Intraday Momentum StrategyExplanation of the StrategyIndicators:Fast and Slow EMA: A crossover of the 9-period EMA over the 21-period EMA signals a bullish trend (long entry), while a crossunder signals a bearish trend (short entry).

RSI: Ensures entries are not in overbought (RSI > 70) or oversold (RSI < 30) conditions to avoid reversals.

VWAP: Acts as a dynamic support/resistance. Long entries require the price to be above VWAP, and short entries require it to be below.

Trading Session:The strategy only trades during a user-defined session (e.g., 9:30 AM to 3:45 PM, typical for US markets).

All positions are closed at the session end to avoid overnight risk.

Risk Management:Stop Loss: 1% below/above the entry price for long/short positions.

Take Profit: 2% above/below the entry price for long/short positions.

These can be adjusted via inputs for optimization.

Position Sizing:Fixed lot size of 1 for simplicity. Adjust based on your account size during backtesting.

Educational

SulLaLuna PO3 Acceleration Tracker### 🚀 **Power of 3 Acceleration Script | Enter the Cave of Wonder 🧙♂️**

> *“When we find the God Candle, we don’t just ride it—we ritualize it.”*

> — The Calzolaio Way

🌕 The **SulLaLuna PO3 Acceleration Tracker** is a tool born from Smart Money theory, built with surgical logic, and forged to ride the **acceleration phase** with confluence and confidence.

Inspired by the teachings of (youtu.be), this indicator captures the moment of explosive expansion—the candle after the manipulation wick, the price action spark that ignites the trend.

---

### ⚔️ The PO3 Framework (ICT)

* **Accumulation** – Compression, trap laid

* **Manipulation** – Liquidity taken, fakeouts triggered

* **Expansion** – God Candle. This is where we enter.

This script automatically detects that exact **post-manipulation acceleration** candle and plots:

* ✅ TP/SL based on risk-reward

* ✅ Dynamic trend dashboard (15m to 1D)

* ✅ Long/Short trade markers

* ✅ Custom alerts and dashboard positioning

---

### 🔁 **Use Confluence**

> ⚠️ *No entry should ever be made on one signal alone.*

For optimal precision, pair this script with a **trend-strength and momentum filter**.

I personally use (), a brilliant tool that dynamically adapts to volatility and momentum changes using a responsive EMA and wave strength logic. It's CC BY-NC-SA 4.0 licensed and adds serious edge in distinguishing true trends from false breaks.

💡 Look for PO3 entries that align with:

* ✅ Bullish dominance in trend speed

* ✅ Dynamic EMA slope support

* ✅ MTF Trend agreement on the SulLaLuna dashboard

---

### ✨ The Cave of Wonder

This is more than just a script—this is your **map**.

The Cave of Wonder isn’t a place, it’s a **process**. Each PO3 entry is a torch lighting the path deeper into the vaults of financial freedom.

When you use this with **discipline**, **data**, and **divine timing**, you don't just take trades.

You take **territory**.

---

### 🔗 Try It. Trade It. Ritualize It.

🛠️ Built by @Calzolaio

🎓 Based on PO3 by @TheMovingAverage

📊 Powered by trend confluence from @Zeiierman

> “Capture the Acceleration. Honor the Trend. Trade with the Moon.” 🌕

Williams Percent Range with ThresholdEnhance your trading analysis with the "Williams Percent Range with Threshold" indicator, a powerful modification of the classic Williams %R oscillator. This custom version introduces customizable uptrend and downtrend thresholds, combined with dynamic candlestick coloring to visually highlight market trends. Originally designed to identify overbought and oversold conditions, this script takes it a step further by allowing traders to define specific threshold levels for trend detection, making it a versatile tool for momentum and trend-following strategies.

Key Features:

Customizable Thresholds: Set your own uptrend (default: -16) and downtrend (default: -67) thresholds to adapt the indicator to your trading style.

Dynamic Candlestick Coloring: Candles turn green during uptrends, red during downtrends, and gray in neutral conditions, providing an intuitive visual cue directly on the price chart.

Flexible Length: Adjust the lookback period (default: 50) to fine-tune sensitivity.

Overlay Design: Integrates seamlessly with your price chart, enhancing readability without clutter.

How It Works:

The Williams %R calculates the current closing price's position relative to the highest and lowest prices over a specified period, expressed as a percentage between -100 and 0. This version adds trend detection based on user-defined thresholds, with candlestick colors reflecting the trend state. The indicator plots the %R line with color changes (green for uptrend, red for downtrend) and includes dashed lines for the custom thresholds.

Usage Tips:

Use the uptrend threshold (-16 by default) to identify potential buying opportunities when %R exceeds this level.

Apply the downtrend threshold (-67 by default) to spot selling opportunities when %R falls below.

Combine with other indicators (e.g., moving averages or support/resistance levels) for confirmation signals.

Adjust the length and thresholds based on the asset's volatility and your trading timeframe.

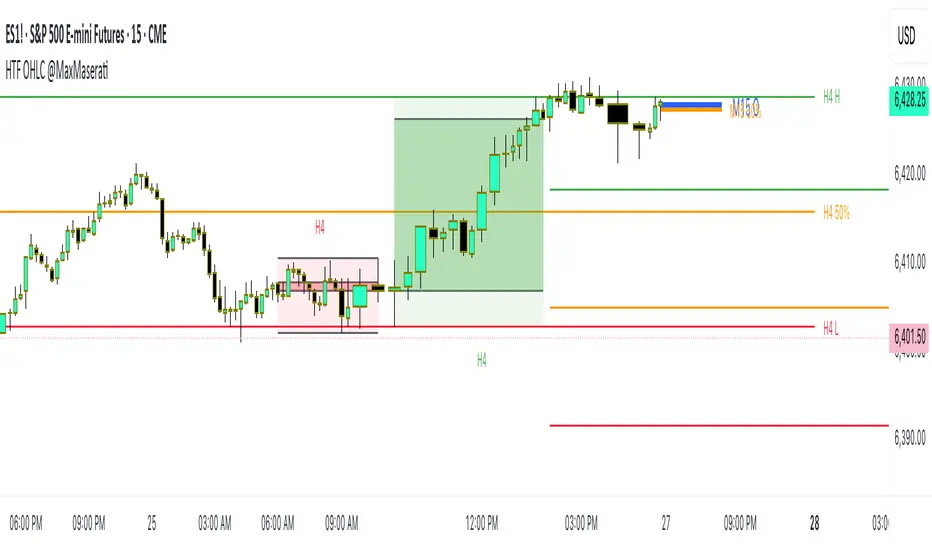

HTF OHLC Candle + 50% @MaxMaseratiHTF OHLC Candle + 50% @MaxMaserati

This advanced multi-timeframe indicator displays higher timeframe OHLC data as visual candle boxes and extended key levels on lower timeframe charts, providing essential context for institutional trading decisions.

Core Functionality:

Multi-Timeframe Box Display:

Main Timeframe Box (Default H4): Shows complete higher timeframe candles as colored boxes with separate body and wick visualization, including bullish (green) and bearish (red) candle representation with customizable transparency levels.

Independent Box 2 (Default M15): Secondary timeframe display with lime/fuchsia color scheme, allowing traders to monitor intermediate timeframes simultaneously with different visual styling.

Independent Box 3 (Default H1): Third independent timeframe with blue/orange color scheme, providing additional context for multi-timeframe analysis and confluence identification.

OHLC Level Analysis:

Each timeframe box includes individual Open, High, Low, and Close level lines with customizable colors and visibility settings. These levels act as key support and resistance zones that institutional traders often respect.

50% Retracement Levels:

Automatic calculation and display of 50% levels between each timeframe's high and low, representing critical equilibrium zones where price often finds support or resistance during retracements.

Extended Line System:

Current Live Timeframe Extended Lines: Real-time extension of the forming candle's Open, High, Low, and 50% levels with customizable line weights and label positioning.

TF2 Extended Lines (Default H4): Previous completed candle's key levels extended forward, showing immediate higher timeframe reference points for current price action.

TF3 Extended Lines (Default Daily): Longer-term reference levels from daily or weekly timeframes, providing macro trend context and major institutional levels.

Key Features:

Smart Timeframe Detection: Only displays boxes for timeframes higher than the current chart timeframe, preventing redundant information and maintaining chart clarity.

Global Box Limit Control: Intelligent cleanup system that maintains optimal performance by limiting total displayed elements while preserving the most recent and relevant timeframe periods.

Comprehensive Customization: Full control over colors, transparency, line weights, label sizes, and visibility for each timeframe component, allowing personalized setups for different trading styles.

Label System: Automatic timeframe identification labels (H4, M15, D1, etc.) positioned on each box for instant timeframe recognition and clear multi-timeframe organization.

Current Candle Options: Optional display of forming/current candles for each timeframe, enabling real-time monitoring of developing price action and potential setup completion.

This indicator is essential for traders utilizing multi-timeframe analysis, institutional trading concepts, and higher timeframe confluence strategies, providing clear visual representation of key levels and candle structures that drive major market movements.

S&R Zones MTF (TechnoBlooms)S&R Zones MTF – Multi-Timeframe Support & Resistance Boxes

🔍 Overview

S&R Zones MTF is a professional-grade yet beginner-friendly indicator that dynamically plots Support & Resistance zones across multiple timeframes, helping traders recognize high-probability reversal areas, entry confirmations, and price reaction points.

This tool visualizes structured zones as colored boxes, allowing both new and experienced traders to analyze multi-timeframe confluence with ease and clarity.

🧠 What Is This Indicator?

S&R Zones MTF automatically detects the most significant support and resistance levels from up to four custom timeframes, using a configurable lookback period. These zones are displayed as colored horizontal boxes directly on the chart, making it easy to:

Spot where price has historically reacted

Identify potential reversal or breakout zones

Confirm entries with institutional-style precision

🛠️ Key Features

✅ Multi-Timeframe Zone Detection (up to 4 timeframes)

📦 Auto Plotted Boxes for Support (Blue) & Resistance (Pink)

🧱 Dynamic Height based on average price range or fixed input

🏷️ Timeframe Labels to instantly identify zone origin

🎛️ Customizable inputs: Lookback length, box color, height style

🔁 Real-time updates as price structure changes

🎓 Educational & Easy to Use

Whether you’re a new trader learning about price structure, or a professional applying institutional concepts, this tool offers an educational layout to understand:

How price respects historic zones

Why multi-timeframe zones offer stronger confluence

How to use zones for entry, exit, or risk placement

📈 How to Use (Multi-Timeframe Strategy)

Select Your Timeframes – Customize up to 4 higher timeframes (e.g., 1m, 5m, 15m, 1h).

Observe Overlapping Zones – When multiple timeframes agree, those zones are more significant.

Entry Confirmation – Wait for price to reach a zone, then look for reversal patterns (engulfing candle, pin bar, etc.)

Combine with Other Tools – Use alongside indicators like RSI, MACD, or Order Blocks for added confidence.

💡 Pro Tips

Zones from higher timeframes (1H, 4H) are often more powerful and reliable.

Confluence matters: If a 15m support zone aligns with a 1H support zone — that's a high-probability reaction area.

Use break-and-retest strategies with zone rejections for sniper entries.

Enable "Auto Height" for a more adaptive, volatility-based zone display.

🌟 Summary

S&R Zones MTF blends precision, clarity, and professional analysis into a visual structure that’s easy to understand. Whether you're learning support & resistance or optimizing your MTF edge — this tool will bring clarity to your charts and confidence to your trades.

🗓️ Day Separator🗓️ Day Separator – Visual Day Markers for Your Chart

This script adds automatic vertical lines to visually separate each trading day on your chart. It helps you quickly identify where each day starts and ends — especially useful for intraday and scalping strategies.

✅ Features:

Distinct colored lines for each weekday (Monday to Friday)

Optional day-of-week labels (toggle on/off)

Custom label position (top or bottom of the chart)

Works on any timeframe

Whether you're tracking market sessions or reviewing daily price action, this tool gives you a clean structure to navigate your charts with more clarity.

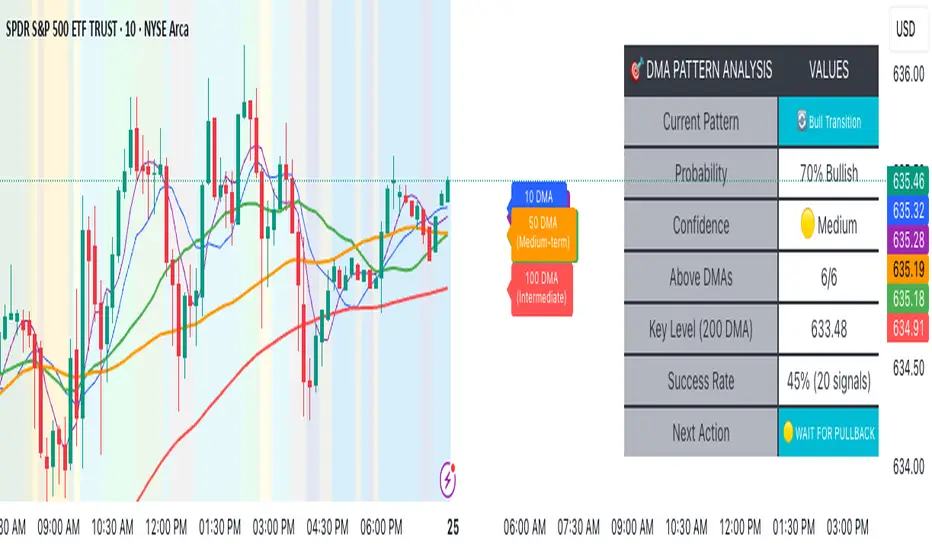

Advanced DMA Pattern Detection SystemAdvanced DMA Pattern Detection System with Smart Intelligence

Professional-grade moving average indicator that combines traditional DMA analysis with advanced pattern recognition and probabilistic forecasting.

Core Features:

6 Key DMAs (5, 10, 20, 50, 100, 200) with descriptive labels showing trading purpose

Advanced Pattern Recognition - Detects Institutional Accumulation, Distribution Phases, Bull/Bear Transitions, and Choppy Markets

Probability Engine - Assigns confidence scores (0-100%) with Low/Medium/High classifications

Historical Validation - Tracks success rate of last 20 pattern signals for real performance data

Smart Alert System - Only triggers on significant pattern changes (20%+ probability shifts)

Dual Display System:

Movable Information Table - Shows current pattern, probability, confidence level, success rate, and recommended action

Chart Alerts & Background Colors - Visual confirmation of high-confidence setups (80%+ patterns)

Traditional DMA Labels - Clear identification of each average's trading significance

Complete Customization:

Master on/off controls for entire system

Individual toggles for all components (DMAs, table, alerts, colors)

Adjustable alert sensitivity (Conservative/Medium/Aggressive)

6 table positions to fit any chart layout

Perfect For: Swing traders, position traders, and anyone wanting systematic trend analysis with quantified probability scores rather than subjective interpretation.

Bottom Line: Transforms basic moving averages into an intelligent trading system that tells you exactly what the market structure means and what to do about it.

BE-Indicator Aggregator toolkit█ Overview:

BE-Indicator Aggregator toolkit is a toolkit which is built for those we rely on taking multi-confirmation from different indicators available with the traders. This Toolkit aid's traders in understanding their custom logic for their trade setups and provides the summarized results on how it performed over the past.

█ How It Works:

Load the external indicator plots in the indicator input setting

Provide your custom logic for the trade setup

Set your expected SL & TP values

█ Legends, Definitions & Logic Building Rules:

Building the logic for your trade setup plays a pivotal role in the toolkit, it shall be broken into parts and toolkit aims to understand each of the logical parts of your setup and interpret the outcome as trade accuracy.

Toolkit broadly aims to understand 4 types of inputs in "Condition Builder"

Comments : Line which starts with single quotation ( ' ) shall be ignored by toolkit while understanding the logic.

Note: Blank line space or less than 3 characters are treated equally to comments.

Long Condition: Line which starts with " L- " shall be considered for identifying Long setups.

Short Condition: Line which starts with " S- " shall be considered for identifying Short setups.

Variables: Line which starts with " VAR- " shall be considered as variables. Variables can be one such criteria for Long or short condition.

Building Rules: Define all variables first then specify the condition. The usual declare and assign concept of programming. :p)

Criteria Rules: Criteria are individual logic for your one parent condition. multiple criteria can be present in one condition. Each parameter should be delimited with ' | ' key and each criteria should be delimited with ' , ' (Comma with a space - IMPORTANT!!!)

█ Sample Codes for Conditional Builder:

For Trading Long when Open = Low

For Trading Short when Open = High with a Red candle

'Long Setup <---- Comment

L-O|E|L

' E <- in the above line refers to Equals ' = '

'Short Setup

S-AND:O|E|H, O|G|C

' 2 Criteria for used building one condition. Since, both have to satisfied used "AND:" logic.

Understanding of Operator Legends:

"E" => Refers to Equals

"NE" => Refers to Not Equals

"NEOR" => Logical value is Either Comparing value 1 or Comparing value 2

"NEAND" => Logical value is Comparing value 1 And Comparing value 2

"G" => Logical value Greater than Comparing value 1

"GE" => Logical value Greater than and equal to Comparing value 1

"L" => Logical value Lesser than Comparing value 1

"LE" => Logical value Lesser than and equal to Comparing value 1

"B" => Logical value is Between Comparing value 1 & Comparing value 2

"BE" => Logical value is Between or Equal to Comparing value 1 & Comparing value 2

"OSE" => Logical value is Outside of Comparing value 1 & Comparing value 2

"OSI" => Logical value is Outside or Equal to Comparing value 1 & Comparing value 2

"ERR" => Logical value is 'na'

"NERR" => Logical value is not 'na'

"CO" => Logical value Crossed Over Comparing value 1

"CU" => Logical value Crossed Under Comparing value 1

Understanding of Condition Legends:

AND: -> All criteria's to be satisfied for the condition to be True.

NAND: -> Output of AND condition shall be Inversed for the condition to be True.

OR: -> One of criteria to be satisfied for the condition to be True.

NOR: -> Output of OR condition shall be Inversed for the condition to be True.

ATLEAST:X: -> At-least X no of criteria to be satisfied for the condition to be True.

Note: "X" can be any number

NATLEAST:X: -> Output of ATLEAST condition shall be Inversed for the condition to be True

WASTRUE:X: -> Single criteria WAS TRUE within X bar in past for the condition to be True.

Note: "X" can be any number.

ISTRUE:X: -> Single criteria is TRUE since X bar in past for the condition to be True.

Note: "X" can be any number.

Understanding of Variable Legends:

While Condition Supports 8 Types, Variable supports only 6 Types listed below

AND: -> All criteria's to be satisfied for the Variable to be True.

NAND: -> Output of AND condition shall be Inversed for the Variable to be True.

OR: -> One of criteria to be satisfied for the Variable to be True.

NOR: -> Output of OR condition shall be Inversed for the Variable to be True.

ATLEAST:X: -> At-least X no of criteria to be satisfied for the Variable to be True.

Note: "X" can be any number

NATLEAST:X: -> Output of ATLEAST condition shall be Inversed for the Variable to be True

█ Sample Outputs with Logics:

1. RSI Indicator + Technical Indicator: StopLoss: 2.25 against Reward ratio of 1.75 (3.94 value)

Plots Used in Indicator Settings:

Source 1:- RSI

Source 2:- RSI Based MA

Source 3:- Strong Buy

Source 4:- Strong Sell

Logic Used:

For Long Setup : RSI Should be above RSI Based MA, RSI has been Rising when compared to 3 candles ago, Technical Indicator signaled for a Strong Buy on the current candle, however in last 6 candles Technical indicator signaled for Strong Sell.

Similarly Inverse for Short Setup.

L-AND:ES1|GE|ES2, ES1|G|ES1

L-ES3|E|1

L-OR:ES4 |E|1, ES4 |E|1, ES4 |E|1, ES4 |E|1, ES4 |E|1, ES4 |E|1

S-AND:ES1|LE|ES2, ES1|L|ES1

S-ES4|E|1

S-OR:ES3 |E|1, ES3 |E|1, ES3 |E|1, ES3 |E|1, ES3 |E|1, ES3 |E|1

'Note: Last OR condition can also be written by using WASTRUE definition like below

'L-WASTRUE:6:ES4|E|1

'S-WASTRUE:6:ES3|E|1

Output:

2. Volumatic Support / Resistance Levels :

Plots Used in Indicator Settings:

Source 1:- Resistance

Source 2:- Support

Logic Used:

For Long Setup : Long Trade on Liquidity Support.

For Short Setup : Short Trade on Liquidity Resistance.

'Variable Named "ChkLowTradingAbvSupport" is declared to check if last 3 candles is trading above support line of liquidity.

VAR-ChkLowTradingAbvSupport:AND:L|G|ES2, L |G|ES2, L |G|ES2

'Variable Named "ChkCurBarClsdAbv4thBarHigh" is declared to check if current bar closed above the high of previous candle where the Liquidity support is taken (4th Bar).

VAR-ChkCurBarClsdAbv4thBarHigh:OR:C|GE|H , L|G|H

'Combining Condition and Variable to Initiate Long Trade Logic

L-L |LE|ES2

L-AND:ChkLowTradingAbvSupport, ChkCurBarClsdAbv4thBarHigh

VAR-ChkHghTradingBlwRes:AND:H|L|ES1, H |L|ES1, H |L|ES1

VAR-ChkCurBarClsdBlw4thBarLow:OR:C|LE|L , H|L|L

S-H |GE|ES1

S-AND:ChkHghTradingBlwRes, ChkCurBarClsdBlw4thBarLow

Output 1: Day Trading Version

Output 2: Scalper Version

Output 3: Position Version

Gold vs DXYThe 30-day rolling correlation between Gold (XAU/USD) and the US Dollar Index (DXY) shows how closely the two move together — or more often, in opposite directions — over the last 30 trading days. In most market environments, the relationship is pretty straightforward: when the dollar goes up, gold tends to go down, and vice versa. That’s because gold is priced in dollars, so a stronger dollar makes it more expensive for international buyers, which usually softens demand.

But it’s not always that simple. There are times when this inverse correlation breaks down. For example, if real yields (like the US 10-year yield minus inflation expectations) are rising, that can pressure gold even if the dollar is falling — because higher real returns elsewhere make gold less attractive. Another case is when other currencies, like the euro or yen, rally strongly on their own central bank decisions. This can pull DXY lower without necessarily signaling weakness in the U.S. economy — meaning gold might not benefit much.

There are also “risk-on” moments where investors rotate into equities or crypto, selling off both gold and the dollar in favor of yield or momentum. And during periods of crisis or uncertainty, both gold and the dollar can rise together as safe-haven assets, breaking the usual pattern entirely.

That’s why tracking the rolling correlation is helpful. It shows whether the historical relationship between gold and the dollar is still holding — or if we’re entering a different market regime. It’s not about predicting exact price moves, but about understanding the current backdrop. When gold and DXY are moving out of sync as expected, it can support your trade thesis. But when the correlation flattens or flips, it’s often a sign to dig deeper — macro forces may be shifting.

🧪 Yuri Garcia Smart Money Strategy FULL (Slope Divergence))📣 Yuri Garcia – Smart Money Strategy FULL

This is my private Smart Money Concept strategy, designed for my family and community to learn, trade, and grow sustainably.

🔑 How it works:

✅ Volume Cluster Zones: Automatically detects areas where strong buyers or sellers concentrate, acting as dynamic S/R levels.

✅ HTF Institutional Zones (4H): Higher timeframe trend filter ensures you’re always trading in the direction of major flows.

✅ Wick Pullback Filter: Confirms price rejects the zone, catching smart money traps and reversals.

✅ Cumulative Delta (CVD): Confirms whether buyers or sellers are truly in control.

✅ Slope-Based Divergence: Optional hidden divergence between price & CVD to spot reversals others miss.

✅ ATR Dynamic SL/TP: Adapts stop loss and take profit to live volatility with adjustable risk/reward.

🧩 Visual Markers Explained:

🟦 Blue X: Price inside HTF zone

🟨 Yellow X: Price inside Volume Cluster zone

🟧 Orange Circle: Wick pullback detected

🟥 Red Square: CVD confirms order flow strength

🔼 Aqua Triangle Up: Bullish slope divergence

🔽 Purple Triangle Down: Bearish slope divergence

🟢 Green Triangle Up: Final Long Entry confirmed

🔴 Red Triangle Down: Final Short Entry confirmed

⚡ Who is this for?

This strategy is best suited for traders who understand smart money concepts, order flow, and want an adaptive framework to trade major assets like BTC, Gold, SP500, NASDAQ, or FX pairs.

🔒 Important

Use responsibly, backtest extensively, and combine with solid risk management. This is for educational purposes only.

✨ Credits

Built with ❤️ by Yuri Garcia – dedicated to my family & community.

✅ How to use it

1️⃣ Add to chart

2️⃣ Adjust inputs for your asset & timeframe

3️⃣ Enable/disable slope divergence filter to match your style

4️⃣ Set your alerts with built-in conditions

Volume Delta Pressure Tracker ⚡ by GSK-VIZAG-AP-INDIA📢 Title:

Volume Delta Pressure Tracker ⚡ by GSK-VIZAG-AP-INDIA

📝 Short Description (for script title box):

Real-time volume pressure tracker with estimated Buy/Sell volumes and Delta visualization in an Indian-friendly format (K, L, Cr).

📃 Full Description

🔍 Overview:

This indicator estimates buy and sell volumes using candle structure (OHLC) and displays a real-time delta table for the last N candles. It provides traders with a quick view of volume imbalance (pressure) — often indicating strength behind price moves.

📊 Features:

📈 Buy/Sell Volume Estimation using the candle’s OHLC and Volume.

⚖️ Delta Calculation (Buy Vol - Sell Vol) to detect pressure zones.

📅 Time-stamped Table displaying:

Time (HH:MM)

Buy Volume (Green)

Sell Volume (Red)

Delta (Color-coded)

🔢 Indian Number Format (K = Thousands, L = Lakhs, Cr = Crores).

🧠 Fully auto-calculated — no need for tick-by-tick bid/ask feed.

📍 Neatly placed bottom-right table, customizable number of rows.

🛠️ Inputs:

Show Table: Toggle the table on/off

Number of Bars to Show: Choose how many recent candles to include (5–50)

🎯 Use Cases:

Identify hidden buyer/seller strength

Detect volume absorption or exhaustion

✅ Compatibility:

Works on any timeframe

Ideal for intraday instruments like NIFTY, BANKNIFTY, etc.

Ideal for volume-based strategy confirmation.

🖋️ Developed by:

GSK-VIZAG-AP-INDIA

ATR: Тело % + Диапазоны и АномалииEssentially, this combined indicator is a powerful tool for:

Analyzing candlestick anatomy: Quickly understanding how much of a candlestick’s overall range is in its body, indicating the strength of buying or selling pressure versus uncertainty.

Volatility estimates: Understanding the typical pip range of bars, adjusted for the tick size of the instrument.

Identifying anomalies: Highlighting unusually small or large bar ranges that may signal changes in market momentum or significant events.

Average range filtering: Providing a clearer picture of average market volatility by excluding extreme outliers from the calculation.

This comprehensive approach can help traders make more informed decisions by gaining a deeper understanding of the nuances of price action and market volatility.

SessionsSession 10-12 12-16 1630-1830

Including HOD/LOD for different sessions.

Session 10:00 - 12: 00

Session 12:00 - 16:00

Session 16:30 - 18:30

Bollinger Bands📊 Bollinger Bands Strategy: Ride the Waves of Volatility 🌊

Bollinger Bands are a powerful tool to identify overbought and oversold conditions, volatility breakouts, and price reversals. This strategy uses:

🔹 Middle Band – 20-period simple moving average

🔹 Upper & Lower Bands – 2 standard deviations away from the SMA

💡 Strategy Logic:

Buy Entry: When price closes below the lower band and RSI < 30 → Expect mean reversion.

Sell Entry: When price closes above the upper band and RSI > 70 → Possible pullback.

Exit: Near middle band or opposite band.

📈 You can also use Bollinger Band squeezes to detect upcoming breakouts. Less distance = low volatility → Expansion = potential big move!

🧠 Great for swing trading or intraday scalping with proper risk management.

HMA Trend Line (Croc Signal Line)HMA Trend Line (Croc Signal Line) — The Ultimate Hull Moving Average Trend Indicator

Full English description here:

What is the HMA Trend Line (Croc Signal Line)?

The HMA Trend Line (Croc Signal Line) is a powerful, adaptive trend indicator for TradingView, based on the Hull Moving Average (HMA). This indicator is designed to help traders identify real market trends with less lag and reduced noise compared to traditional moving averages like SMA (Simple Moving Average) and EMA (Exponential Moving Average).

Why use the HMA Trend Line?

+ Faster Trend Detection: The Hull Moving Average (HMA) responds more quickly to price action, giving you earlier buy and sell signals.

+ Smoother and Cleaner: It provides a visually clean trend line that avoids the choppiness of classic EMAs and SMAs.

+ Reduced Lag: The HMA Trend Line follows the market closer, helping you avoid late entries or exits and spot trend reversals sooner.

+ Dynamic Support and Resistance: Use the line as a dynamic support or resistance to manage trades and identify pullbacks or breakouts.

What does “Croc Signal Line” mean?

The “Croc” in Croc Signal Line stands for:

+ Clean

+ Responsive

+ Optimized

+ Curve

This highlights the unique advantage of this indicator: a curve that is both fast-reacting and smooth, helping traders focus on real trends and filter out market noise.

How does the Hull Moving Average (HMA) work?

The HMA was developed by Alan Hull and uses weighted moving averages and a unique calculation to deliver both responsiveness and smoothness. Unlike standard moving averages, the HMA reacts faster to new price moves and avoids false signals in ranging or volatile markets.

How to use the HMA Trend Line (Croc Signal Line) on TradingView?

+ Watch for price crossing above the trend line for potential bullish signals, and below for bearish signals.

+ Use on any timeframe: from 1-minute scalping to daily, weekly, or even monthly charts.

+ Works with all asset classes: Forex, stocks, indices, cryptocurrencies, commodities, and futures.

+ Combine with other indicators (like Stochastics, RSI, or volume) for confirmation and to build your unique trading strategy.

+ Adjust the Signal Line Period for your market and style: shorter periods for faster markets, longer for smoother trends.

Who should use this indicator?

+ Day traders, swing traders, and long-term investors looking for reliable, actionable trend signals.

+ Anyone seeking a cleaner, more responsive alternative to the classic moving averages.

+ Traders who want a simple, visually clear way to filter out market noise and see real price direction.

Disclaimer:

This indicator is for educational and study purposes only. Please perform your own backtesting and analysis before using it in live trading. This script does not constitute financial advice. Use at your own risk.

--------

📊 Bot-Activated Signal OverlayThis script blends momentum, volume confirmation, and trend analysis to make signals more reliable — especially for flagged tickers you’re watching closely. You could even layer in alerts or refine the thresholds if you want a tighter grip on signal quality.

DR OF ORB ( MEROOOO )this indicator marks the first 15 min candle of each session

if the market closed above the box go long with stop loss blow the box

and vice versa

Fair Value MSThis indicator introduces rigid rules to familiar concepts to better capture and visualize Market Structure and Areas of Support and Resistance in a way that is both rule-based and reactive to market movements.

Typical "Market Structure" or "Zig-Zag" methods determine swing points based on fixed thresholds (length or percentage). While this does provide rigid structure, the results may be lagging or confusing due to the timing, since it is fixed to static parameters.

I believe the concept of Fair Value Gaps can solve this problem.

As you will notice, there are no length settings in this indicator.

> FVG Market Structure

Fair Value Gaps are a well known concept used to indicate directional intent, forming when price moves aggressively in one direction, leaving behind an imbalance between buyers and sellers. While the term FVG was popularized by ICT, the underlying concept predates them, known historically as imbalances, inefficiencies, or liquidity voids in institutional trading.

Note: For simplicity, in this indicator they'll be called FVGs.

By reading into this, we are able to clearly and rigidly define market structure simply by "looking" at the chart, using objective price events rather than subjective interpretation, or lengths.

By using FVGs to determine structure direction, the length, and speed of identification lies entirely on the market. If an FVG Down occurs immediately after a New Higher High forms, it is reasonable to assume there was a seller at that point, so the script would indicate a New Swing High.

The script is NOT stuck, waiting for a % retrace, or # bars to pass to identify it as such.

Sometimes the market is in a steady trend in a single direction and no FVGs form; therefore, no structure forms. -> Why would we try to impose structure on a clear trend?

Ultimately, the FVG Structure Method uses real reactions from the market to determine Market structure, and is not fixed to specific parameters.

As with other market structure indicators, "Market Structure Breaks" are still identifiable when price moves outside the most recent swing points.

These are helpful to indicate larger direction. In the following section you will see how these help us determine when we should start the search for an "Area of Interest (AOI)".

> Areas of Interest (AOIs)

"Area of Interest (AOI)" is a generalized term, and could refer to many types of zones you might recognize under different names. While the AOIs in this indicator are specialized in their own way, I have chosen to simply use the term "Area of Interest" because it’s more important to understand how they behave and why they exist than to focus on what they’re called.

The goal of an AOI is to point out reasonable areas where buyers or sellers may be staging, as is typical with support and resistance.

In order to reasonably identify these areas, we look for cause and effect relationships. When considering these relationships, it's easier to understand the placement of the points to define each zone.

(Buyer Examples)

Cause: Strong Buyers step in at Swing Low

Effect: Fair Value Gap Forms

Cause: Sustained Buying Pressure

Effect: Market Structure Breaks

In this example, The zone is drawn from the Swing Low, to the Bottom of the FVG closest to the swing point.

In theory, the participation at the swing point was strong and aggressive enough to create the FVG imbalance. Which then found acceptance and continued into a Market Structure Break. So with these AOIs, we are trying to locate the aggressive Buyers or Sellers which were positioned BEFORE the FVG.

These Zones are intended to act as areas to look for reactions from market participants, to judge where price may be going. When revisiting these zones, we look for a reaction or a break, to further provide us information to if the buyers or sellers are still there.

As seen in the screenshot above, The information we gain is not from the creation of these zones, but from the behavior we witness when these zones are revisited.

Technical Note: In this indicator, Market Structure Breaks are only considered when price closes outside the recent swing points. Wicks are not considered as confirmation, therefore are not used to detect structural breaks.

Inside each AOI you can optionally display a readout of the volume which accumulated during the time starting at the swing point and going until the closing bar of the FVG.

Note: We are counting volume until the closing bar of the FVG since the FVG is a 3 bar formation, and aggressive volume is required throughout to create the imbalance.

There are multiple FVGs that typically occur in a single direction, but we do not look to every single one to be indicative of structure, only the first FVG in the opposite direction of the previous direction (which is determined by previous FVGs)

You will probably notice, the AOIs do not form from the closest swing or FVG to the break, this is because we are targeting larger directional changes to draw these AOIs from.

Since they do not always happen perfectly every time, the AOI formation waits for an FVG to occur AND a Market structure break to happen. One without the other will result in no Zone displaying.

> Reflection Lines

While they may seem slightly redundant, Reflection Lines serve as reminders of previous support and resistance pivots. They are drawn at the same Pivots where and AOI is formed, and extend beyond the mitigation of the AOI.

These lines are often points of price to look for "Support Flips", a re-test pattern where price trades through previous support (or resistance) then returns to it and rejects, continuing into a larger move or trend.

Their namesake is based on the behavior of price, "reflecting" at these levels.

The Reflection lines are simple and change color based on price's location.

If price is above, we would typically look to a reflection line in with support in mind.

As a basic filter, these lines use an average price to determine their color, this way they will not change their color as frequently in choppy situations.

> Session Start/End Lines

For analysis purposes and trade review, it is helpful to analyze with context.

For that reason, I have implemented start and end session lines into the indicator, these are helpful when reviewing historical charts to not provide additional context.

By default, they are set to the NYSE Session, but can be changed to fit any needs.

These lines are not advanced, and simply draw a line as the chart passes the start and end of the sessions. It's very likely that you may need to adjust the session for your specific needs.

Note: The Timezone can be adjusted within the code if needed. By Default, the indicator uses "America/New_York" Timezone.

> Conclusion

If you’ve ever felt like your structure tools were confusing or lagging, drawing zones too late, or zones that simply don't make sense, this should feel like a breath of fresh air.

By removing arbitrary length settings and instead using FVGs to define structure and as a basis for AOIs, you're getting a more accurate look at what price is doing and where it's reacting from.

This indicator is rule-based, reactive, and aims to keep things logical without fluff or false confidence.

Enjoy!

TheDevashishratio-MomentumThis custom momentum indicator is inspired by Fibonacci principles but builds a unique sequence with steps of 0.5 (i.e., 0, 0.5, 1, 1.5, 2, ...). Instead of traditional Fibonacci numbers, each step functions as a dynamic lookback period for a momentum calculation. By cycling through these fractional steps, you capture a layered view of price momentum over varying intervals.

The "Fibonacci" Series Used

Sequence:

0, 0.5, 1, 1.5, 2, … up to a user-defined maximum

For trading indicators, lag values (lookback) must be integers, so each step is rounded to the nearest integer and duplicates are removed, resulting in lookbacks:

1, 2, 3, 4, ... N

Indicator Logic

For each selected lookback, the indicator calculates momentum as:

Momentum

n

=

close

−

close

Momentum

n

=close−close

Where:

close = current price

n = integer from your series of

You can combine these momenta for an averaged or weighted momentum profile, displaying the composite as an oscillator.

How To Use

Bullish: Oscillator above zero indicates positive composite momentum.

Bearish: Oscillator below zero indicates negative composite momentum.

Crosses: A cross from below to above zero may signal emerging bullish momentum, and vice versa.

Customization

Adjust max_step to control how many interval lags you want in your composite.

This oscillator averages across many short and mid-term momenta, reducing noise while still being sensitive to changes.

Summary

TheDevashishratio-Momentum offers a fresh momentum oscillator, blending a "Fibonacci-like" progression with technical analysis, and can be easily copy-pasted into TradingView to experiment and refine your edge.

For more on momentum indicator logic or how to use arrays and series in Pine Script, explore TradingView's official documentation and open-source scripts

Momentum_EMABand📢 Reposting this script as the previous version was shut down due to house rules. Follow for future updates.

The Momentum EMA Band V1 is a precision-engineered trading indicator designed for intraday traders and scalpers. This first version integrates three powerful technical tools — EMA Bands, Supertrend, and ADX — to help identify directional breakouts while filtering out noise and choppy conditions.

How the Indicator Works – Combined Logic

This script blends distinct but complementary tools into a single, visually intuitive system:

1️⃣ EMA Price Band – Dynamic Zone Visualization

Plots upper and lower EMA bands (default: 9-period) to form a dynamic price zone.

Green Band: Price > Upper Band → Bullish strength

Red Band: Price < Lower Band → Bearish pressure

Yellow Band: Price within Band → Neutral/consolidation zone

2️⃣ Supertrend Overlay – Reliable Trend Confirmation

Based on customizable ATR length and multiplier, Supertrend adds a directional filter.

Green Line = Uptrend

Red Line = Downtrend

3️⃣ ADX-Based No-Trade Zone – Choppy Market Filter

Manually calculated ADX (default: 14) highlights weak trend conditions.

ADX below threshold (default: 20) + Price within Band → Gray background, signaling low-momentum zones.

Optional gray triangle marker flags beginning of sideways market.

Why This Mashup & How the Indicators Work Together

This mashup creates a high-conviction, rules-based breakout system:

Supertrend defines the primary trend direction — ensuring trades are aligned with momentum.

EMA Band provides structure and timing — confirming breakouts with retest logic, reducing false entries.

ADX measures trend strength — filtering out sideways markets and enhancing trade quality.

Each component plays a specific role:

✅ Supertrend = Trend bias

✅ EMA Band = Breakout + Retest validation

✅ ADX = Momentum confirmation

Together, they form a multi-layered confirmation model that reduces noise, avoids premature entries, and improves trade accuracy.

💡 Practical Application

Momentum Breakouts: Enter when price breaks out of EMA Band with Supertrend confirmation

Avoid Whipsaws: Skip trades during gray-shaded low-momentum periods

Intraday Scalping Edge: Tailored for lower timeframes (5min–15min) where noise is frequent

⚠️ Important Disclaimer

This is Version 1 — expect future enhancements based on trader feedback.

This tool is for educational purposes only. No indicator guarantees profitability. Use with proper risk management and strategy validation.

Strategy Chameleon [theUltimator5]Have you ever looked at an indicator and wondered to yourself "Is this indicator actually profitable?" Well now you can test it out for yourself with the Strategy Chameleon!

Strategy Chameleon is a versatile, signal-agnostic trading strategy designed to adapt to any external indicator or trading system. Like a chameleon changes colors to match its environment, this strategy adapts to match any buy/sell signals you provide, making it the ultimate backtesting and automation tool for traders who want to test multiple strategies without rewriting code.

🎯 Key Features

1) Connects ANY external indicator's buy/sell signals

Works with RSI, MACD, moving averages, custom indicators, or any Pine Script output

Simply connect your indicator's signal output to the strategy inputs

2) Multiple Stop Loss Types:

Percentage-based stops

ATR (Average True Range) dynamic stops

Fixed point stops

3) Advanced Trailing Stop System:

Percentage trailing

ATR-based trailing

Fixed point trailing

4) Flexible Take Profit Options:

Risk:Reward ratio targeting

Percentage-based profits

ATR-based profits

Fixed point profits

5) Trading Direction Control

Long Only - Bull market strategies

Short Only - Bear market strategies

Both - Full market strategies

6) Time-Based Filtering

Optional trading session restrictions

Customize active trading hours

Perfect for day trading strategies

📈 How It Works

Signal Detection: The strategy monitors your connected buy/sell signals

Entry Logic: Executes trades when signals trigger during valid time periods

Risk Management: Automatically applies your chosen stop loss and take profit levels

Trailing System: Dynamically adjusts stops to lock in profits

Performance Tracking: Real-time statistics table showing win rate and performance

⚙️ Setup Instructions

0) Add indicator you want to test, then add the Strategy to your chart

Connect Your Signals:

imgur.com

Go to strategy settings → Signal Sources

1) Set "Buy Signal Source" to your indicator's buy output

2) Set "Sell Signal Source" to your indicator's sell output

3) Choose table position - This simply changes the table location on the screen

4) Set trading direction preference - Buy only? Sell only? Both directions?

imgur.com

5) Set your preferred stop loss type and level

You can set the stop loss to be either percentage based or ATR and fully configurable.

6) Enable trailing stops if desired

imgur.com

7) Configure take profit settings

8) Toggle time filter to only consider specific time windows or trading sessions.

🚀 Use Cases

Test various indicators to determine feasibility and/or profitability.

Compare different signal sources quickly

Validate trading ideas with consistent risk management

Portfolio Management

Apply uniform risk management across different strategies

Standardize stop loss and take profit rules

Monitor performance consistently

Automation Ready

Built-in alert conditions for automated trading

Compatible with trading bots and webhooks

Easy integration with external systems

⚠️ Important Notes

This strategy requires external signals to function

Default settings use 10% of equity per trade

Pyramiding is disabled (one position at a time)

Strategy calculates on bar close, not every tick

🔗 Integration Examples

Works perfectly with:

RSI strategies (connect RSI > 70 for sells, RSI < 30 for buys)

Moving average crossovers

MACD signal line crosses

Bollinger Band strategies

Custom oscillators and indicators

Multi-timeframe strategies

📋 Default Settings

Position Size: 10% of equity

Stop Loss: 2% percentage-based

Trailing Stop: 1.5% percentage-based (enabled)

Take Profit: Disabled (optional)

Trade Direction: Both long and short

Time Filter: Disabled

Volumen Spike Übersicht (10 Symbole) Ultima by James_BLThe script checks up to 10 volume sources simultaneously to see if they are above average.

There is also a volume spike factor that allows you to specify the strength compared to the average.

It supports alerts for each individual volume or for any one out of ten, which minimizes the limited number of available alerts.

✅ TrendSniper Pro✅ SPNIPER ENTRY – Precision Trend Reversal Signals

The SPNIPER ENTRY is a smart trend-following and reversal indicator designed for traders who want timely entries, clear trend confirmation, and clean visuals.

Key Features:

✅ Triple TEMA Trend Confirmation (21, 50, 200): Ensures you're entering only when all moving averages agree on direction.

🎯 Dip/Top Detection: Uses pivot analysis and ATR proximity to detect ideal pullback entries in the prevailing trend.

📉 Stop Loss & Take Profit Zones: ATR-based dynamic SL/TP levels plotted automatically.

📛 False Signal Filter: Avoids multiple entries by maintaining a position until an opposite signal occurs.

📊 Clean Chart Coloring: Candles turn green for confirmed uptrend and red for downtrend—easy to follow.

🔔 Built-in Alerts: Be notified when conditions align perfectly for a high-probability trade.

👁️ Optional TEMA Display: Toggle visibility of trend components for deeper insight.

How it Works:

A buy signal occurs only when:

All 3 TEMA slopes are positive

Price pulls back near a recent pivot low (dip)

A valid uptrend is in place

A sell signal occurs only when:

All 3 TEMA slopes are negative

Price nears a recent pivot high (top)

A confirmed downtrend is active

This indicator is ideal for swing traders, intraday traders, and scalpers who want precise entries based on structure, slope, and volatility.