OPEN-SOURCE SCRIPT

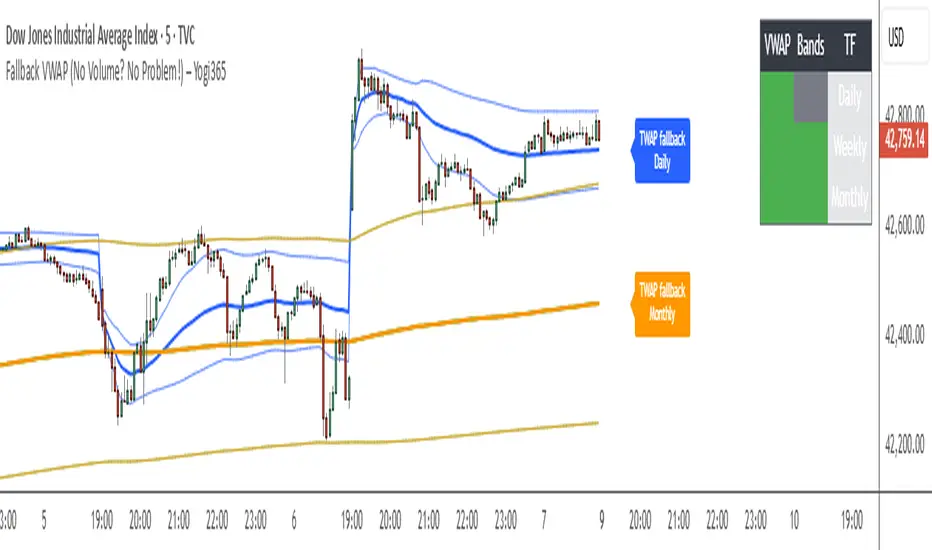

Fallback VWAP (No Volume? No Problem!) – Yogi365

Fallback VWAP (No Volume? No Problem!) – Yogi365

This script plots Daily, Weekly, and Monthly VWAPs with ±1 Standard Deviation bands. When volume data is missing or zero (common in indices or illiquid assets), it automatically falls back to a TWAP-style calculation, ensuring that your VWAP levels always remain visible and accurate.

Features:

Daily, Weekly, and Monthly VWAPs with ±1 Std Dev bands.

Auto-detection of missing volume and seamless fallback.

Clean, color-coded trend table showing price vs VWAP/bands.

Uses hlc3 for VWAP source.

Labels indicate when fallback is used.

Best Used On:

Any asset or index where volume is unavailable.

Intraday and swing trading.

Works on all timeframes but optimized for overlay use.

How it Works:

If volume == 0, the script uses a constant fallback volume (1), turning the VWAP into a TWAP (Time-Weighted Average Price) — still useful for intraday or index-based analysis.

This ensures consistent plotting on instruments like indices (e.g., NIFTY, SENSEX,DJI etc.) which might not provide volume on TradingView.

This script plots Daily, Weekly, and Monthly VWAPs with ±1 Standard Deviation bands. When volume data is missing or zero (common in indices or illiquid assets), it automatically falls back to a TWAP-style calculation, ensuring that your VWAP levels always remain visible and accurate.

Features:

Daily, Weekly, and Monthly VWAPs with ±1 Std Dev bands.

Auto-detection of missing volume and seamless fallback.

Clean, color-coded trend table showing price vs VWAP/bands.

Uses hlc3 for VWAP source.

Labels indicate when fallback is used.

Best Used On:

Any asset or index where volume is unavailable.

Intraday and swing trading.

Works on all timeframes but optimized for overlay use.

How it Works:

If volume == 0, the script uses a constant fallback volume (1), turning the VWAP into a TWAP (Time-Weighted Average Price) — still useful for intraday or index-based analysis.

This ensures consistent plotting on instruments like indices (e.g., NIFTY, SENSEX,DJI etc.) which might not provide volume on TradingView.

Open-source script

In true TradingView spirit, the creator of this script has made it open-source, so that traders can review and verify its functionality. Kudos to the author! While you can use it for free, remember that republishing the code is subject to our House Rules.

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.

Open-source script

In true TradingView spirit, the creator of this script has made it open-source, so that traders can review and verify its functionality. Kudos to the author! While you can use it for free, remember that republishing the code is subject to our House Rules.

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.