System 0530 - Stoch RSI Strategy with ATR filterStrategy Description: System 0530 - Multi-Timeframe Stochastic RSI with ATR Filter

Overview:

This strategy, "System 0530," is designed to identify trading opportunities by leveraging the Stochastic RSI indicator across two different timeframes: a shorter timeframe for initial signal triggers (assumed to be the chart's current timeframe, e.g., 5-minute) and a longer timeframe (15-minute) for signal confirmation. It incorporates an ATR (Average True Range) filter to help ensure trades are taken during periods of adequate market volatility and includes a cooldown mechanism to prevent rapid, successive signals in the same direction. Trade exits are primarily handled by reversing signals.

How It Works:

1. Signal Initiation (e.g., 5-Minute Timeframe):

Long Signal Wait: A potential long entry is considered when the 5-minute Stochastic RSI %K line crosses above its %D line, AND the %K value at the time of the cross is at or below a user-defined oversold level (default: 30).

Short Signal Wait: A potential short entry is considered when the 5-minute Stochastic RSI %K line crosses below its %D line, AND the %K value at the time of the cross is at or above a user-defined overbought level (default: 70). When these conditions are met, the strategy enters a "waiting state" for confirmation from the 15-minute timeframe.

2. Signal Confirmation (15-Minute Timeframe):

Once in a waiting state, the strategy looks for confirmation on the 15-minute Stochastic RSI within a user-defined number of 5-minute bars (wait_window_5min_bars, default: 5 bars).

Long Confirmation:

The 15-minute Stochastic RSI %K must be greater than or equal to its %D line.

The 15-minute Stochastic RSI %K value must be below a user-defined threshold (stoch_15min_long_entry_level, default: 40).

Short Confirmation:

The 15-minute Stochastic RSI %K must be less than or equal to its %D line.

The 15-minute Stochastic RSI %K value must be above a user-defined threshold (stoch_15min_short_entry_level, default: 60).

3. Filters:

ATR Volatility Filter: If enabled, trades are only confirmed if the current ATR value (converted to ticks) is above a user-defined minimum threshold (min_atr_value_ticks). This helps to avoid taking signals during periods of very low market volatility. If the ATR condition is not met, the strategy continues to wait for the condition to be met within the confirmation window, provided other conditions still hold.

Signal Cooldown Filter: If enabled, after a signal is generated, the strategy will wait for a minimum number of bars (min_bars_between_signals) before allowing another signal in the same direction. This aims to reduce overtrading.

4. Entry and Exit Logic:

Entry: A strategy.entry() order is placed when all trigger, confirmation, and filter conditions are met.

Exit: This strategy primarily uses reversing signals for exits. For example, if a long position is open, a confirmed short signal will close the long position and open a new short position. There are no explicit take profit or stop loss orders programmed into this version of the script.

Key User-Adjustable Parameters:

Stochastic RSI Parameters: RSI Length, Stochastic RSI Length, %K Smoothing, %D Smoothing.

Signal Trigger & Confirmation:

5-minute %K trigger levels for long and short.

15-minute %K confirmation thresholds for long and short.

Wait window (in 5-minute bars) for 15-minute confirmation.

Filters:

Enable/disable and configure the Signal Cooldown filter (minimum bars between signals).

Enable/disable and configure the ATR Volatility filter (ATR period, minimum ATR value in ticks).

Strategy Parameters:

Leverage Multiplier (Note: This primarily affects theoretical position sizing for backtesting calculations in TradingView and does not simulate actual leveraged trading risks).

Recommendations for Users:

Thorough Backtesting: Test this strategy extensively on historical data for the instruments and timeframes you intend to trade.

Parameter Optimization: Experiment with different parameter settings to find what works best for your trading style and chosen markets. The default values are starting points and may not be optimal for all conditions.

Understand the Logic: Ensure you understand how each component (Stochastic RSI on different timeframes, ATR filter, cooldown) interacts to generate signals.

Risk Management: Since this version does not include explicit stop-loss orders, ensure you have a clear risk management plan in place if trading this strategy live. You might consider manually adding stop-loss orders through your broker or using TradingView's separate strategy order settings for stop-loss if applicable.

Disclaimer:

This strategy description is for informational purposes only and does not constitute financial advice. Past performance is not indicative of future results. Trading involves significant risk of loss. Always do your own research and understand the risks before trading.

Indicators and strategies

TrendMaster Pro 2.3 with Alerts

Hello friends,

A member of the community approached me and asked me how to write an indicator that would achieve a particular set of goals involving comprehensive trend analysis, risk management, and session-based trading controls. Here is one example method of how to create such a system:

Core Strategy Components

Multi-Moving Average System - Uses configurable MA types (EMA, SMA, SMMA) with short-term (9) and long-term (21) periods for primary signal generation through crossovers

Higher Timeframe Trend Filter - Optional trend confirmation using a separate MA (default 50-period) to ensure trades align with broader market direction

Band Power Indicator - Dynamic high/low bands calculated using different MA types to identify price channels and volatility zones

Advanced Signal Filtering

Bollinger Bands Volatility Filter - Prevents trading during low-volatility ranging markets by requiring sufficient band width

RSI Momentum Filter - Uses customizable thresholds (55 for longs, 45 for shorts) to confirm momentum direction

MACD Trend Confirmation - Ensures MACD line position relative to signal line aligns with trade direction

Stochastic Oscillator - Adds momentum confirmation with overbought/oversold levels

ADX Strength Filter - Only allows trades when trend strength exceeds 25 threshold

Session-Based Trading Management

Four Trading Sessions - Asia (18:00-00:00), London (00:00-08:00), NY AM (08:00-13:00), NY PM (13:00-18:00)

Individual Session Limits - Separate maximum trade counts for each session (default 5 per session)

Automatic Session Closure - All positions close at specified market close time

Risk Management Features

Multiple Stop Loss Options - Percentage-based, MA cross, or band-based SL methods

Risk/Reward Ratio - Configurable TP levels based on SL distance (default 1:2)

Auto-Risk Calculation - Dynamic position sizing based on dollar risk limits ($150-$250 range)

Daily Limits - Stop trading after reaching specified TP or SL counts per day

Support & Resistance System

Multiple Pivot Types - Traditional, Fibonacci, Woodie, Classic, DM, and Camarilla calculations

Flexible Timeframes - Auto-adjusting or manual timeframe selection for S/R levels

Historical Levels - Configurable number of past S/R levels to display

Visual Customization - Individual color and display settings for each S/R level

Additional Features

Alert System - Customizable buy/sell alert messages with once-per-bar frequency

Visual Trade Management - Color-coded entry, SL, and TP levels with fill areas

Session Highlighting - Optional background colors for different trading sessions

Comprehensive Filtering - All signals must pass through multiple confirmation layers before execution

This approach demonstrates how to build a professional-grade trading system that combines multiple technical analysis methods with robust risk management and session-based controls, suitable for algorithmic trading across different market sessions.

Good luck and stay safe!

atr stop loss for double SMA v6Strategy Name

atr stop loss for double SMA v6

Credit: This v6 update is based on Daveatt’s “BEST ATR Stop Multiple Strategy.”

Core Logic

Entry: Go long when the 15-period SMA crosses above the 45-period SMA; go short on the inverse cross.

Stop-Loss: On entry, compute ATR(14)×2.0 and set a fixed stop at entry ± that amount. Stop remains static until hit.

Trend Tracking: Uses barssince() to ensure only one active long or short position; stop is only active while that trend persists.

Visualization

Plots fast/slow SMA lines in teal/orange.

On each entry bar, displays a label showing “ATR value” and “ATR×multiple” positioned at the 30-bar low (long) or high (short).

Draws an “×” at the stop-price level in green (long) or red (short) while the position is open.

Execution Settings

Initial Capital: $100 000, Size = 100 shares per trade.

Commission: 0.075% per trade.

Pyramiding: 1.

Calculations: Only on bar close (no intra-bar ticks).

Usage Notes

Static ATR stop adapts to volatility but does not trail.

Ideal for trending, liquid markets (stocks, futures, FX).

Adjust SMA lengths or ATR multiple for faster/slower signals.

Pin Bar Reversal StrategyStrategy: Pin Bar Reversal with Trend Filter

One effective high-probability setup is a Pin Bar reversal in the direction of the larger trend. A pin bar is a candlestick with a tiny body and a long wick, signaling a sharp rejection of price

By itself, a pin bar often marks a potential reversal, but not all pin bars lead to profitable moves. To boost reliability, this strategy trades pin bars only when they align with the prevailing trend – for example, taking a bullish pin bar while the market is in an uptrend, or a bearish pin bar in a downtrend. The trend bias can be determined by a long-term moving average or higher timeframe analysis.

Why it works: In an uptrend, a bullish pin bar after a pullback often indicates that sellers tried to push price down but failed, and buyers are resuming control. Filtering for pin bars near key support or moving averages further improves odds of success. This aligns the entry with both a strong price pattern and the dominant market direction, yielding a higher win rate. The pin bar’s own structure provides natural levels for stop and target placement, keeping risk management straightforward.

Example Setup:

USDCHF - 4 Hour Chart

Trend SMA 12

Max Body - 34

Min Wick - 66

ATR -15

ATR Stop Loss Multiplier - 2.3

ATR Take Profit Multiplier - 2.9

Minimum ATR to Enter - 0.0025

AutoFib Breakout Strategy for Uptrend AssetsThis trading strategy is designed to help you catch powerful upward moves on assets that are in a long-term uptrend, such as Gold (XAUUSD). It uses a popular technical tool called the Fibonacci Extension, combined with a trend filter and a risk-managed exit system.

✅ When to Use This Strategy

• Works best on higher timeframes: Daily (1D), 3-Day (3D), or Weekly (W).

• Best used on uptrending assets like Gold.

• Designed for swing trading – holding trades from a few days to weeks.

📊 How It Works

1. Find the Trend

We only want to trade in the direction of the trend.

• The strategy uses the 200-period EMA (Exponential Moving Average) to identify if the market is in an uptrend.

• If the price is above the 200 EMA, we consider it an uptrend and allow long trades.

2. Identify Breakout Levels

• The strategy detects recent high and low pivot points to draw Fibonacci extension levels.

• It focuses on the 1.618 Fibonacci level, which is often a target in strong trends.

• When the price breaks above this level in an uptrend, it signals a potential momentum breakout – a good time to buy.

3. Enter a Trade

• The strategy enters a long (buy) position when the price closes above the 1.618 Fibonacci level and the market is in an uptrend (above the 200 EMA).

4. Manage Risk Automatically

• The trade includes a stop-loss set to 1x the ATR (Average True Range) below the entry price – this protects against sudden drops.

• It sets a take-profit at 3x the ATR above the entry – aiming for higher rewards than risks.

⚠️ Important Notes

• 📈 Higher Timeframes Preferred: This strategy works best on Daily (D), 3-Day (3D), and Weekly (W) charts, especially on Gold (XAUUSD).

• 🧪 Not for Deep Backtesting: Due to the nature of how pivot points and Fib levels are calculated, this strategy may not perform well in backtesting simulations (because the historical calculations can shift). It is better used for live analysis and forward testing.

Grid TLong V1The “Grid TLong V1” strategy is based on the classic Grid strategy, but in the mode of buying and selling in favor of the trend and only on Long. This allows to take advantage of large uptrend movements to maximize profits in bull markets. For this reason, excessively sideways or bearish markets may not be very conducive to this strategy.

Like our Grid strategies in favor of the trend, you can enter and exit with the balance with controlled risk, as the distance between each grid functions as a natural and adaptable stop loss and take profit. What differentiates it from bidirectional strategies is that Short uses a minimum amount of follow-through, so that the percentage distance between the grids is maintained.

In this version of the script the entries and exits can be chosen at market or limit , and are based on the profit or loss of the current position, not on the percentage change in price.

The user may also notice that the strategy setup is risk-controlled, because it risks 5% on each trade, has a fairly standard commission and modest initial capital, all in order to protect the strategy user from unrealistic results.

As with all strategies, it is strongly recommended to optimize the parameters for the strategy to be effective for each asset and for each time frame.

Random State Machine Strategy📌 Random State Machine Strategy (Educational)

This strategy showcases a randomized entry model driven by a finite state machine, integrated with user-defined exit controls and a full-featured moving average filter.

🧠 Trade Entry Logic

Entries occur only when:

A random trigger occurs (~5% probability per bar)

The state machine accepts a new transition (sm.step())

Price is:

Above the selected MA for long entries

Below the selected MA for short entries

This ensures that entries are both stochastically driven and trend-aligned, avoiding frequent or arbitrary trades.

⚙️ How It Works

Randomized Triggers

A pseudo-random generator (seeded with time and volume) attempts to trigger state transitions.

Finite State Machine

Transitions are managed using the StateMachine from robbatt/lib_statemachine — credit to @robbatt for the modular FSM design.

Controlled Reset

The state machine resets every N bars (default: 100) if at least two transitions have occurred. This prevents stale or locked states.

Backtest Range

Define a specific test window using Start and End Date inputs.

Risk & Exits

Specify risk in points and a target risk/reward ratio. TP is auto-computed. Timed and MA-based exits can be toggled.

🧪 How to Use

Enable Long or Short trades

Choose your Moving Average type and length

Set Risk per trade and R/R ratio

Toggle TP/SL, timed exit, or MA cross exit

Adjust the State Reset Interval to suit your signal frequency

📘 Notes

Educational use only — not financial advice

Random logic is used to model structure, not predict movement

Thanks to @robbatt for the lib_statemachine integration

Strategy Builder With IndicatorsThis strategy script is designed for traders who enjoy building systems using multiple indicators.

Please note: This script does not include any built-in indicators. Instead, it works by referencing the plot outputs of the indicators you’ve already added to your chart.

For example, if you add a MACD and an ATR indicator to your chart, you can assign their plot values as inputs in the settings panel of this strategy.

• MACD as a trigger

• ATR as a filter

How Filters Work

Filters check whether certain conditions are met before a trade can be opened. For instance, if you set a filter like ATR > 30, then no trade will be executed unless that condition is true — even if the trigger fires.

All filters are linked, meaning every active filter must be satisfied for a trade to occur.

How Triggers Work

Triggers are what actually fire a trade signal — such as a moving average crossover or RSI breaking above a specific level. Unlike filters, triggers are independent. Only one active trigger needs to be true for the trade to execute.

Thanks to its modular structure, this strategy can be used with any indicator of your choice.

⸻

Risk Management Features

In the settings, you’ll find flexible options for:

• Stop Loss (SL)

• Trailing Stop Loss (TSL)

• Multi Take-Profit (TP)

These features enhance trade safety and let you tailor your risk management.

SL types available:

• Tick-based SL

• Percent-based SL

• ATR-based SL

Once you select your preferred SL type, you can fine-tune its distance using the offset field.

Trailing SL allows your stop to follow price as it moves in your favor — helping to lock in profits.

Multi-TP lets you take profits at two different levels, helping you secure gains while leaving room for extended moves.

Breakeven option is also available to automatically move your SL to entry after reaching a profit threshold.

⸻

How to Build a Solid Strategy

Let’s break down a good setup into three key components:

1. Trend Filter

Avoid trading against the trend — that’s like swimming against the current.

Use a filter like:

• Supertrend

• Momentum indicators

• Candlestick bias, etc.

Example: In this case, I used Supertrend and filtered for trades only if the price is above the uptrend line.

2. Trigger Condition

Once we confirm the trend is on our side, we need a trigger to execute at the right moment. This can be:

• RSI cross

• Candlestick patterns

• Trendline breaks

• Moving average crossovers, etc.

Example: I used RSI crossing above 50 as the entry trigger.

3. Risk Management

Even in the right trend at the right time — anything can happen. That’s why you should always define Stop Loss and Take Profit levels.

⸻

And there you have it! Your strategy is ready to backtest, refine, and deploy with alerts for live trading.

Questions or suggestions? Feel free to reach out

Volatility Bias ModelVolatility Bias Model

Overview

Volatility Bias Model is a purely mathematical, non-indicator-based trading system that detects directional probability shifts during high volatility market phases. Rather than relying on classic tools like RSI or moving averages, this strategy uses raw price behavior and clustering logic to determine potential breakout direction based on recent market bias.

How It Works

Over a defined lookback window (default 10 bars), the strategy counts how many candles closed in the same direction (i.e., bullish or bearish).

Simultaneously, it calculates the price range during that window.

If volatility is above a minimum threshold and a clear directional bias is detected (e.g., >60% of closes are bullish), a trade is opened in the direction of that bias.

This approach assumes that when high volatility is coupled with directional closing consistency, the market is probabilistically more likely to continue in that direction.

ATR-based stop-loss and take-profit levels are applied, and trades auto-exit after 20 bars if targets are not hit.

Key Features

- 100% non-indicator-based logic

- Statistically-driven directional bias detection

- Works across all timeframes (1H, 4H, 1D)

- ATR-based risk management

- No pyramiding, slippage and commissions included

- Compatible with real-world backtesting conditions

Realism & Assumptions

To make this strategy more aligned with actual trading environments, it includes 0.05% commission per trade and a 1-point slippage on every entry and exit.

Additionally, position sizing is set at 10% of a $10,000 starting capital, and no pyramiding is allowed.

These assumptions help avoid unrealistic backtest results and make the performance metrics more representative of live conditions.

Parameter Explanation

Bias Window (10 bars): Number of past candles used to evaluate directional closings

Bias Threshold (0.60): Required ratio of same-direction candles to consider a bias valid

Minimum Range (1.5%): Ensures the market is volatile enough to avoid noise

ATR Length (14): Used to dynamically define stop-loss and target zones

Risk-Reward Ratio (2.0): Take-profit is set at twice the stop-loss distance

Max Holding Bars (20): Trades are closed automatically after 20 bars to prevent stagnation

Originality Note

Unlike common strategies based on oscillators or moving averages, this script is built on pure statistical inference. It models the market as a probabilistic process and identifies directional intent based on historical closing behavior, filtered by volatility. This makes it a non-linear, adaptive model grounded in real-world price structure — not traditional technical indicators.

Disclaimer

This strategy is for educational and experimental purposes only. It does not constitute financial advice. Always perform your own analysis and test thoroughly before applying with real capital.

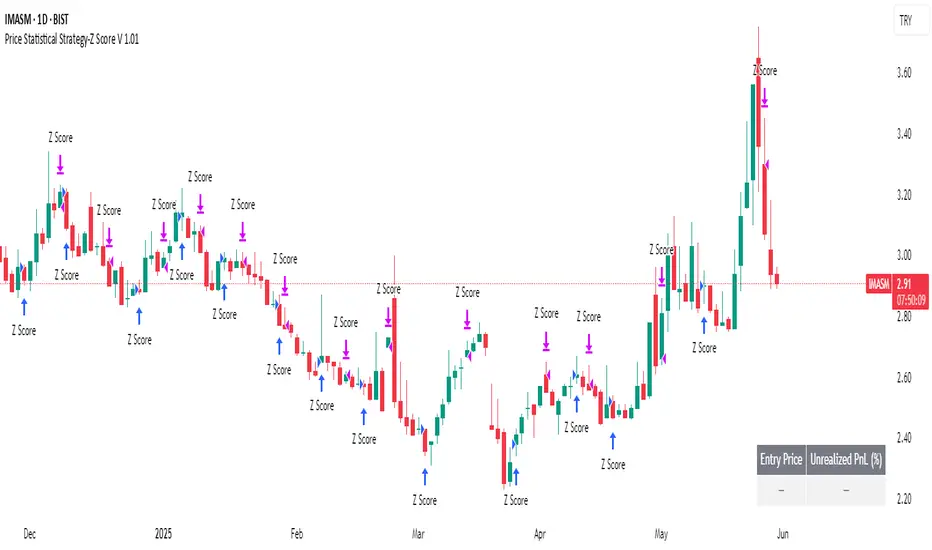

Price Statistical Strategy-Z Score V 1.01

Price Statistical Strategy – Z Score V 1.01

Overview

A technical breakdown of the logic and components of the “Price Statistical Strategy – Z Score V 1.01”.

This script implements a smoothed Z-Score crossover mechanism applied to the closing price to detect potential statistical deviations from local price mean. The strategy operates solely on price data (close) and includes signal spacing control and momentum-based candle filters. No volume-based or trend-detection components are included.

Core Methodology

The strategy is built on the statistical concept of Z-Score, which quantifies how far a value (closing price) is from its recent average, normalized by standard deviation. Two moving averages of the raw Z-Score are calculated: a short-term and a long-term smoothed version. The crossover between them generates long entries and exits.

Signal Conditions

Entry Condition:

A long position is opened when the short-term smoothed Z-Score crosses above the long-term smoothed Z-Score, and additional entry conditions are met.

Exit Condition:

The position is closed when the short-term Z-Score crosses below the long-term Z-Score, provided the exit conditions allow.

Signal Gapping:

A minimum number of bars (Bars gap between identical signals) must pass between repeated entry or exit signals to reduce noise.

Momentum Filter:

Entries are prevented during sequences of three or more consecutively bullish candles, and exits are prevented during three or more consecutively bearish candles.

Z-Score Function

The Z-Score is calculated as:

Z = (Close - SMA(Close, N)) / STDEV(Close, N)

Where N is the base period selected by the user.

Input Parameters

Enable Smoothed Z-Score Strategy

Enables or disables the Z-Score strategy logic. When disabled, no trades are executed.

Z-Score Base Period

Defines the number of bars used to calculate the simple moving average and standard deviation for the Z-Score. This value affects how responsive the raw Z-Score is to price changes.

Short-Term Smoothing

Sets the smoothing window for the short-term Z-Score. Higher values produce smoother short-term signals, reducing sensitivity to short-term volatility.

Long-Term Smoothing

Sets the smoothing window for the long-term Z-Score, which acts as the reference line in the crossover logic.

Bars gap between identical signals

Minimum number of bars that must pass before another signal of the same type (entry or exit) is allowed. This helps reduce redundant or overly frequent signals.

Trade Visualization Table

A table positioned at the bottom-right displays live PnL for open trades:

Entry Price

Unrealized PnL %

Text colors adapt based on whether unrealized profit is positive, negative, or neutral.

Technical Notes

This strategy uses only close prices — no trend indicators or volume components are applied.

All calculations are based on simple moving averages and standard deviation over user-defined windows.

Designed as a minimal, isolated Z-Score engine without confirmation filters or multi-factor triggers.

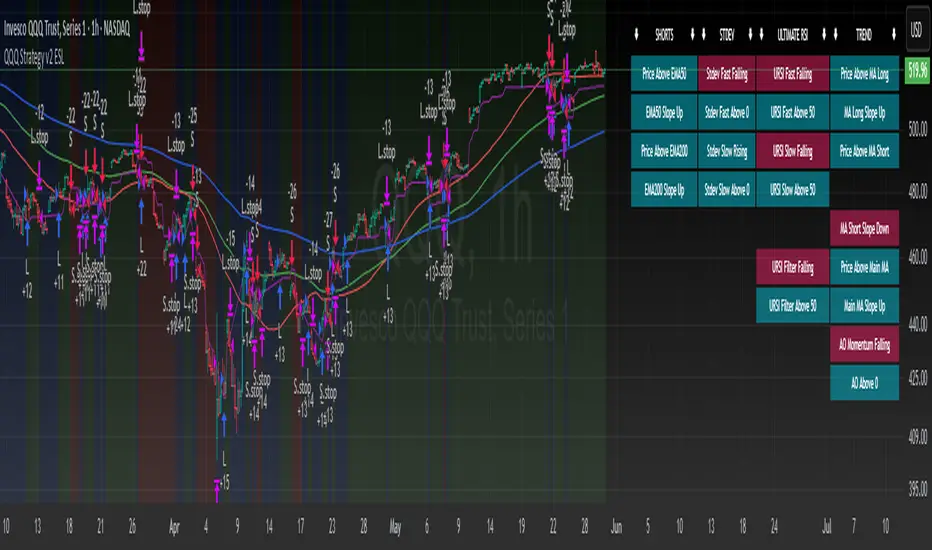

QQQ Strategy v2 ESL | easy-peasy-x This is a strategy optimized for QQQ (and SPY) for the 1H timeframe. It significantly outperforms passive buy-and-hold approach. With settings adjustments, it can be used on various assets like stocks and cryptos and various timeframes, although the default out of the box settings favor QQQ 1H.

The strategy uses various triggers to take both long and short trades. These can be adjusted in settings. If you try a different asset, see what combination of triggers works best for you.

Some of the triggers employ LuxAlgo's Ultimate RSI - shoutout to him for great script, check it out here .

Other triggers are based on custom signed standard deviation - basically the idea is to trade Bollinger Bands expansions (long to the upside, short to the downside) and fade or stay out of contractions.

There are three key moving averages in the strategy - LONG MA, SHORT MA, BASIC MA. Long and Short MAs are guides to eyes on the chart and also act as possible trend filters (adjustable in settings). Basic MA acts as guide to eye and a possible trade trigger (adjustable in settings).

There are a few trend filters the strategy can use - moving average, signed standard deviation, ultimate RSI or none. The filters act as an additional condition on triggers, making the strategy take trades only if both triggers and trend filter allows. That way one can filter out trades with unfavorable risk/reward (for instance, don't long if price is under the MA200). Different trade filters can be used for long and short trades.

The strategy employs various stop loss types, the default of which is a trailing %-based stop loss type. ATR-based stop loss is also available. The default 1.5% trailing stop loss is suitable for leveraged trading.

Lastly, the strategy can trigger take profit orders if certain conditions are met, adjustable in settings. Also, it can hold onto winning trades and exit only after stop out (in which case, consecutive triggers to take other positions will be ignored until stop out).

Let me know if you like it and if you use it, what kind of tweaks would you like to see.

With kind regards,

easy-peasy-x

Three Candle Bullish Engulfing StrategyThe Three Candle Bullish Engulfing Strategy is a versatile, multi-mode trading system designed for TradingView, combining classic candlestick patterns with momentum confirmation and dynamic risk management. This script supports both swing trading and intraday approaches, as well as an optional RSI-based breakout mode for additional signal filtering.

Key Features:

Three Candle Pattern Detection:

The strategy identifies potential trend reversal points using a three-candle pattern:

The first candle is a strong bullish (or bearish) move.

The second candle is a doji or small-bodied candle, indicating indecision.

The third candle is a bullish (or bearish) engulfing candle that closes above (or below) the previous high (or low), confirming the reversal.

Flexible Trading Modes:

Swing Long Only: Enter long trades on bullish three-candle setups.

Intraday Long & Short: Trade both long and short based on bullish and bearish three-candle patterns, with automatic session-end exits.

RSI Breakout Mode: Enter long trades when the 1-hour RSI exceeds a user-defined threshold (default 80) and a bullish candle forms, with breakout confirmation and a fixed-percentage stop loss.

Visual Aids:

Plots the RSI breakout trigger price and stop loss on the chart for easy monitoring.

How It Works:

Three Candle Pattern Entries:

Long Entry: Triggered when a bullish candle is followed by a doji, then a bullish engulfing candle closes above the previous high.

Short Entry (Intraday only): Triggered by the inverse pattern—bearish candle, doji, then bearish engulfing candle closing below the previous low.

RSI Breakout Entries:

When the RSI on a higher timeframe (default 1 hour) exceeds the set threshold and a bullish candle forms, the script records a trigger price.

A long trade is entered if the price breaks above this trigger, with a stop loss set a fixed percentage below.

Exits:

Positions are closed if the trailing stop is hit, the session ends (for intraday mode), or the stop loss is triggered in RSI breakout mode.

In RSI breakout mode, positions are also closed if a new breakout trigger forms while in position.

MACD + RSI + EMA + BB + ATR Day Trading StrategyEntry Conditions and Signals

The strategy implements a multi-layered filtering approach to entry conditions, requiring alignment across technical indicators, timeframes, and market conditions .

Long Entry Requirements

Trend Filter: Fast EMA (9) must be above Slow EMA (21), price must be above Fast EMA, and higher timeframe must confirm uptrend

MACD Signal: MACD line crosses above signal line, indicating increasing bullish momentum

RSI Condition: RSI below 70 (not overbought) but above 40 (showing momentum)

Volume & Volatility: Current volume exceeds 1.2x 20-period average and ATR shows sufficient market movement

Time Filter: Trading occurs during optimal hours (9:30-11:30 AM ET) when market volatility is typically highest

Exit Strategies

The strategy employs multiple exit mechanisms to adapt to changing market conditions and protect profits :

Stop Loss Management

Initial Stop: Placed at 2.0x ATR from entry price, adapting to current market volatility

Trailing Stop: 1.5x ATR trailing stop that moves up (for longs) or down (for shorts) as price moves favorably

Time-Based Exits: All positions closed by end of trading day (4:00 PM ET) to avoid overnight risk

Best Practices for Implementation

Settings

Chart Setup: 5-minute timeframe for execution with 15-minute chart for trend confirmation

Session Times: Focus on 9:30-11:30 AM ET trading for highest volatility and opportunity

Multi-Indicator Trend-Following Strategy v6Multi-Indicator Trend-Following Strategy v6

This strategy uses a combination of technical indicators to identify potential trend-following trade entries and exits. It is intended for educational and research purposes.

How it works:

Moving Averages (EMA): Entry signals are generated on crossovers between a fast and slow exponential moving average.

RSI Filter: Confirms momentum with a threshold above/below 50 for long/short entries.

Volume Confirmation: Requires volume to exceed a moving average multiplied by a user-defined factor.

ATR-Based Risk Management: Stop loss and take profit levels are calculated using the Average True Range (ATR), allowing for dynamic risk control based on market volatility.

Customizable Inputs:

Fast/Slow MA lengths

RSI length and levels

MACD settings (used in calculation, not directly in signal)

Volume MA and multiplier

ATR period and multipliers for stop loss and take profit

Notes:

This strategy does not guarantee future results.

It is provided for analysis and backtesting only.

Alerts are available for buy/sell conditions.

Feel free to adjust parameters to explore different market conditions and asset classes.

Long Explosive V1The “Long Explosive V1” strategy calculates the percentage change in price from the last closing price of the candlestick, so that if it increases by a certain percentage it goes long, but if it decreases by another percentage it sends an exit order, so that the percentage limits above and below the current price function as inherent stop loss and take profit, with the benefit of taking advantage of the volatility of the bull market.

Entries and exits are always at the market and based on percentage changes in the price. Of course, the default configuration of the strategy considers a position with a 5% risk control, modest initial capital and standard commissions, which helps to obtain realistic results and protect the user from unexpectedly controlled potential losses.

It is again emphasized that it is always advisable to adjust the parameters of the strategy well, so that the risk-reward is well controlled.

Reversal Trap Sniper – Verified VersionReversal Trap Sniper

Overview

Reversal Trap Sniper is a counterintuitive momentum-following strategy that identifies "reversal traps"—situations where traders expect a market reversal based on RSI, but the price continues trending. By detecting these failed reversal signals, the strategy enters trades in the trend direction, often catching strong follow-through moves.

How It Works

The system monitors the Relative Strength Index (RSI). When RSI moves above the overbought level (e.g., 70) and then drops back below it, many traders interpret this as a sell signal.

However, this strategy treats such moves with caution. If the RSI pulls back below the overbought threshold but the price continues to rise, the system considers it a "reversal trap"—a fakeout.

In such cases, instead of going short, the strategy enters a long position, assuming that the trend is still valid and those betting on a reversal may fuel a breakout.

Similarly, if RSI rises above the oversold level from below, but price continues falling, a short trade is triggered.

Entries are followed by ATR-based stop-loss and dynamic take-profit (2× risk), with a fallback time-based exit after 30 bars.

Key Features

- Detects failed RSI-based reversals ("traps")

- Follows momentum after the trap is triggered

- Uses ATR for dynamic stop-loss and take-profit

- Auto-exit after a fixed bar count (30 bars)

- Visual markers on chart for transparency

- Realistic trading assumptions: 0.05% commission, slippage, and capped pyramiding

Parameter Explanation

RSI Length (14): Standard RSI calculation period

Overbought/Oversold Levels (70/30): Common thresholds used by many traders

ATR Length (14): Used to define stop-loss and target dynamically

Risk-Reward Ratio (2.0): Take-profit is set at 2× the stop-loss distance

Max Holding Bars (30): Ensures trades don’t remain open indefinitely

Pyramiding (10): Allows scaling into trades, simulating real-world strategy stacking

Originality Note

This strategy inverts traditional RSI logic. Instead of treating overbought/oversold conditions as signals for reversal, it waits for those signals to fail. Only after such failures, confirmed by continued price action in the same direction, does the system enter trades. This logic is based on the behavioral observation that failed reversal signals often trigger stronger trend continuation—making this strategy uniquely positioned to exploit trap scenarios.

Disclaimer

This script is for educational and research purposes only. Trading involves risk, and past performance does not guarantee future results. Always test thoroughly before applying with live capital.

Dual MACD Strategy [Js.k]Strategy Overview

The Dual MACD Strategy leverages two MACD indicators with different parameters to generate buy and sell signals. By combining the trend-following properties of MACD with specific entry/exit criteria, this strategy aims to capture significant price movements while effectively managing risk.

Entry and Exit Conditions

Long Entry: A buy signal is triggered when:

The histogram of MACD1 crosses above zero.

The histogram of MACD2 is positive and rising.

Short Entry: A sell signal is triggered when:

The histogram of MACD1 crosses below zero.

The histogram of MACD2 is negative and declining.

Risk Management

Stop Loss and Take Profit:

Stop Loss is set at 1% below the entry price for long positions and 1% above the entry price for short positions.

Take Profit is set at 1.5% above the entry price for long positions and 1.5% below the entry price for short positions.

Position Sizing: Each trade risks a maximum of 10% of account equity, keeping potential losses manageable and in line with standard trading practices.

Backtesting Results

The strategy is tested on BTCUSDT with a time frame of 1 hour, resulting in 200+ trades.

The initial capital for backtesting is set to $10,000, with a realistic commission of 0.04% and a slippage of 2 ticks.

Conclusion

This strategy is inspired by Dreadblitz's Double MACD Buy and Sell, as well as some YouTube videos. My purpose in redeveloping them into this strategy is to validate the practicality of the Double MACD. After multiple modifications, this is the final version. I believe its profitability is limited and may lead to losses; please do not use this strategy for live trading.

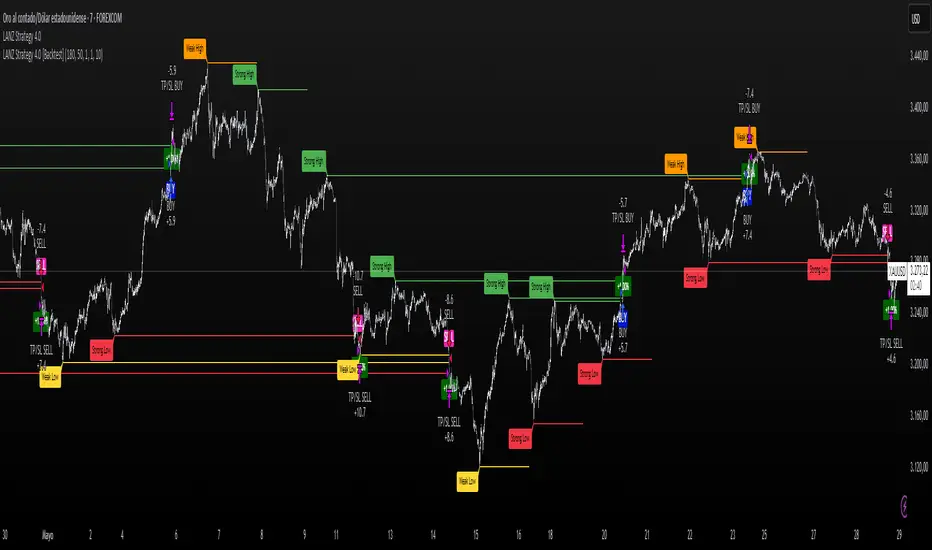

LANZ Strategy 4.0 [Backtest]🔷 LANZ Strategy 4.0 — Strategy Execution Based on Confirmed Structure + Risk-Based SL/TP

LANZ Strategy 4.0 is the official backtesting engine for the LANZ Strategy 4.0 trading logic. It simulates real-time executions based on breakout of Strong/Weak Highs or Lows, using a consistent structural system with SL/TP dynamically calculated per trade. With integrated risk management and lot size logic, this script allows traders to validate LANZ Strategy 4.0 performance with real strategy metrics.

🧠 Core Components:

Confirmed Breakout Entries: Trades are executed only when price breaks the most recent structural level (Strong High or Strong Low), detected using swing pivots.

Dynamic SL and TP Logic: SL is placed below/above the breakout point with a customizable buffer. TP is defined using a fixed Risk-Reward (RR) ratio.

Capital-Based Risk Management: Lot size is calculated based on account equity, SL distance, and pip value (e.g. $10 per pip on XAUUSD).

Clean and Controlled Executions: Only one trade is active at a time. No new entries are allowed until the current position is closed.

📊 Visual Features:

Automatic plotting of Entry, SL, and TP levels.

Full control of swing sensitivity (swingLength) and SL buffer.

SL and TP lines extend visually for clarity of trade risk and reward zones.

⚙️ How It Works:

Detects pivots and classifies trend direction.

Waits for breakout above Strong High (BUY) or below Strong Low (SELL).

Calculates dynamic SL and TP based on buffer and RR.

Computes trade size automatically based on risk per trade %.

Executes entry and manages exits via strategy engine.

📝 Notes:

Ideal for evaluating the LANZ Strategy 4.0 logic over historical data.

Must be paired with the original indicator (LANZ Strategy 4.0) for live trading.

Best used on assets with clear structural behavior (gold, indices, FX).

📌 Credits:

Backtest engine developed by LANZ based on the official rules of LANZ Strategy 4.0. This script ensures visual and logical consistency between live charting and backtesting simulations.

NY Opening Range Breakout - MA StopCore Concept

This strategy trades breakouts from the New York opening range (9:30-9:45 AM NY time) on intraday timeframes, designed for scalping and day trading.

Setup Requirements

Timeframe: Works on any timeframe under 15 minutes (1m, 2m, 3m, 5m, 10m)

Session: New York market hours

Range Period: 9:30-9:45 AM NY time (15-minute opening range)

Entry Rules

Long Entries:

Wait for a candle to close above the opening range high

Enter long on the next candle (before 12:00 PM NY time)

Must be above moving average if using MA-based take profit

Short Entries:

Wait for a candle to close below the opening range low

Enter short on the next candle (before 12:00 PM NY time)

Must be below moving average if using MA-based take profit

Risk Management

Stop Loss:

Long trades: Opening range low

Short trades: Opening range high

Take Profit Options:

Fixed Risk Reward: 1.5x the range size (customizable ratio)

Moving Average: Exit when price crosses back through MA

Both: Whichever comes first

Key Features

Trade Direction Options:

Long Only

Short Only

Both directions

Moving Average Filter:

Prevents entries that would immediately hit stop loss

Uses EMA/SMA/WMA/VWMA with customizable length

Acts as dynamic support/resistance

Time Restrictions:

No entries after 12:00 PM NY time (customizable cutoff)

One trade per direction per day

Daily reset of all variables

Visual Elements

Red/green lines showing opening range

Purple line for moving average

Entry and breakout signals with shapes

Take profit and stop loss levels plotted

Information table with current status

Strategy Logic Flow

Morning: Capture 9:30-9:45 range high/low

Wait: Monitor for breakout (previous candle close outside range)

Filter: Check MA condition if using MA-based exits

Enter: Trade on next candle after breakout

Manage: Exit at fixed TP, MA cross, or stop loss

Reset: Start fresh next trading day

This is a momentum-based breakout strategy that capitalizes on early market volatility while using the opening range as natural support/resistance levels.

RSI SwingRadar🧠 Strategy Overview

This long-only strategy combines RSI/MA crossovers with ATR-based risk management, designed for cleaner entries during potential bounce phases — especially tuned for assets like XMR/USDT.

🔍 Core Logic:

- RSI Crossover: Entry occurs when the 14-period RSI crosses above its 14-period SMA, signaling a potential shift in momentum.

- Oversold Filter: The RSI must have been below a user-defined oversold threshold (default: 35) on the previous candle, filtering for bounce setups after a pullback.

- ATR-Based Stop/Target: Stop-loss is placed below the low by a user-adjustable ATR multiplier (default: 0.5×). Take-profit is calculated with a Risk:Reward multiplier (default: 4×).

These elements work in tandem — RSI crossovers give momentum confirmation, oversold filtering adds context, and ATR-based exits adapt to volatility, creating a compact yet responsive strategy.

📉 Visuals:

- Dynamic Bands: The chart displays the active stop-loss, entry price, and take-profit as colored bands for easy visual tracking.

- Clean Overlay: Designed with simplicity — only confirmed setups are shown, keeping noise low.

✅ Suggested Use:

- Works best on XMR/USDT or similarly trending assets.

- Best suited for pullback entries during broader uptrends.

- Adjustable for different volatility conditions and asset behaviors.

⚠️ Disclaimer

- This strategy is for educational and research purposes only.

- It does not guarantee profitability in any market.

- Always backtest, forward-test, and understand your own risk tolerance before using any

strategy in a live environment.

- Past performance is not indicative of future results.

- This script is not financial advice.

Trend Surge with Pullback FilterTrend Surge with Pullback Filter

Overview

Trend Surge with Pullback Filter is a price action-based strategy designed to enter strong trends not at the breakout, but at the first controlled pullback after a surge. It filters out noise by requiring momentum confirmation and low volatility conditions, aiming for better entry prices and reduced risk exposure.

How It Works

A strong upward trend is identified when the Rate of Change (ROC) exceeds a defined percentage (e.g., 2%).

Instead of jumping into the trend immediately, the strategy waits for a pullback: the price must drop at least 1% below its recent high (over the past 3 candles).

A low volatility environment is also required for entry — measured using ATR being below its 20-period average multiplied by a safety factor.

If all three conditions are met (trend + pullback + quiet volatility), the system enters a long position.

The trade is managed using a dynamic ATR-based stop-loss and a take-profit at 2x ATR.

An automatic exit occurs after 30 bars if neither SL nor TP is hit.

Key Features

- Momentum-triggered trend detection via ROC

- Smart pullback filter avoids overbought entries

- Volatility-based filter to eliminate noise and choppy conditions

- Dynamic risk-reward ratio with ATR-driven exit logic

- Time-limited exposure using bar-based exit

Parameter Explanation

ROC Length (10): Looks for short-term price surges

ROC Threshold (2.0%): Trend is considered valid if price increased more than 2%

Pullback Lookback (3): Checks last 3 candles for price retracement

Minimum Pullback % (1.0%): Entry only if price pulled back at least 1%

ATR Length (14): Measures current volatility

Low Volatility Multiplier (1.2): ATR must be below this multiple of its 20-period average

Risk-Reward (2.0): Target is set at 2x the stop-loss distance

Max Bars (30): Trade is closed automatically after 30 bars

Originality Statement

This strategy doesn’t enter at the trend start, unlike many momentum bots. Instead, it waits for the first market hesitation — a minor pullback under low volatility — before entering. This logic mimics how real traders often wait for a better entry after a breakout, avoiding emotional overbought buys. The combined use of ROC, dynamic pullback detection, and ATR-based environment filters makes it both practical and original for real-world trading.

Disclaimer

This strategy is intended for educational and research purposes. Backtest thoroughly and understand the logic before using with real capital.

MNQ EMA StrategyThis strategy is not perfected yet. ONE MINUTE TIMEFRAME

The goal is to take Longs above the 5 ema when price is above all the 200, 30, and 5 ema.

Short side is when candle closes below the 5 ema and price is below the 300, 30, and 5 ema.

I use candle range blocks for different time zones to avoid excess orders from being triggered. As well as blocks when stoploss is hit or after a profitable trade of certain ticks.

There is an RSI to avoid trades when there isn't too much movement.

My goal is to get an entry when price trades above the 5 ema and then next candle passes it by .25 instead of entering immediately. The stoploss as the low of candle before entry and TP as 3 times the stoploss. I've tried a million times to make it like this but I don't know how to use pine script or Code.

The sell side is basically the same, enter at candle close below 5 ema wait for low to get swept to enter and stoploss above previous high, with TP 3 times the stoploss.

Publishing in hopes anyone knows how to adjust this

CAUTION THIS STRATEGY WORKS WITH CURRENT PRICE ACTION DUE TO ME USING RECENT TICK COUNT RATHER THAN BASED ON CANDLES OR PERCENTAGES. THIS WILL ONLY WORK AS LONG AS MARKET MOVES AS IT HAS BEEN SINCE 2024. CME_MINI:MNQ1!

Hammer + EMA Strategy with Tick-based SL/TPWhat This Script Does:

Detects Hammer (bullish reversal) and Inverted Hammer (bearish reversal) patterns

Requires a simple trend context (using 2 bars back)

Confirms price position relative to EMA 50

Applies tick-based SL and TP

Plots buy/sell signals on chart with emoji labels