be noted that Trencor spent R100m buying back its own shares between 4-10-18 and 6-12-18. Investors have been unhappy with the fact that Textainer has been underperforming its competitors. For example, Triton had a return on equity of 16% compared to Textainer's 1,7%.

Trencor has unbundled its holding of Textainer into the hands of its shareholders, which resulted in a tax of R17m.

In its results for the six months to 30th June 2024, the company reported headline earnings per share of 9,8c compared to 64,8c in the previous period. The company said, "Whether or not the company will be in a position to commence the winding up process following 31 December 2024, as currently intended, will depend on the satisfactory conclusion of all outstanding regulatory and other matters required in order to wind the company up."

In a trading statement for the year to 31st December 2024, the company estimated that HEPS would fall by between 55,2% and 65%. The company said, "The after-tax unrealised loss from the translation of the US dollar deposits into SA rand for the current period was R15,1 million (2023: profit of R83,9 million)."

Trencor paid out a special dividend of 730c to shareholders, which went ex-div on 19th February 2025, resulting in a sharp drop in the share's price.

Our opinion on the current state of AFRIMAT(AFT)Afrimat (AFT) is an open-pit mining company that supplies composites, construction materials, and other commodities to a range of industries in Southern Africa.

Until the end of 2015, Afrimat was one of the best-performing shares on the JSE. The share broke up out of a three-year sideways pattern, which included the COVID-19 crisis. It rose to a peak of R76 on 6th April 2022 but has been declining since then as the commodities cycle came to an end.

The acquisition of the Demaneng iron mine in the Northern Cape has insulated Afrimat against the difficulties in the construction industry. The company is also looking to diversify into other base minerals like manganese, chrome, and coal. The CEO, Andries van Heerden, said that Afrimat was known for its success in acquisitions and was still evaluating potential acquisitions.

On 26th May 2020, the company announced that it had submitted a non-binding expression of interest to Unicorn Capital Partners (in which it already owns 27%), which runs an anthracite mine. The offer is for 1 Afrimat share for 280 Unicorn shares. The company benefited from rising iron ore prices due to supply constraints in Brazil and rising demand from China.

On 17th August 2020, the company announced that it had bought a mining exploration company (Coza Mining) involved in looking for iron and manganese in the Northern Cape for R300m. On 21st May 2021, the company announced the purchase of a manganese mine, Gravenhage, in the Kalahari Manganese Field, 50km from Hotazel, for $45m plus R15m.

On 10th December 2021, the company announced the acquisition of Glenover Phosphate for R550m. On 20th March 2022, the company announced that its listing had been moved from Basic Materials Construction and Materials to the General Mining sector, which better reflected its business.

On 20th June 2023, the company announced that it had acquired 100% of construction materials company, Lafarge, for $6m, less any amounts categorised as leakage under the Share Purchase Agreement.

In its results for the six months to 31st August 2024, the company reported revenue up 44,3% and headline earnings per share of 53c. The company's net asset value (NAV) rose 10,5% to 3038c per share. The company said, "Afrimat felt the brunt of a declining iron ore price, a strengthening Rand, continued limitations on the export rail line, large industrial customers reducing offtake because of economic and unforeseeable circumstances, and losses in the cement business. This culminated in headline earnings per share reducing from 263,4 cents to 53,0 cents."

In a pre-close update, the company said, "Poor rail performance continues to impact export iron ore volumes. Volumes align with the previous financial year, which is good news to an extent because volumes have not deteriorated."

Like all commodity companies, Afrimat's shares have declined with the drop in commodity prices, but this company is well-diversified and has very low debt levels, making it good value. On 10th April 2024, the company announced that it had received approval from the Competition Commission for its acquisition of 100% of Lafarge.

On a P:E of 17,63, it seems fully priced to us. Technically, the share is in a volatile upward trend, which we believe will continue.

Our opinion on the current state of AMPLATS(AMS)Anglo American Platinum (AMS), or Amplats, is the second-largest platinum-producing company in the world (after Sibanye), producing a large portion of the world's platinum. It is owned 77,62% by Anglo American.

Amplats was one of the first platinum mining companies in South Africa to move away from expensive deep-level mining towards shallower, more mechanised mining. The company has reduced the number of mines it is operating from 18 to 7 over the past five years, decreased overheads by 50%, and its number of employees by 50%. This shift is now paying handsome dividends.

The Mogalakwena open-cast operation is a palladium-rich operation with costs in the lowest quartile in the platinum group metals (PGM) industry worldwide. A new project at Mogalakwena will see platinum production up by 250,000 ounces and palladium production up by 270,000 ounces. Amplats also recently bought out Glencore's 40,2% stake in their joint venture Mototolo mine and the adjacent Der Brochen property for R1,5bn. Mototolo is a highly mechanised shallow mine that can be extended into Der Brochen without putting in new surface infrastructure.

The platinum price is plagued by an effective recycling industry that produces about 2 million ounces a year by recovering from old auto catalysts. We believe AMS is the best of the PGM shares on the JSE - but it remains a commodity share and thus volatile and unpredictable.

As part of its plans to boost production at Mogalakwena, the company has plans to relocate 1,000 families of its employees, which could result in unrest. On 10th December 2021, the company announced a R3,9bn extension to the life of its Mototolo/De Brochen mines to beyond 30 years. On 15th February 2023, the company announced that CEO, Natascha Viljoen, would resign but would serve out her 12-month notice period.

In its results for the year to 31st December 2024, the company reported revenue down 13% and headline earnings per share (HEPS) down 40%. The rand basket price per PGM ounce fell by 13%, and costs per 3E ounce were down 13% in US dollars. The company said, "EBITDA of R19.8 billion, is 19% lower than the prior period, largely due to a ~13% decline in the realised ZAR PGM basket price and R3.5 billion of non-recurring costs owing to the recent operational and corporate restructuring, the demerger and losses from associates."

This share is a speculation on the international prices of the platinum group metals that it produces and hence very volatile. Technically, the share has been moving sideways since September 2023, mainly due to the challenges faced by the industry, including load-shedding and the falling prices that they are getting for their production.

On 23rd July 2024, *Business Day* reported that Amplats was considering listing on the London Stock Exchange (LSE).

Our opinion on the current state of AVENG(AEG)The once-massive construction company, Aveng (AEG), which traded at R69 a share in 2008, was reduced to a penny stock. This sad demise was brought about by a number of factors.

Among these, the reduction in construction spending following the sub-prime crisis has been critical. The government ceased infrastructure development after the 2010 World Cup, which had a further detrimental impact. This was then followed up by the Competition Commission's R1,4bn fines in the construction industry.

The difficult operating environment was made worse by losses on various construction contracts, which have required extensive write-downs and impairments. Its objective has been to focus on McConnell Dowell in Australia and the mining contractor Moolmans, both of which are now profitable.

On 26th January 2021, the company announced the terms of a fully underwritten rights issue to raise R300m by selling about 20 billion shares at 1,5c each. Shareholders were offered 103.122 rights for every 100 shares held. This obviously substantially diluted the existing shareholders.

On 12th October 2021, the company announced a 500-for-1 consolidation effective 8th December 2021, which resulted in the share price rising to around R28. The company announced the sale of Trident Steel on 3rd May 2023 for R1,2bn - which effectively leaves the company debt-free.

The company announced its intention to report in Australian dollars in the future, not rands, because it said 91% of its income was now received in Australian dollars.

In its results for the six months to 31st December 2024, the company reported revenue slightly down at A$1,4bn, with a headline loss per share of A$26,7c compared with a profit of A$8,8c in the previous period.

The company said, "Aveng's revenue contracted 8.1%, in line with previous guidance, to A$1.4 billion (R16.6 billion) in the interim period ended 31 December 2024 (December 2023: A$1.5 billion (R18.6 billion)), following an expected softening of infrastructure markets in Australia and New Zealand."

Prior to this, the share had been moving up since mid-May 2024 and looked to be in a new upward trend. The latest results have seen the share lose most of its gains.

Our opinion on the current state of QUANTUM(QFH)Quantum (QFH) is in the chicken business. It has four divisions - Animal Feeds, Eggs and Layers, Broilers, and an African division where it sells related products.

Quantum was obviously badly impacted by the drought in Southern Africa, but since that abated and the price of animal feeds came down, it has benefited from the much higher prices of eggs and the lower cost of feeds.

In general, the chicken business is a tough business. It is labour-intensive, which creates exposure to union action, it involves large quantities of working capital tied up in stock and, to a lesser extent, debtors, it is subject to unexpected disease threats like avian flu or Newcastle disease, and it has experienced the dumping of cheap chicken onto the South African market from Europe, Brazil, and America.

With top-class management, a sustainable profit can be achieved, but the industry is regarded as relatively high-risk by investors, which accounts for its low price-earnings (P:E) multiple and its high dividend yield (DY).

The unprotected strike at Kaalfontein Farm has restricted output and cost an estimated R10m. The company suffered an outbreak of HPAI at its Lemoenkloof Farm as well as loadshedding and labour unrest.

In its results for the year to 30th September 2024, the company reported revenue down 8.9% and headline earnings per share (HEPS) of 80.4c compared with a loss of 17.4c in the previous period.

The company said, "FY2024 will be remembered for the severe impact of highly pathogenic avian influenza (“HPAI”) on our layer farming and egg businesses, the Malmesbury feed mill explosion, leadership changes and dramatic fluctuation in our share price on the back of shareholder activity."

In an update for the 4 months to 31st January 2025, the company reported a significant improvement in trading conditions.

The company said, "...the Company benefited from improved throughput as a result of a recovery in its layer flock, no loadshedding in South Africa, relatively high egg selling prices and no HPAI outbreaks. Feed costs for the Current Period were relatively stable compared to the Previous Period."

Nobody knows what difficulties the business may experience over the next 12-month period. So, if you plan to invest in this share, be prepared for considerable volatility. This company sometimes has difficulty in passing on higher raw materials costs to consumers, especially in the current economic environment.

Our opinion on the current state of BATS(BTI)British American Tobacco (BTI) describes itself as a "leading consumer goods company" - which is a euphemistic way of saying that they produce and sell an enormous number of cigarettes and related products worldwide. It is also the second-largest company on the JSE after Naspers.

In recent decades, cigarette companies have become increasingly oppressed. Their ability to advertise their products and even package them has been severely curtailed in many countries. They are seen to be exploiting an addiction that is clearly anti-social and very bad for the individual's health, regularly involving them in lawsuits for damages.

BAT owns well-known brands like Camel, Peter Stuyvesant, Rothmans, Benson & Hedges, Dunhill, Pall Mall, Kent, and Lucky Strike. In an effort to get away from the negative perceptions of cigarettes, the company has diversified into "new category" products such as vaping and electronic cigarettes, which it claims offer a long-term prospect for growth.

Recently, especially in the United States, these products have also come under the spotlight for health reasons, leading to a drop-off in sales.

As an investment, the company offers some attractions. Roughly 20% of the world's population still smokes, making a truly massive market. Setting aside our distaste for the business which BAT conducts, the share looks like very good value at current levels. This is one of the shares that has performed well and perhaps even benefited from COVID-19.

The CEO says that he aims to double non-combustible sales by the 2023/24 year. It is interesting that BAT considers South Africa's illegal cigarette market to be the largest in the world.

On 6th December 2023, *Business Day* reported that BAT had impaired its US operations by GBP25bn (R595bn), leading to a drop of 10% in the BTI share price.

In its results for the year to 31st December 2024, the company reported revenue down 5.2% with organic revenue up 1.3%, driven by New Categories, which was up 8.9%.

The company said, "Reported profit from operations of £2,736m (2023: loss of £15,751m) with 2024 including a provision of £6.2 billion in respect of the proposed settlement in Canada, while 2023 was negatively impacted by one-off impairment charges largely in the U.S. Adjusted organic profit from operations up 1.4% (at constant rates), driven by AME and APMEA."

The share has basically been moving sideways for several years. We do not regard it as a good long-term investment.

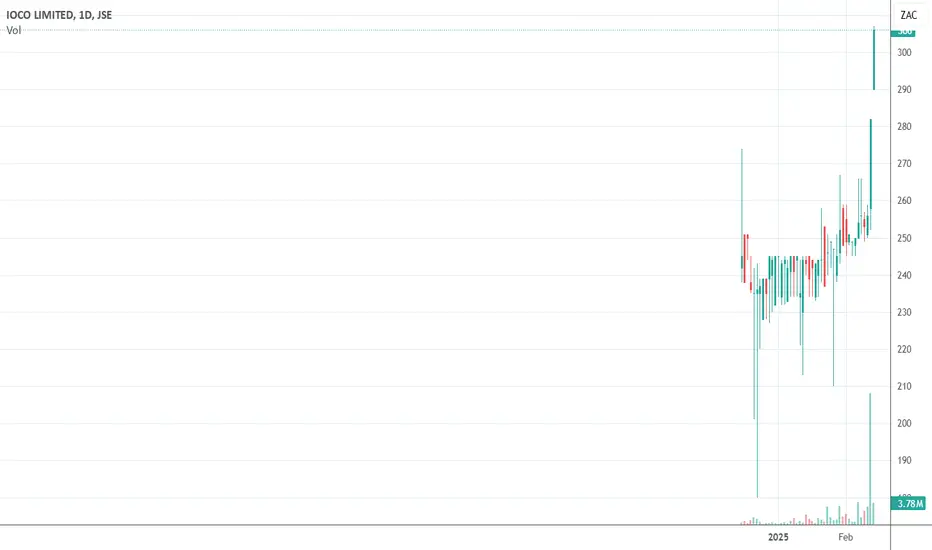

Our opinion on the current state of IOCO(IOC)Previously called Enterprise Outsourcing Holdings (EOH), Ioco was Africa's largest information technology company with involvement in almost every aspect of computer applications. At one point, the company had 11,000 staff members, but that has now been reduced to 6,151.

It was, until August 2015, the darling of the JSE because it had a long track record of steadily improving profits. It made a peak of R178 per share at a P:E of 35. An unsuccessful attempt to exceed that high (i.e., a double top) came a year later in September 2016, and since then, the share has fallen steadily to reach a low of 146c in February 2023.

This fall was initially accompanied by allegations that the company was involved in and owed its success to state capture in collaboration with the Guptas. The CEO and founder, Asher Bohbot, resigned in May 2017 and handed over to Zunaid Mayet, who later handed over to Stephen van Coller. Usually, when a company is run by a strong charismatic leader and that leader (like Bohbot) resigns, it is time to sell the share.

The company's 200 subsidiaries have been consolidated into three divisions with centralized debt collection and procurement.

On 6th July 2021, *Business Day* reported that EOH could possibly be "blacklisted" by the government as a result of its past tender frauds. This would obviously be very negative for the company.

On 11th November 2022, the company announced a R500m rights issue and a R100m private placement, mainly to reduce debt. On 13th February 2023, it announced that the offer had been 135.8% oversubscribed.

In its results for the year to 31st July 2024, the company reported revenue down 3.1% and a headline loss per share of 0.21c compared with a loss of 21c in the previous year.

The company said, "A special board subcommittee was formed in June 2024 to turn EOH around. Key initiatives include business restructure and rationalization plans. Corporate and administration cost restructure successfully completed. Cost savings of between R160 million and R200 million anticipated into FY25."

In a trading statement for the six months to 31st January 2025, the company estimated that HEPS would increase to between 19c and 21c compared with a loss of 11c in the previous period.

On 31st May 2024, the company announced the resignation of various directors and the appointment of Marius de la Rey as interim CEO.

Technically, the share made a "double bottom" in April and May of 2024, after which it began a new upward trend. We believe that it will continue to rise.

On 14th February 2025, the company announced that Marius de la Rey had resigned with immediate effect. Directors Rhys Summerton and Dennis Venter have been appointed as joint CEOs and executive directors.

Our opinion on the current state of ITLTILE(ITE)Italtile (ITE) is a franchisor of tiles, sanitary ware, flooring, and home finishing products - which it manufactures and wholesales itself. The company is controlled by the Ravazotti family.

It has 206 stores and six online web stores. It also has a property portfolio of retail and industrial properties worth about R4.3bn. The company has acquired 95.47% of Ceramic Industries and 71.54% of Ezee Tile, which it styles as its manufacturing business (as opposed to its retail business).

The company gained an increased "share of wallet" and improved the management of stockholding and working capital. The company appears to be benefiting from increased sales as people work from home and seek to improve their home environments. It plans to add between 10 and 15 new stores this year. It has also bought back about R240m worth of its own shares at lower levels.

The company closed 18 stores in Natal and 16 other stores for ten days during the civil unrest. Two stores at Orange Farm and Spruitview were destroyed. There have also been store closures due to COVID-19 during July 2021.

In its results for the year to 30th June 2024, the company reported turnover unchanged and headline earnings per share (HEPS) down 7%. The company's net asset value (NAV) was up 10% at 707.5c per share.

The company said, "While our retail operation's full-year results were slightly lower than the prior comparable year, the division recovered market share and performed better in the second half of the period than the first half."

In a sales update for the five months to 30th November 2024, the company reported retail turnover up by 2.2%.

The company said, "Combined manufacturing sales reported by Ceramic Industries Proprietary Limited ("Ceramic Industries") and Ezee Tile Adhesive Manufacturers Proprietary Limited to both Group and third-party customers declined by 1.6% compared to the Prior Period's decline of 5.9%."

In a trading statement for the six months to 31st December 2024, the company estimated that HEPS would increase by between 2% and 6.7%.

Technically, the share moved sideways for two years until COVID-19 took it down to levels around R10. The share broke up through its long-term downward trendline in June 2024 and rose strongly until the end of that year. Since then, it has been in a downtrend.

It will probably benefit from new building activity expected to follow the formation of the new GNU in South Africa.

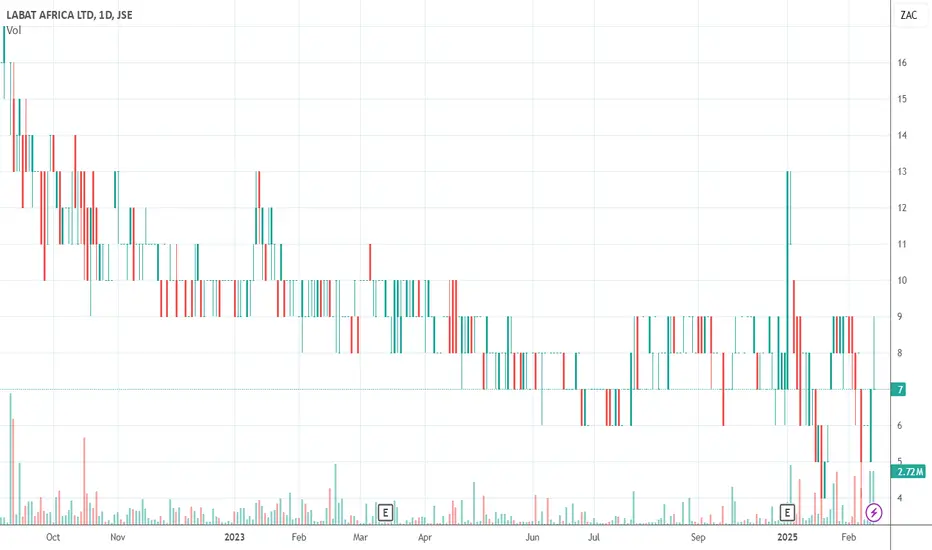

Our opinion on the current state of LABAT(LAB)Labat (LAB) is a 57% black-owned investment holding company that listed on the JSE in 1999. The company buys and improves subsidiaries and then sells them for a profit.

At the moment, Labat has two operations - South African Micro-Electronic Systems (SAMES) and Labat Logistics.

On 14th April 2020, the company announced that it had acquired 70% of Biodata, an East London-based company that is focused on cannabis healing. The acquisition is to be paid for in shares. The market for cannabis in South Africa in 2020 was expected to be worth around R27bn.

On 5th May 2020, the company issued a profit forecast for the years 2021 and 2022 - in which it said it was raising R112m by the issue of shares and that it would generate a profit of R60m in 2021 and R162.3m in 2022, resulting in headline earnings per share (HEPS) of 10.9c and 29.9c respectively.

On 8th May 2020, the company announced that it had decided to put Force Fuel into business rescue because of a drop in volumes as a result of COVID-19.

In its results for the six months to 30th November 2023, the company reported revenue of R36.6m compared with R24m in the previous period. Headline earnings per share (HEPS) were 0.78c compared with a loss of 1c in the previous period.

The company said, "Group revenue for the year increased by 152% to R36.7 million (2022: R24.1 million) compared to the prior year. This increase was driven mainly by the 13 new retail wellness stores that were opened during the year."

In a trading statement for the six months to 30th November 2024, the company estimated that HEPS would increase by 98.72%.

The company's shares were suspended on the JSE in October 2023 and only commenced trading again on 2nd January 2025 with the publication of the interim results to 30th November 2024.

Even when trading, this is a volatile, often loss-making penny stock, so investors should probably leave it alone.

Our opinion on the current state of IMPLATS(IMP)Impala Platinum Holdings (IMP), or Implats, is the world's third-largest platinum group metals (PGM) producer.

It has been suffering over the past seven years from aggressive union action and legislative uncertainty. The CEO says that they are focused "...on developing a portfolio of long-life, low-cost, shallow, modern, mechanised mining assets." This is similar to what Anglo American Platinum has been doing for the past ten years.

The market for platinum itself has been damaged by a reduction in auto catalyst demand recently, especially for diesel trucks. Palladium and rhodium still have strong markets, but platinum has been oversupplied on world markets.

The company plans to grow its production from Zimbabwe by 14% due to the Mupani shaft coming on stream in 2022. Its newly acquired Canadian operation should also increase production.

On 20th July 2023, the company announced that it had acquired 56.52% of RB Plats as a result of its mandatory offer. Northam also announced its decision to sell its 34.5% holding to Implats.

On 28th June 2022, the company announced that it had reached a five-year wage deal with its major union, the Association of Mine Workers and Construction Union (AMCU), for an average wage increase of 6.6% per annum.

On 28th November 2023, the company reported that 11 people had died and 75 were hospitalised following an incident at its No. 11 shaft in Rustenburg.

In its results for the year to 30th June 2024, the company reported revenue down 18.9% and headline earnings per share (HEPS) down 87.8%.

The company said, "Significantly weaker US dollar sales revenue offset the benefit of strong operational delivery in FY2024 - average palladium and rhodium pricing dropped sharply, negating higher sales volumes and compressing operating margins and free cash flow."

In an update on the first quarter to 30th September 2024, the company reported production volumes down by 5% but maintained production volume guidance.

The company said, "Implats is on track to deliver our previously provided operational, cost and capital expenditure guidance in FY2025."

In a trading statement for the six months to 31st December 2024, the company estimated that HEPS would fall by between 40% and 49% due to an 8% drop in the rand price of 6E PGMs, which offset cost controls and higher output.

Technically, the share was in a downward trend from March 2022 to March 2024, mainly as a result of lower PGM prices, increased costs, and load-shedding. It has recovered somewhat since then but remains a volatile commodity share.

Our opinion on the current state of BRIMSTON(BRT)Brimstone (BRT) is a black-controlled investment holding company with a diverse portfolio of holdings.

It owns:

1. 54.2% of Sea Harvest, which is a listed fishing company and has a market capitalisation of just over R4.5bn.

2. 100% of Lion of Africa, a loss-making insurance company, which decided in November 2018 to cease operations and close its doors.

3. 100% of House of Monatic, a loss-making clothing manufacturer.

4. 24% of Oceana, the largest fishing company in South Africa with a market capitalisation of R8.6bn. Brimstone is increasing its shareholding by buying 8m shares from Tiger Brands, which will take its holding to 22.9%.

5. 6.1% of Grindrod.

6. 18% of Aon Re Africa.

7. 25% of South African Enterprise Development.

8. 49.8% of Vuna Fishing company.

9. 12.8% of Milpark Education.

10. 25% of Obsidian (a black-owned investment holding firm positioned to benefit from the roll-out of the NHI), which in January 2020, it increased to 80% for R35.7m.

Additionally, Brimstone holds a variety of other smaller shareholdings in property, healthcare, 3.9% of Long4Life, and 5.3% of Stadio.

The company has been selling down its stakes in Life Healthcare, Lion of Africa, House of Monatic, Equites, Multichoice, and Phuthuma Nathi. It has used the proceeds to pay down R1bn of its debt.

In its results for the six months to 30th June 2024, the company reported revenue down 39% and headline earnings per share (HEPS) up 110%.

The company's intrinsic net asset value (NAV) fell 5.7% to 1143.6c per share.

The company said, "Despite the operating environment, the Group reported headline earnings per share of 71.9 cents (2023: 34.2 cents), up 110% over the comparative period. This was mainly due to fair value gains of R76.2 million compared to fair value losses of R40.3 million in the prior period, and the increase in Brimstone’s share of profits of associate, Oceana, from R94.9 million in the prior period to R187 million in the period under review."

The company disposed of its entire stake in Milpark and part-stakes in Phuthuma Nathi, MTN Zakhele Futhi, and Equites.

In a trading statement for the year to 31st December 2024, the company estimated that HEPS would be between 46% and 56% higher.

We regard the share as too thinly traded for private investors and, unless they begin to unbundle the portfolio, the extra value is likely to remain locked in.

Our opinion on the current state of KAPKAP International Holdings (KAP) is a diversified industrial company that produces and markets timber, chemicals (PET and related chemicals), bedding, and car parts. It also has a logistics division.

The acquisitions of Safripol and Hosaf were integrated into a polymers business under the Safripol name. The bedding division showed strong growth with new investment in infrastructure and manufacturing capability. Growth in the automotive parts division was muted.

This company was 43% owned by Steinhoff, which has now divested completely. The renewal of the government's Automotive Production and Development Programme (APDP) until 2035 will be a boost for KAP's parts manufacturing business.

The timber division is ramping up after the lockdown, and demand for its products has remained buoyant. The automotive components division was severely impacted, and the post-lockdown recommencement has been slow. The bedding division was able to operate through the lockdown with strong demand for medical and agricultural needs. Polymers also operated throughout the lockdown.

In a report on 20th April 2022 into the flooding in Natal, the company said, "The Company’s operations in the region have experienced some temporary operational and supply chain disruptions, which are in the process of being resolved."

In its results for the year to 30th June 2024, the company reported revenue down 2% and headline earnings per share (HEPS) down 4%. The company's net asset value (NAV) increased by 7% to 500c per share.

The company said, "...operating profit before depreciation, amortisation and capital items (‘EBITDA’) decreased by 8% to R3 694 million (2023: R4 020 million), while operating profit before capital items decreased by 11% to R2 250 million (2023: R2 523 million) for the year, with the decline mostly attributable to Safripol."

In an operational update on the five months to 30th November 2024, the company reported increased operating costs and finance costs.

The company said, "Revenue improved due to a c. 50% combined increase in MDF domestic and export sales volumes, primarily attributable to the higher MDF production."

In a trading statement for the six months to 31st December 2024, the company estimated that HEPS would fall by between 19% and 23%.

Technically, the share has been falling since September 2024, and we recommend waiting for it to break up through its downward trendline before investigating further.

Obviously, the logistics problems at Transnet have been having an impact. We think it may represent good value at current levels, but it is volatile.

Our opinion on the current state of NORTHAM(NPH)Northam (NPH) is a fully empowered platinum mining company that operates in the Bushveld complex.

In the current difficult legislative environment, where the 3rd mining charter is regarded as unfriendly from an investment point of view, Northam is probably the only mining house that is buying up new properties.

It has come to an arrangement with Anglo American to exploit a property adjacent to its Zondereinde mine (the deepest platinum mine in South Africa). It has also bought Eland Platinum from Glencore for R175m, which it intends to re-start at a cost of R2bn.

On 29th October 2019, the company announced the acquisition of Maroelabult for R20m, which is west of the Eland mine with an analogous ore body. This has accelerated the bringing to production of Eland and required very little capital. With the Eland mine, Northam got a concentrator plant that can process up to 250,000 tons a month. In return, Glencore got the right to market all of Northam's chrome.

At the same time, Northam has recently commissioned a new smelter to try to process its backlog of platinum ore, which is estimated to be worth about R2.5bn.

Zondereinde is a deep-level mine that has all the problems associated with mining at depth, while Booysendal is a shallow mechanised mine that is much easier to manage.

Both mines are profitable, but the empowerment structure results in Northam always reporting a loss because of the preference dividend that must be paid. Once Booysendal is complete, the company should generate strong cash flows.

The appointment of Mcebisi Jonas (former South African Minister of Finance) and Jean Nel (previously CEO of Aquarius Platinum) as non-executive directors will significantly add to the strength of the board.

The company has the stated intention of doubling its workforce as it strives to become a major PGM supplier in the world. With plans to increase production of PGMs over the next few years to 1 million ounces, this is probably one of the better options in the industry.

The company has also sold its Impala shares for R3.1bn.

The PGM industry is currently navigating significantly depressed PGM prices and high inflation, together with a raft of global geopolitical uncertainties and, locally, Eskom load curtailment events.

In its results for the year to 30th June 2024, the company reported revenue down 22.2% and headline earnings per share (HEPS) down 81.6%.

In a production update for the six months to 31st December 2024, the company reported refined PGM production up 3.7% and chrome production up 7.5%.

The company said, "PGM production from Zondereinde remains on target, despite a stoppage during November as a result of a failure of a primary Eskom feed substation. Chrome concentrate production has benefitted from increased UG2 milling and further incremental improvements in chrome recovery."

In a trading statement for the six months to 31st December 2024, the company estimated that HEPS would fall by between 44.7% and 54.7%.

Since April 2021, there has been a steady decline in the share, which has seen it fall back substantially. Despite this, we see a good future for this company in the longer term, but it remains a volatile commodity share.

We recommend waiting for a clear break up through the downward trendline before investigating further.

Our opinion on the current state of TRELLIDOR(TRL)RCL is a large producer of food, sugar products, and chicken in South Africa, which is owned 80.4% by Remgro.

The company owns a number of very well-known South African brands such as 5 Star maize meal, Farmer Brown, and Yum Yum peanut butter. It competes with overseas imports of sugar, chicken, and other foods.

It was impacted by the listeriosis outbreak, which damaged the market for processed meats and caused costs estimated at about R158m. The company has been impacted by the weak economy, low consumer spending, and high unemployment.

The company, through the SA Poultry Association, is petitioning the International Trade Administration Commission (ITAC) for an 82% increase in the tariffs on imported chicken.

On 2nd December 2020, the company announced that Remgro had increased its stake by buying 100m shares at R8,05 each.

On 29th March 2023, the company announced that it had sold Vector Logistics for R1,25bn.

On 4th June 2024, the company announced that it would unbundle and separately list Rainbow Chicken. RCL shareholders got 1 Rainbow share for every RCL share that they held on 25th June 2024.

On 10th June 2024, the company published Rainbow's pre-listing statement, with the last day to trade being 25th June 2024.

In its results for the year to 30th June 2024, the company reported revenue up 6.8% and headline earnings per share (HEPS) from continuing operations up 31%.

The company said, "EBITDA from continuing operations increased by 36.8% to R2 300,5 million (2023: R1 681,6 million). This was mainly driven by a strong result in our Sugar business unit and the recovery of service levels in the Pet Food business within Groceries."

In a trading statement for the six months to 31st December 2024, the company estimated that HEPS would increase by between 31.2% and 38.6%.

The company said the increase was, "...largely due to, amongst other items, the current period EPS including the non-cash gain realised on accounting for the unbundling of Rainbow, and the comparative period EPS including the gain on disposal of Vector Logistics."

The share has been drifting down since Rainbow was unbundled but may now be at the start of a new upward trend.

Our opinion on the current state of RCLRCL is a large producer of food, sugar products, and chicken in South Africa, which is owned 80.4% by Remgro.

The company owns a number of very well-known South African brands such as 5 Star maize meal, Farmer Brown, and Yum Yum peanut butter. It competes with overseas imports of sugar, chicken, and other foods.

It was impacted by the listeriosis outbreak, which damaged the market for processed meats and caused costs estimated at about R158m. The company has been impacted by the weak economy, low consumer spending, and high unemployment.

The company, through the SA Poultry Association, is petitioning the International Trade Administration Commission (ITAC) for an 82% increase in the tariffs on imported chicken.

On 2nd December 2020, the company announced that Remgro had increased its stake by buying 100m shares at R8,05 each.

On 29th March 2023, the company announced that it had sold Vector Logistics for R1,25bn.

On 4th June 2024, the company announced that it would unbundle and separately list Rainbow Chicken. RCL shareholders got 1 Rainbow share for every RCL share that they held on 25th June 2024.

On 10th June 2024, the company published Rainbow's pre-listing statement, with the last day to trade being 25th June 2024.

In its results for the year to 30th June 2024, the company reported revenue up 6.8% and headline earnings per share (HEPS) from continuing operations up 31%.

The company said, "EBITDA from continuing operations increased by 36.8% to R2 300,5 million (2023: R1 681,6 million). This was mainly driven by a strong result in our Sugar business unit and the recovery of service levels in the Pet Food business within Groceries."

In a trading statement for the six months to 31st December 2024, the company estimated that HEPS would increase by between 31.2% and 38.6%.

The company said the increase was, "...largely due to, amongst other items, the current period EPS including the non-cash gain realised on accounting for the unbundling of Rainbow, and the comparative period EPS including the gain on disposal of Vector Logistics."

The share has been drifting down since Rainbow was unbundled but may now be at the start of a new upward trend.

Our opinion on the current state of KUMBA-IO(KIO)Kumba (KIO) is a highly successful iron mining operation which is owned (79%) and controlled by Anglo American.

The share price fell to as little as R223 in March 2020 because of COVID-19 but recovered to R668 before falling on the March 2022 quarterly results.

Importantly, exports make up 94% of the company's total sales - which means that it is not heavily dependent on local sales but is vulnerable to any strengthening of the rand and the effectiveness of rail transport to ports.

The company is planning to build a 100MW solar park over the next 3 years to reduce its reliance on Eskom. The company has had to contend with heavy rain and bad rail performance.

On 10th October 2022, Kumba announced that, because of the force majeure at Transnet, it would lose about 50,000 tons of production per day, rising to 90,000 tons after 7 days as a direct result of the Transnet force majeure. Furthermore, they said they would lose about 120,000 tons of exports which will cost them about $8.5m a day in production and $11.7m in lost export revenue. The company is considering 490 retrenchments.

In its results for the six months to 30th June 2024, the company reported revenue down 6% and headline earnings per share (HEPS) down 26%. The average free-on-board (FOB) price received was $97 per ton with an EBITDA of 44%. The company had a closing cash position of R14.6bn.

The company said, "Attributable free cash flow of R9.1 billion supported our Board's decision to declare an interim dividend of R6.0 billion."

In an update on the 3 months to 30th September 2024, the company reported production up 3% and sales up 2%.

The company said, "...in comparison to Q2 2024, sales decreased by 6% as ship loading was impacted by adverse weather conditions in July 2024 at the Saldanha Bay port. Given this, sales are expected to end the year closer to the lower end of our full year 2024 sales guidance of 36 – 38 Mt, subject to Transnet's logistics performance..."

In a trading statement for the year to 31st December 2024, the company estimated that HEPS would fall by between 43% and 48%.

The company said, "Ore railed to Saldanha Bay Port decreased by 8% compared to Q3 2024, due to the planned 15-day annual maintenance shutdown and unfortunate train derailments following the re-opening of the Ore Export Channel (OEC). To maintain a balanced and efficient value chain, finished stock at the mines was drawn down and production reduced by 17% compared to Q3 2024, while sales increased by 1% to 9.1 Mt."

The share trades at a multiple of 5.62 and a dividend yield (DY) of 9.71% - which seems to compensate the investor to some extent for the commodity risk in this rand-hedge share, but it remains volatile and hence risky.

On 28th August 2024, the company announced that it would invest R11.2bn in improved processing technology at Sishen, which would improve premium quality production to 55% from the current level of 18%.