OPEN-SOURCE SCRIPT

Updated Volatility Adjusted EMA - by Crunchster

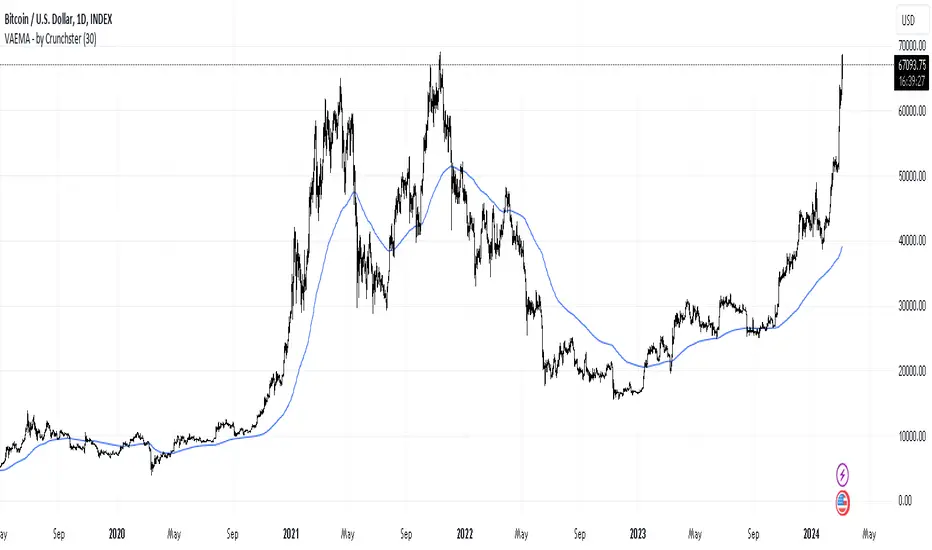

Applies recent volatility adjustment to the exponential moving average, where the smoothing factor is 2/(N + 1) - N being the lookback period or span

Volatility of recent 30 days returns is calculated using standard deviation with a thirty day lookback.

Increased smoothing compared to a standard EMA, which also adjusts to market conditions, as first described by Chande in 1991.

Volatility of recent 30 days returns is calculated using standard deviation with a thirty day lookback.

Increased smoothing compared to a standard EMA, which also adjusts to market conditions, as first described by Chande in 1991.

Release Notes

Minor code updateOpen-source script

In true TradingView spirit, the creator of this script has made it open-source, so that traders can review and verify its functionality. Kudos to the author! While you can use it for free, remember that republishing the code is subject to our House Rules.

Join me on Mizar.com and trade my strategies

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.

Open-source script

In true TradingView spirit, the creator of this script has made it open-source, so that traders can review and verify its functionality. Kudos to the author! While you can use it for free, remember that republishing the code is subject to our House Rules.

Join me on Mizar.com and trade my strategies

Disclaimer

The information and publications are not meant to be, and do not constitute, financial, investment, trading, or other types of advice or recommendations supplied or endorsed by TradingView. Read more in the Terms of Use.